Since Grab’s announcement of SPAC merger with Altimeter Growth Corp (AGC), Southeast Asia’s most valued unicorn has been working towards becoming a public company.

Yesterday (2 Aug 2021), Grab Holdings Limited filed its securities registration document (Form F4) with the SEC, which gave more details about its business(es). The company also released its Q1 2021 results on the same day.

Q1 2021 was the last time that a pandemic quarter is compared to a ‘normal’ quarter year on year. (Southeast Asia entered various stages of lockdowns end of Q1 to Q2 2020).

Both releases contained a lot of information, and we thought it would be interesting and worthwhile to point out a few highlights especially on the Q1 results:

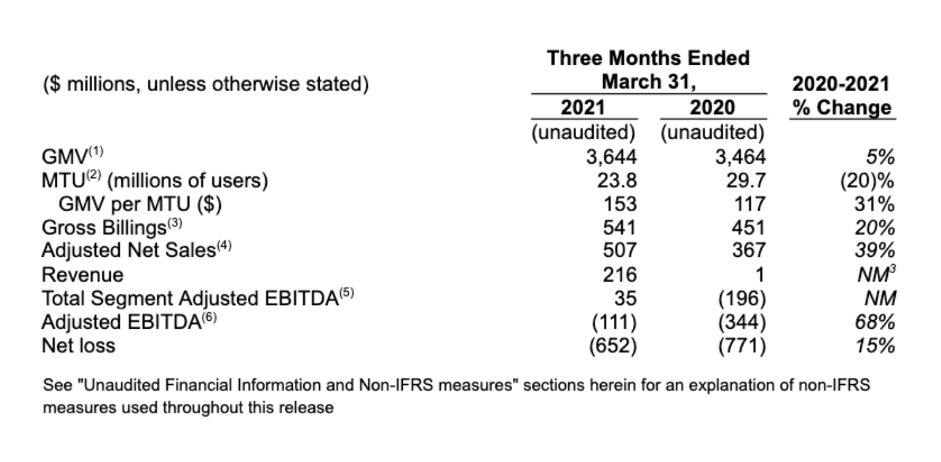

How is the overall performance of Grab?

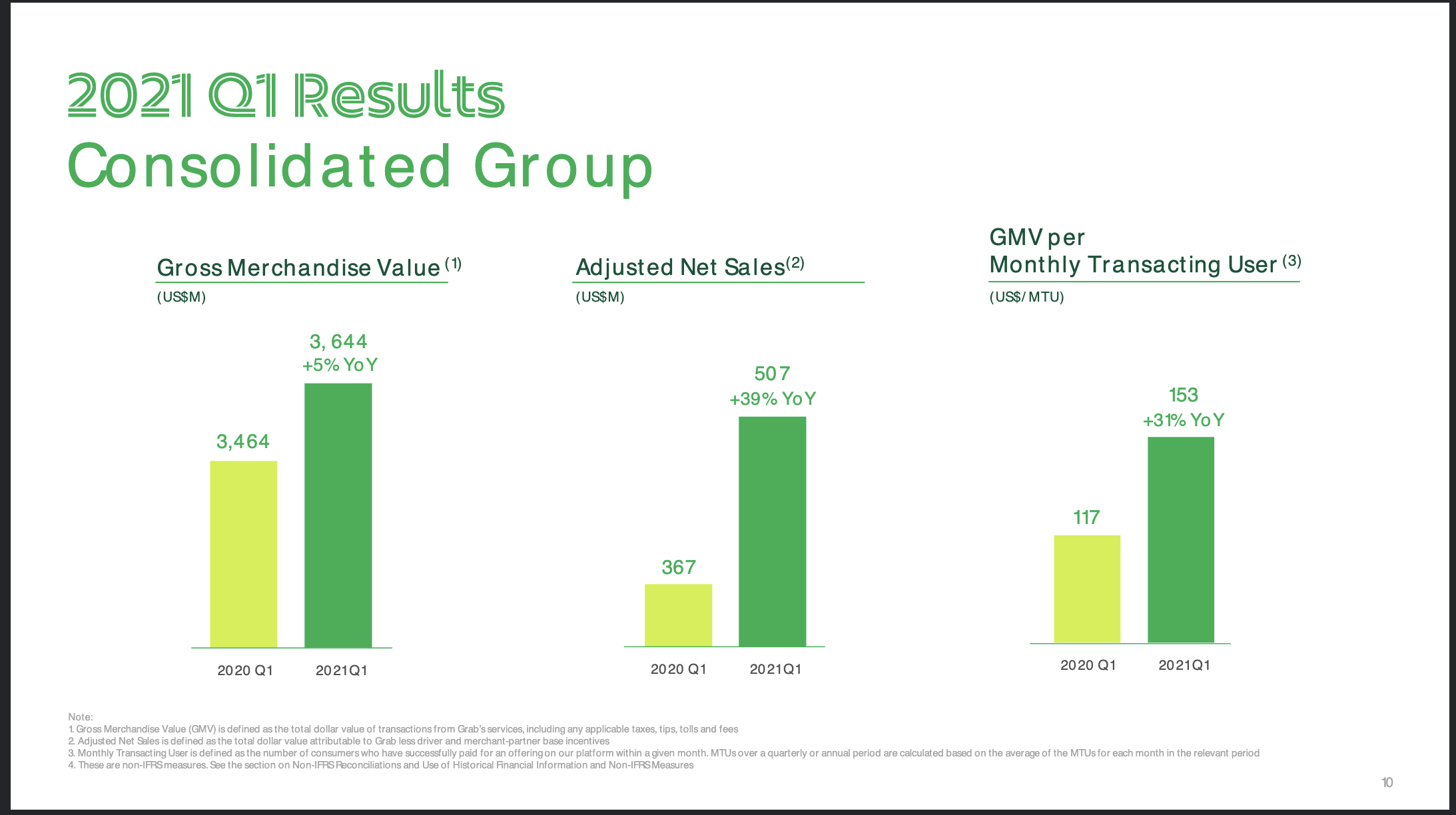

Overall the Q1 performance is actually not bad at all considering the pandemic circumstances that have been engulfing Southeast Asia.

Ride hailing took a big hit because of the movement restrictions imposed in the region, causing overall users (Monthly Transacting Users – or MTUs) to drop (by 20%), and GMV growth to be modest (5%).

However, the quality of users and revenue improved significantly. Adjusted Net Sales, which is defined as Gross Billings (you can think of it as take rate) minus driver/merchant incentives, grew by 39%; while GMV per MTU grew by 31%.

