One of the major pillars of Singapore’s economy has always been logistics. Singapore has prided itself in becoming a key regional (at times global) hub for many multinational brands since early 1990s. But in recent years, many brands have migrated their hubs to Singapore’s neighbours; Malaysia and Thailand. This is largely driven by cost of real estate (i.e warehouse) and cost of manpower; Compounded by the lack of manpower for operations in Singapore. The other trade and tax initiatives introduced recently by Malaysia and Thailand are also contributing factors. Besides, both countries have a bigger domestic market, making it more compelling for these brands to reposition.

However, not all is lost as the eCommerce sector is only in its early stages in South East Asia (SEA). Singapore can revitalise its position as a key gateway and hub to SEA, with the correct niche focus.

Regional Government Partnership

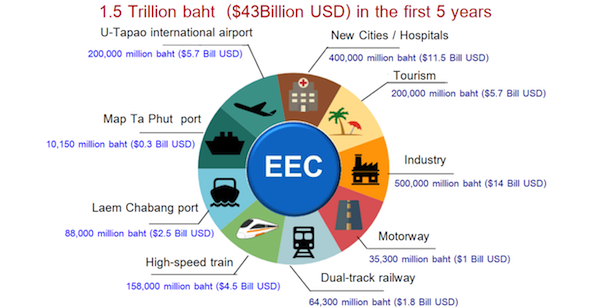

Malaysia’s and Thailand’s government have partnered with AliBaba for the development of Digital Free Trade Zone (DFTZ) and Eastern Economic Corridor (EEC). Many saw this as a massive blow to Singapore’s eCommerce logistics hub ambition. Especially after the development of SingPost’s Regional eCommerce Logistics Hub and SATS redesigning its former mail terminal to focus more on eCommerce.

With DFTZ and EEC, we see potential of splitting the 650 million population in South East Asia (SEA) into 2 key sub-regions. DFTZ serving the Nusantara region (Malaysia, Singapore, Brunei, Indonesia, eventually Timor Leste and potentially Philippines). EEC fulfilling the market needs of Indo-China consisting of Thailand, Vietnam and developing SEA countries like Myanmar, Laos and Cambodia. Through its proxy Lazada, it is speculated that AliBaba will be strategically using the DFTZ and EEC as fulfilment hubs to bring Chinese merchandise closer to the market with suspended import duties and tax. This would reduce cross border logistics cost from China (and pressure on capacity during peak period). At the same time, simultaneously improve customer experience with reduced turnaround time. To be fair, AliBaba in addition to bringing Chinese merchandise in, is also looking at acquiring more SEA merchants. However, it is a pity many SEA brands are not export ready.

Here lies the potential for Singapore to offer a differentiated value for the eCommerce channel. DFTZ and EEC’s key advantage would be bringing down logistics cost for Chinese products (typically USD40 or below). Singapore provides an alternative solutions for brands at the other end of the cost spectrum. Rather than trying to attract the likes of AliBaba, Singapore should be focusing on attracting mid to upper brands (predominantly from US, EU, JP and KR) to leverage on Singapore as a gateway to SEA. Many established (and mostly global) brands are moving to a Direct to Consumer (DTC) model for their eCommerce channel and see SEA as a key market. However, perceived concerns on logistics cost and customs still linger.

Logistics Cost

Warehousing (cost of fulfilment) and last mile are the 2 major costs of logistics. Last mile includes cross-border B2C fulfilment. Most would argue that both Malaysia and Thailand represent a better cost option for warehousing. However, the efficiency and productivity gained with Singapore’s adoption of technology should not be ignored. For example, YCH’s Supply Chain City. Cost sensitive brands may overlook Singapore as an option for a regional hub. However, higher value brands will find Singapore a viable option.

For a regional hub to work, connectivity to market and competitive pricing is essential. Singapore’s airfreight connectivity (from a frequency and capacity point of view) remains the best in the region. This allows service providers to offer competitive B2B inbound rates (via all mode of entry) and more importantly, competitive B2C cross-border last mile (via air) into the other major 5 in SEA (ID, MY, TH, VN and PH).

When doing an apple to apple comparison on freight connectivity, Singapore Airlines via Changi Airport still leads quite significantly in terms of capacity. Especially wide body aircraft flying into Singapore and Intra-SEA. This results in lower freight cost (at times up to 40% to 45% cheaper) compared to Malaysian Airlines via KLIA and Thai Airways via Suvarnabhumi.

Hangzhou based Cainiao Network Technology Co. Ltd., the smart logistics subsidiary of AliBaba, signed a strategic partnership with Singapore Airlines. Aimed at leveraging on the airlines’ network to expedite cross-border eCommerce deliveries. A similar partnership was also signed between Cainiao and Emirates, which is regarded to have similar capabilities as Singapore Airlines. Good cargo hub, high frequency and capacity into sub-regions translating to competitive pricing.

Interesting to note, as part of the airlines’ restructuring effort, SIA Cargo will no longer be a separate entity. All cargo space from the different airlines (i.e Singapore Airlines, Silk Air and Scoot) under the group will be centrally managed. They too have recently introduced an eCommerce team within the airline. An important indicator on how serious they are in being a leading service provider for the global eCommerce cross-border market, estimated to be USD1 Trillion by 2020.

Customs & Air Freight

With the exception of Singapore, and to a certain extent Malaysia and Brunei, import entry to the rest of SEA has always been a challenge. This applies to air, land and sea shipment for both B2B and B2C. However, over the past 2 to 3 years, SEA countries have setup clear import regulations with regards to cross-border eCommerce. Though at times execution on the ground may still be slow, rigid or too flexible (depending on who you know). In general all countries have a clear de minimis regulations with explicit import duties and tax structure. This has levelled the playing field with regards to managing customs and allow service providers to compete based on service capabilities. Supply chain connectivity is where Singapore has an edge over its neighbours.

In addition, 2 of the biggest and most critical SEA markets, Indonesia and Philippines have no direct land connection to the rest of SEA. Connectivity via air into their major cities is essential to ensure efficient service levels when managing a regional hub with centralised inventory servicing the SEA market.. A key factor of customer experience. More importantly, the de minimis rule for eCommerce is only applicable for entry via air. Therefore, in order for a brand to utlise the de minimis rule, importation via air is the only option.

Execution (Start-up Style)

There is an opportunity for Singapore to revitalise its position as a key regional (and global) hub for eCommerce. To position itself as a channel for higher end brands that appreciate the unique value Singapore brings to the table. To succeed, Singapore needs to work hand in hand with eCommerce solutions providers (especially logistics start-ups) to highlight its’ value and to attract international brands and eCommerce platforms.

Similar to a start-up, Singapore needs to focus and execute these actions quickly. Time is of the essence to avoid being blind-sided by potential threats vying for the same market (though it is big enough). Putting aside the airport capabilities in