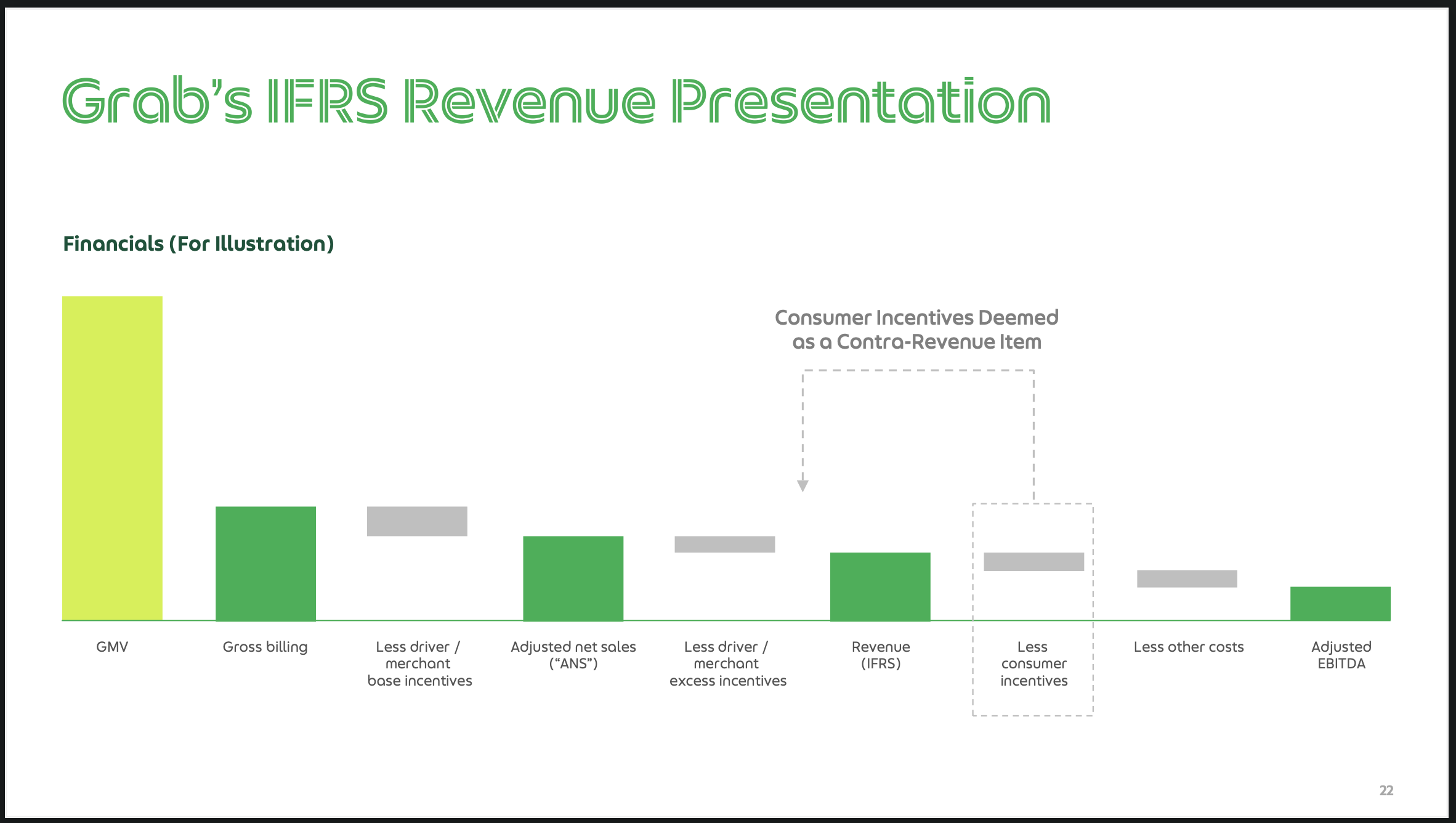

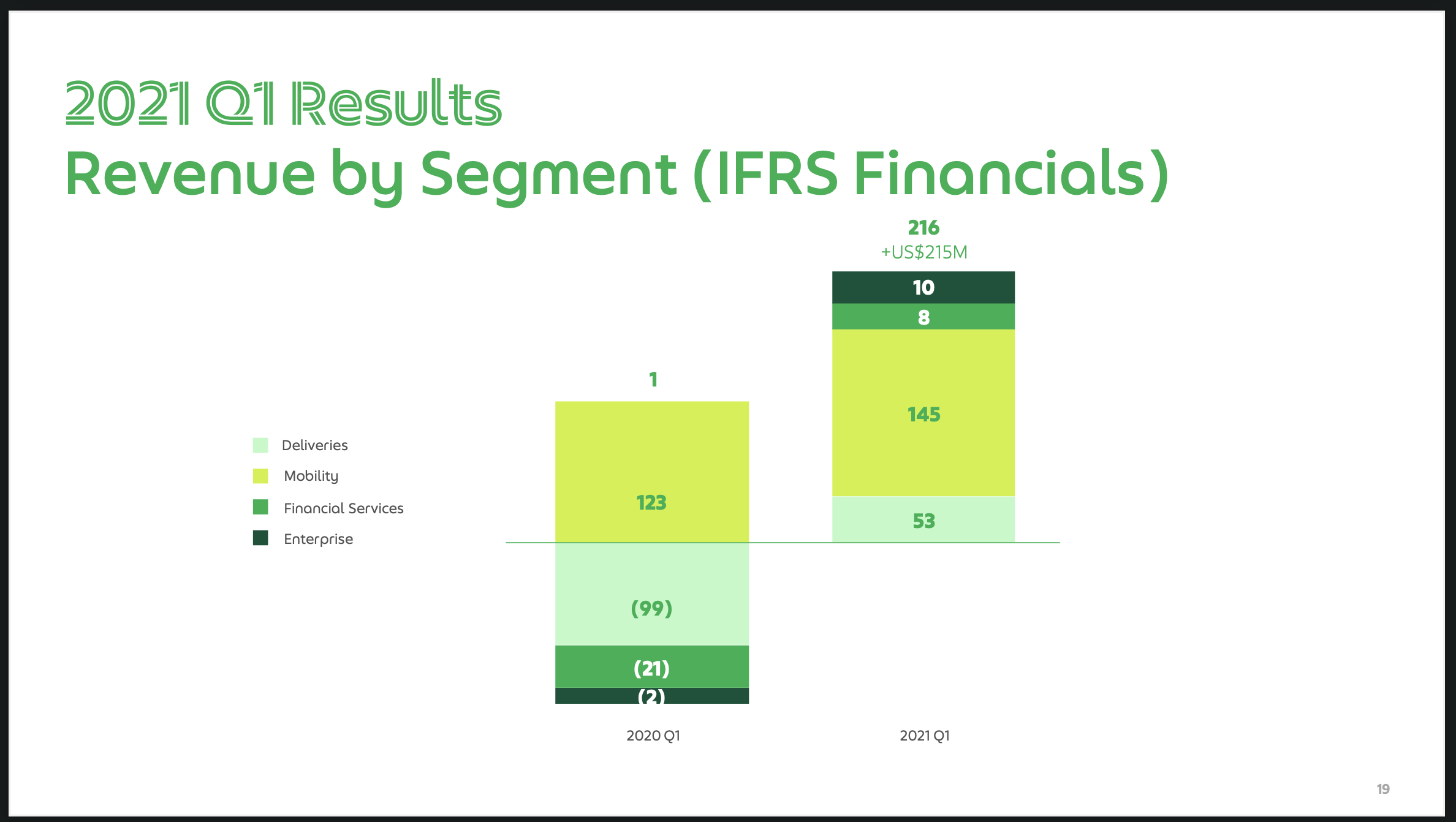

Interestingly, the revenue of Q1 2020 was recognised as $1 million, which stood out as an oddly small number. This is due to accounting treatment changes that affected the top line (but not the bottom line), which we will explain below (in section: Is Grab’s public listing on track?).

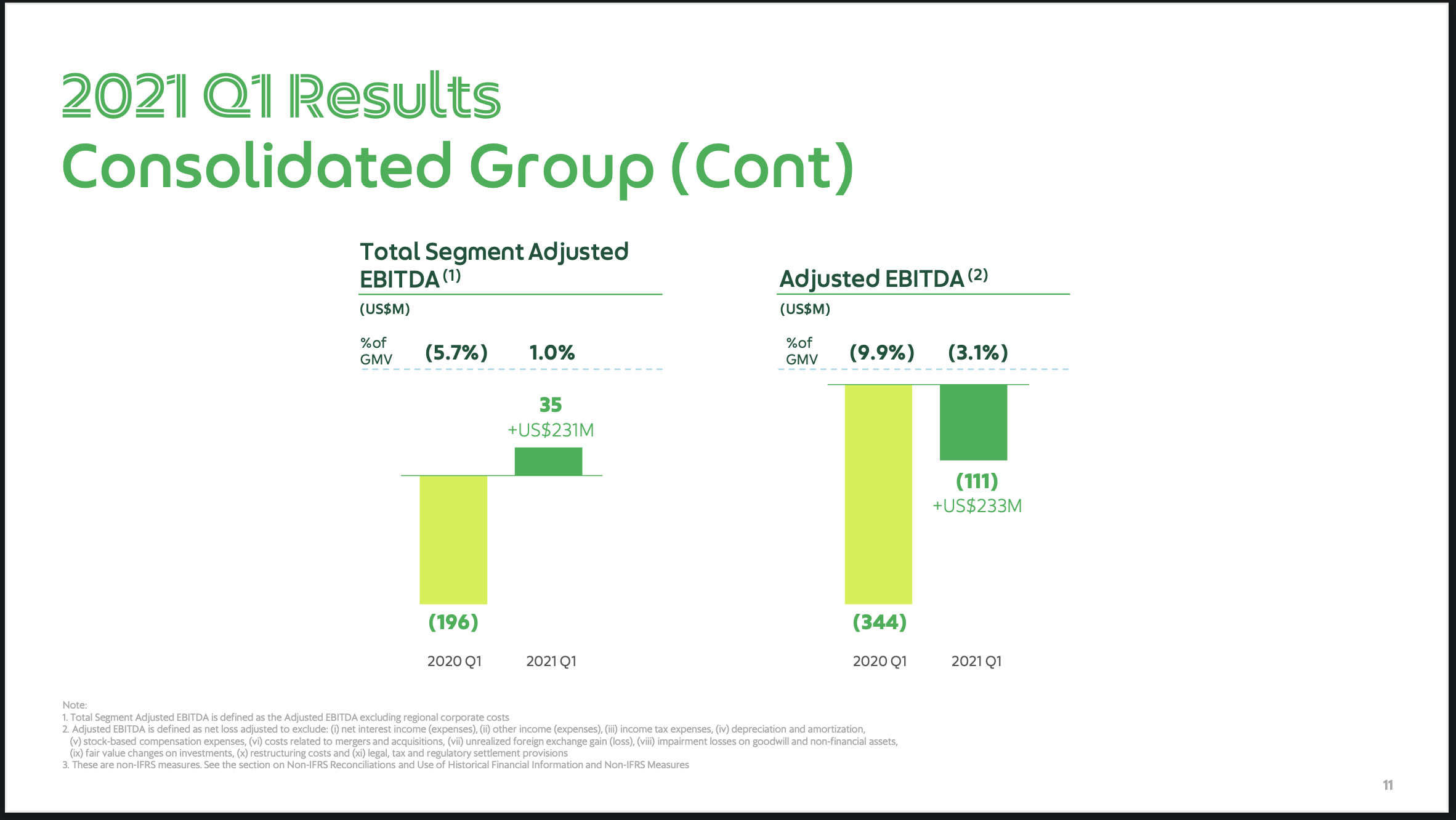

Profitability also improved – with total segment adjusted EBITDA (i.e. the sum of EBITDA of all segments) turning positive. Ride-hailing is positive, deliveries close to, while financial services are still running a big loss.

That is understandable, as in ride hailing Grab is clearly leading around the region, in food deliveries it has about half of market share (check Momentum Works Food Delivery Platforms in Southeast Asia report launched in Jan 2021), while payment and financial services are still very fragmented with stiff competition.

A more visual way of the table above, taken from their earnings presentation yesterday:

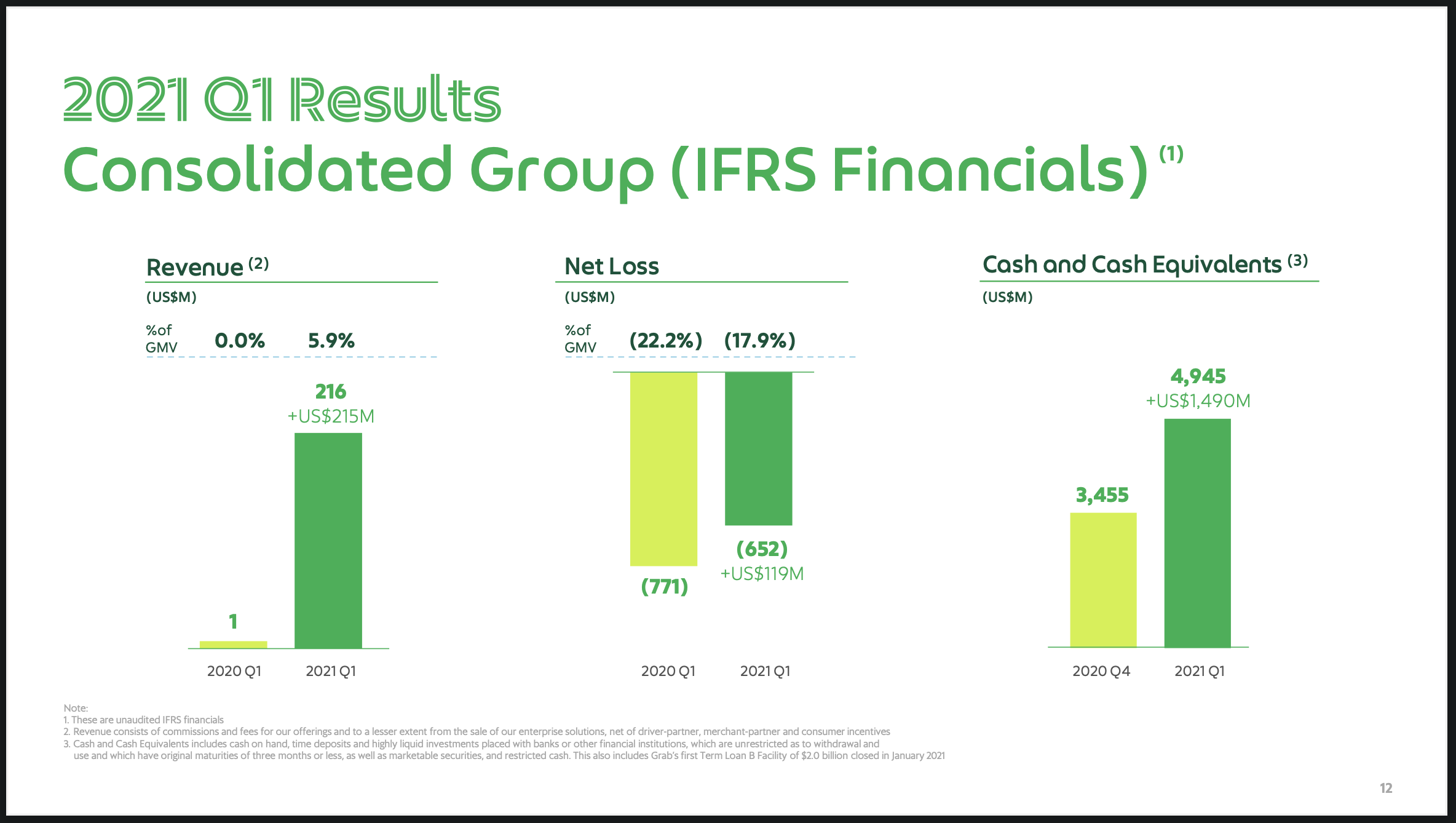

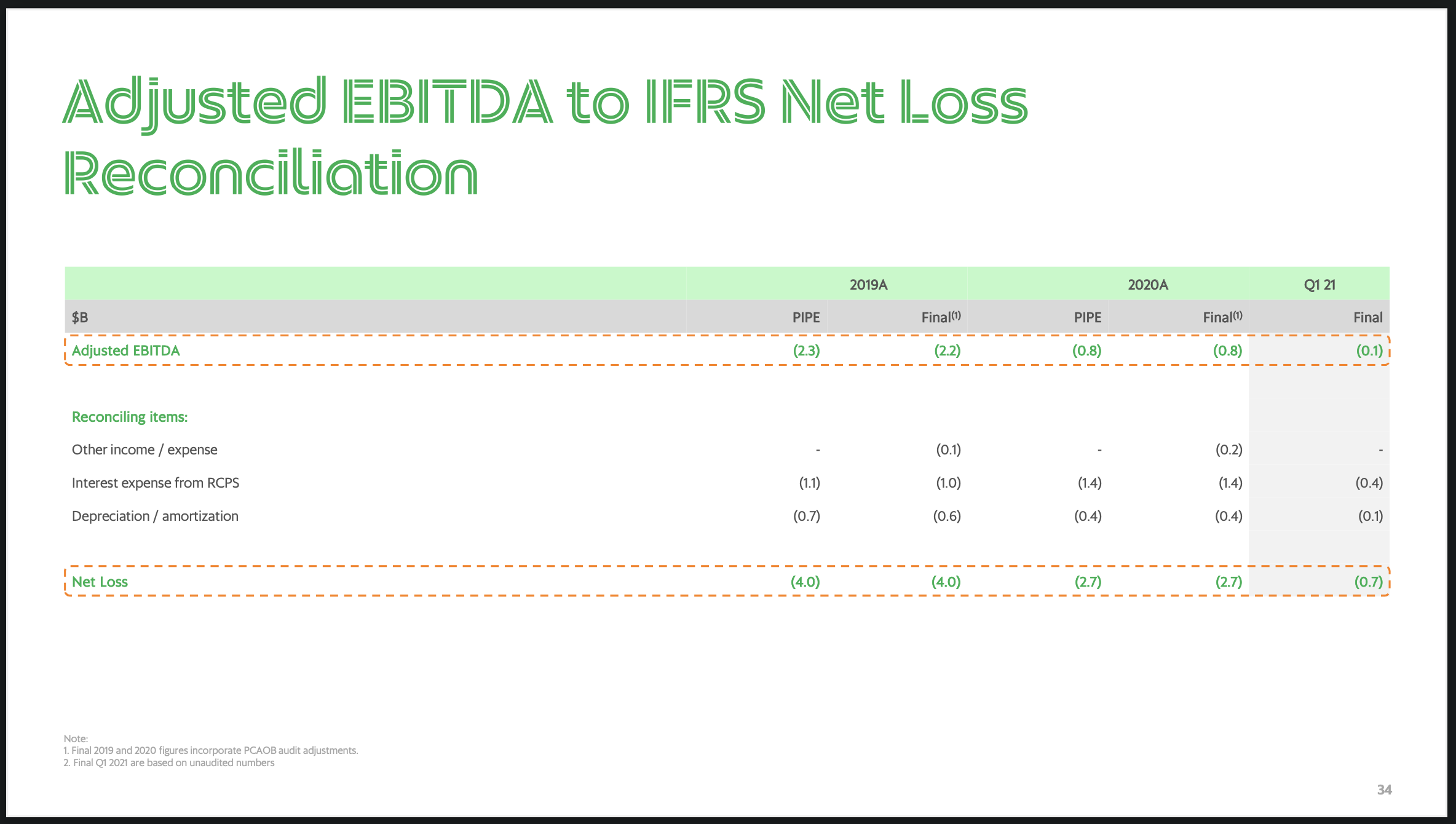

The company incurred US$652 million of losses in Q1 2021, which seemed to be a big amount. However, this might not be a concern for them because:

- It is in a good cash position, with US$5 billion cash and cash equivalents (see the graph above)

- Most of the losses are non cash items related to the interests due to holders of redeemable convertible preferred shares (RCPS). The following from their earnings’ call presentation should shed some light on the RCPS interest as a percentage of net loss.

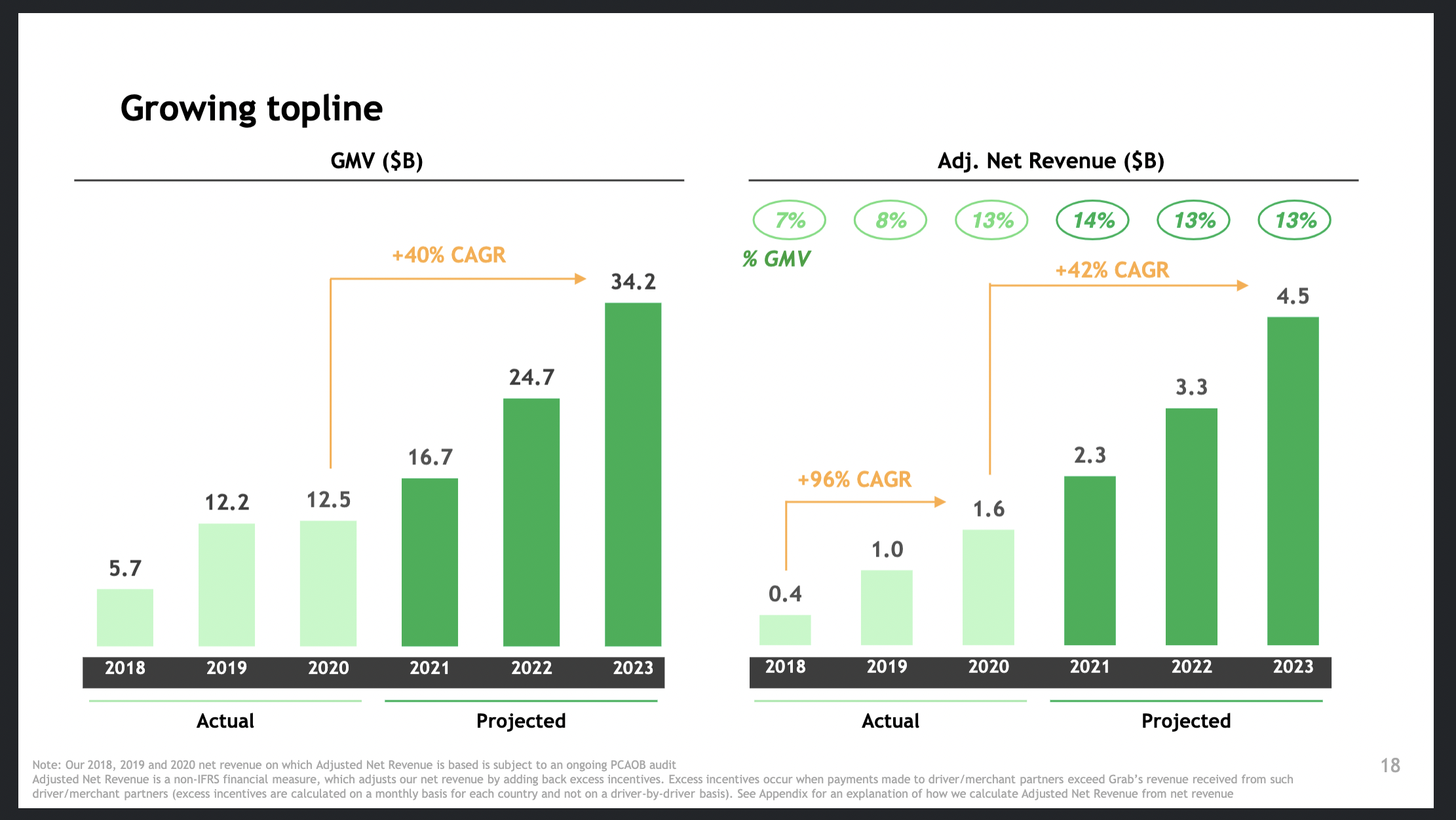

GMV growth in Q1 is lower than expectations, while adjusted net sales, which is basically renamed adjusted net revenue in the new accounting treatment, grew (39%) roughly in line with the projections (42% CAGR) in the PIPE round investor deck. Do note that the “Adjusted Net Revenue” in that deck has been restated following the accounting treatment change:

Grab’s eyebrow-raising listing valuations are based on such projections – so the company will need to consistently deliver the growth. The key is how it manages each of the business segments they are in.

How about the business segments: ride-hailing, deliveries, financial services etc.?

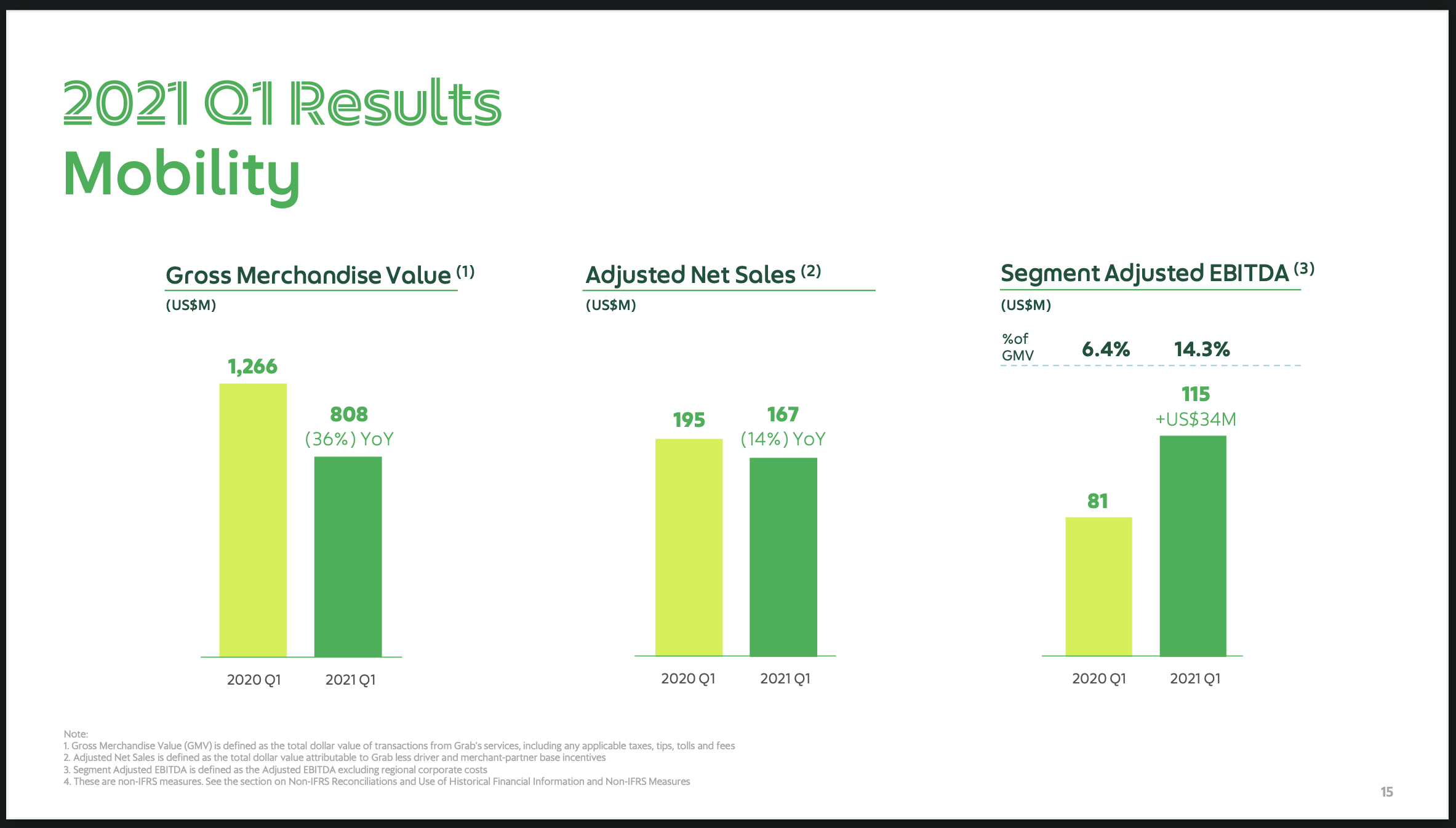

Ride hailing, expectedly, took a hit during the pandemic-induced movement restrictions, with GMV declining by 36% year on year.

However, profitability of the sector actually increased quite a bit, with segment adjusted EBITDA reaching US$115 million. We believe that the platform fee levied on consumers since mid last year played a big part in this.

If the movement restrictions are lifted – they eventually will, we just do not know when – this could become a good cash cow for Grab, as it leads across the region.

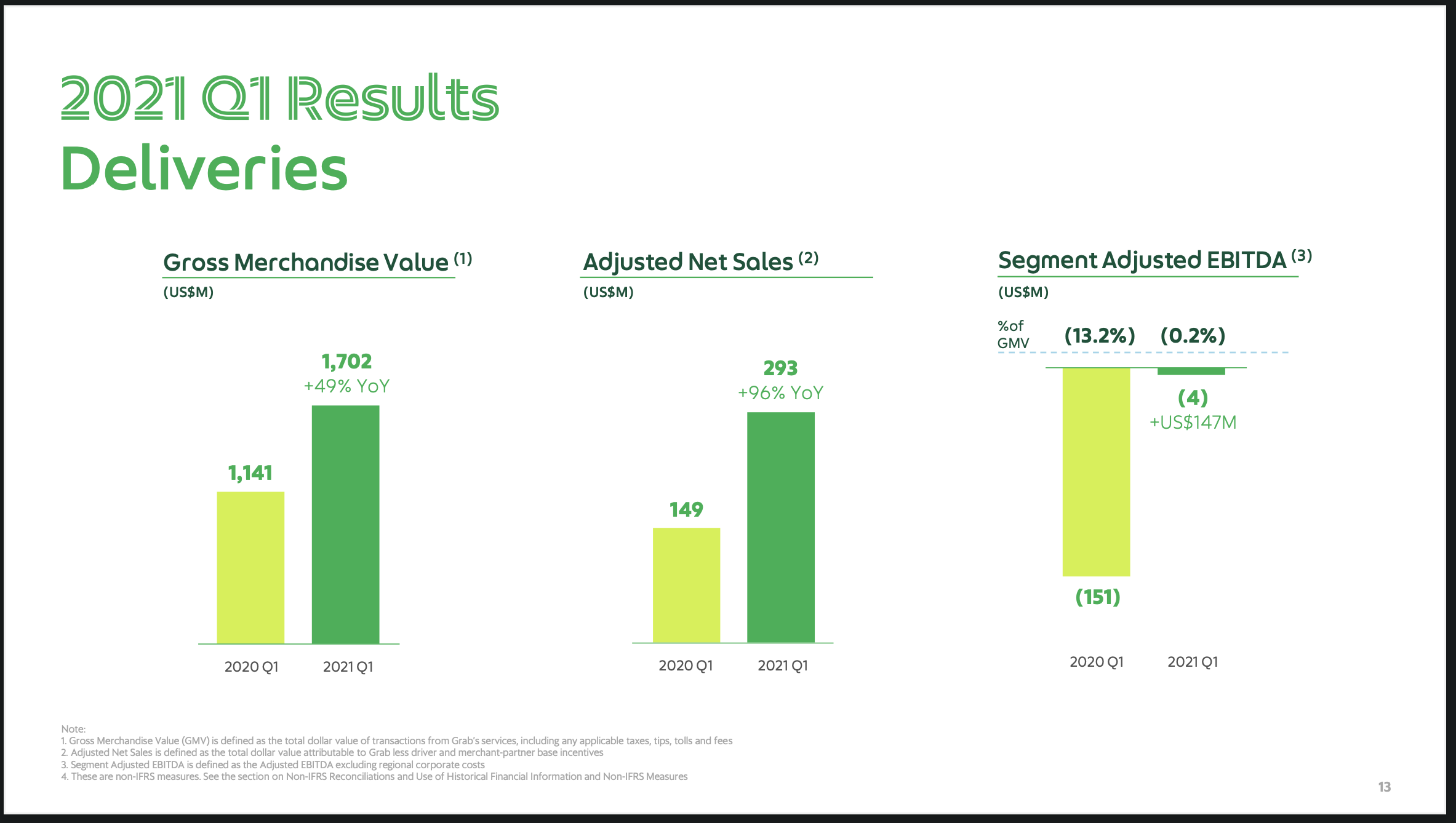

Deliveries grew faster than other sectors, 49% in GMV terms and close to 2X in Adjusted Net Sales terms. Interestingly it is close to break-even point:

It seems Mart, in addition to food, has become a key growth driver for Grab’s deliveries. Grab claimed that Mart has grown 36X in GMV terms year over year. There are no details about the percentage as total deliveries.

Since they only really starting pushing for Mart last year, this increase probably came from a low base and might not be very meaningful. Another reference indicator in the Q1 release was quarter over quarter (Q4 2020) growth of 21%.

This area has become competitive in many markets, where rival foodpanda (part of Frankfurt-listed Delivery Hero Group) has made significant investments as well. It is interesting that foodpanda claims Asia-ex-China leadership (the group has operations in Japan, Korea, Taiwan and Hong Kong, amongst others), but not Southeast Asia.

In the meantime, Grab has removed HappyFresh, which it owns a minority stake, from its suite of offerings from the Grab app, and taken things in their own hands. Although HappyFresh has recently raised $65 million, we are a bit sceptical about its prospects in the stiff competition.

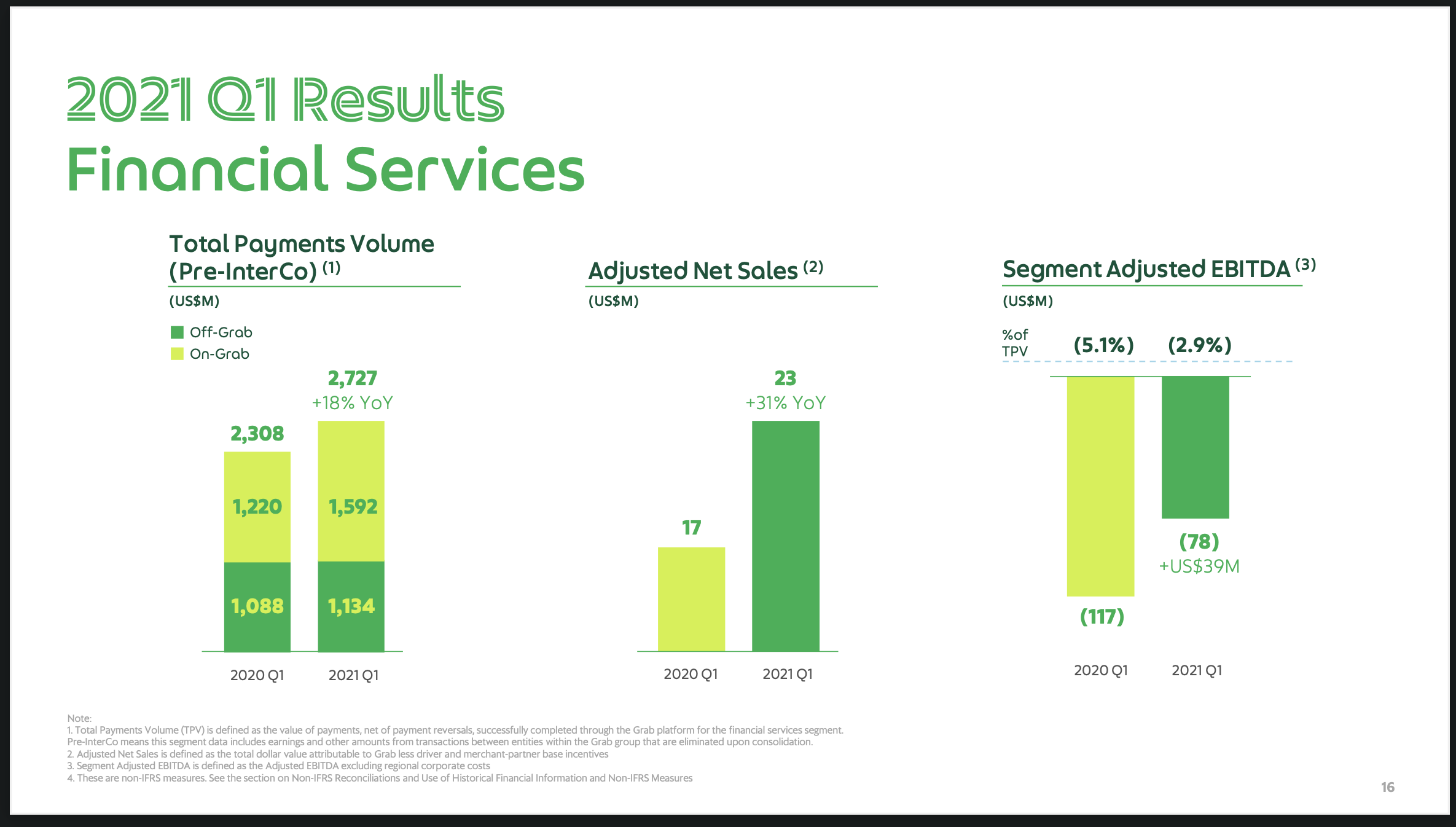

In financial services, while on-Grab payment volume grew about 30%, off-Grab payment volume (those payments done not through Grab app) remained stagnant.

While Grab has not released any details – we feel that this might be related to the movement controls across the region, where spending on offline merchants has probably taken a hit. If the situation continues, Grab needs to get more online merchants to accept its payments to restore off-Grab volume growth.

That probably explains why Grab released information about their partnerships with Adyen and Stripe, two payment gateways which list GrabPay or GrabPayLater as payment options.

A situation not reflected in Q1 results is that Tokopedia might have to divest OVO shares after its merger with Grab rival GoJek. The outcome of this might help Grab gain more control of OVO. Especially that according to new Bank Indonesia (the Central bank) rules effective 1 July 2021, foreign shareholders can own up to 85% of an Indonesian payment service provider.

Overall, financial services occupy a very small part of Grab’s net sales, and contribute to the most of its losses. It is a hyper competitive environment – after listing, Grab will probably need to invest more aggressively in this sector.

We do not have visibility over the lending and insurance businesses, the latter of which has made frequent appearances in Grab-related news releases.

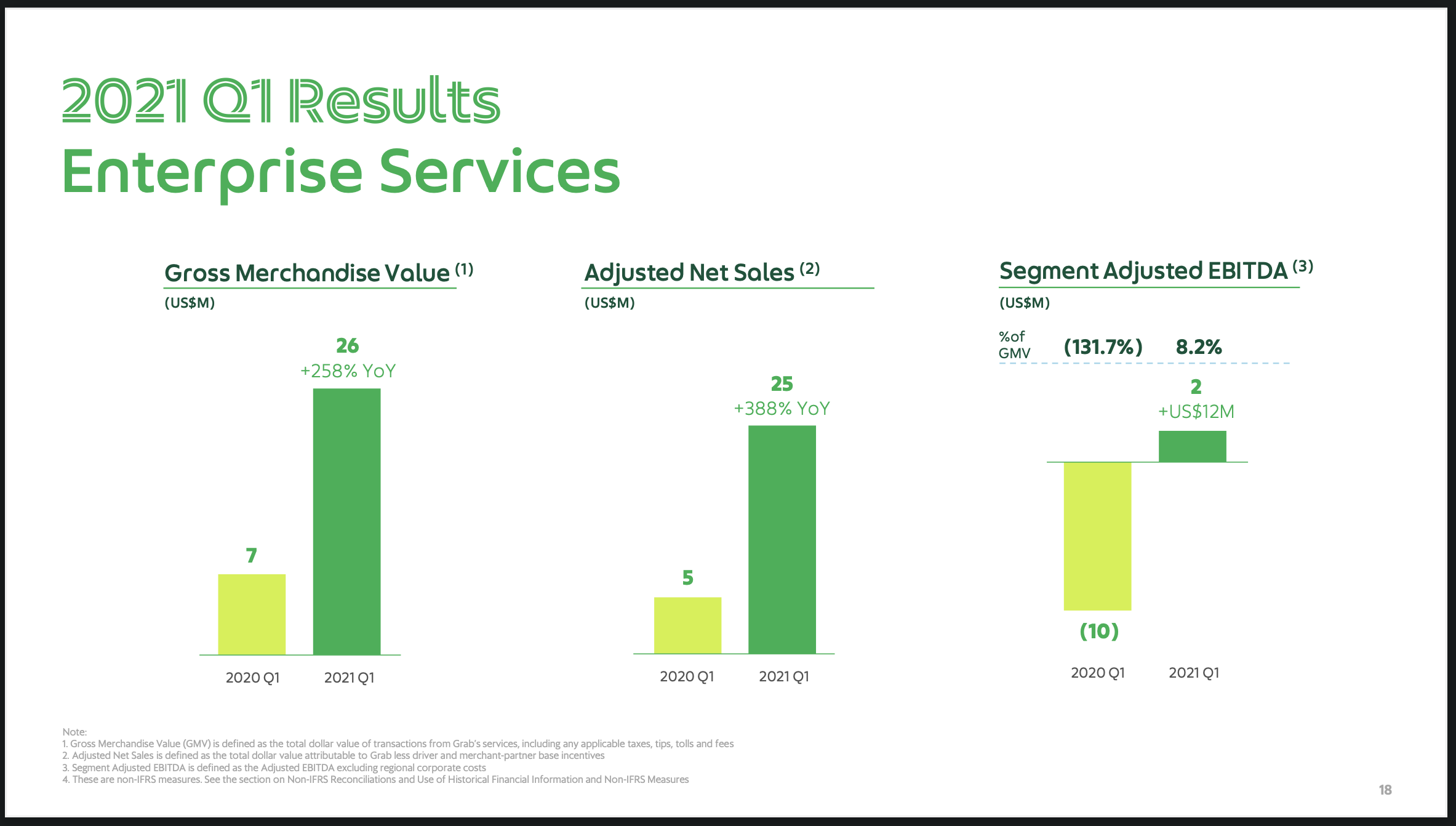

An interesting segment which nobody probably paid attention to previously is enterprise services, which comprises Ads, Maps, and Grab Defence – a fraud and risk solution.

While we are not sure whether it is intuitive to use GMV to account for the top line transaction value in this instance, it is interesting to see:

- The difference between GMV and Adjusted Net Sales is very small, a sign that this is a healthy segment (no need to split order value with partners)

- Adjusted Net Sales here is bigger than that of financial services, and the segment is profitable in segment adjusted EBITDA terms

Monetising data and its key tech capabilities/systems built during its operations is indeed an exciting growth area worth keeping an eye on.

Is Grab’s public listing on track?

When Grab announced it was delaying its public listing to the fourth quarter, a lot of speculations went around to find out why. “SEC clamping down on SPACs” and “changes in SEC leadership” are some of the most widely circulated speculations.

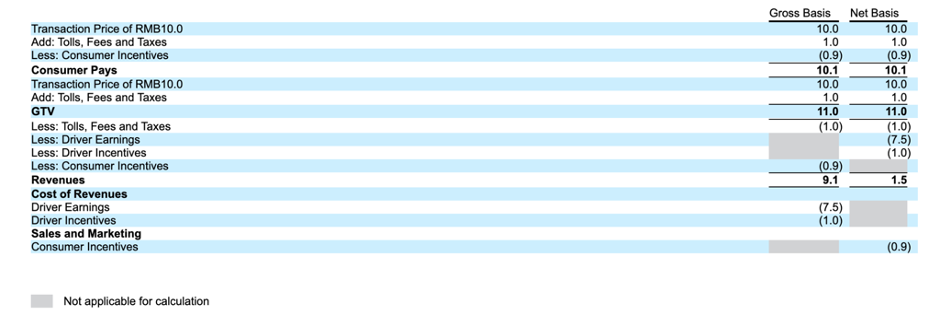

Now it seems to be clear: the revenue recognition has been adjusted (as mentioned above) after SEC talks. Customer incentives, previously recognised as a bottom line item, became contra revenue (top line item).

As a result, many segments in Q1 2020 recorded negative revenue, which aggregate to arrive at the $1 million total revenue mentioned above.

We have looked through a number of comparable companies – and only DoorDash takes this approach.

Uber and Sea Group either do not account for, or only account for partially, customer incentives in its revenue calculation.

Didi, China’s ride hailing leader recently hammered by the government, recognises revenue at “gross basis”, which means it did not deduct driver earning and driver incentives. As a result, Didi’s revenue numbers will look 6x higher.

Peter Oey, Grab’s CFO, said upon the release that Grab’s revenue figures were “more on the conservative end”. Investors will need to account for all these differences to compare the companies effectively (a big headache, we know).

Grab’s IPO (sorry listing through SPAC merger) process otherwise looks to be on track.

What will happen next, after filing of form F4:

- SEC will review the form – which might take up to 2 months;

- After F4 is finalised, AGC will call for a proxy vote by shareholders – they need to give 21 days advance notice;

- If the vote passes, which it highly likely will, Grab can become a public listed company within days

Of course, things might happen during the process – but the Q4 2021 timeline Grab founder Anthony Tan gave in a previous interview seems to be feasible. Looking at this timeline, it seems the process will complete in November.

The continued (and rather unfortunate) pandemic situation should give its deliveries business further tailwind. Grab, as a public company, will still have a lot to deliver, notably in the financial services area.

However, Grab, as a public company, will have more resources to tap into to deliver the growth in segments in sight, as Sea Group and foodpanda did in 2020.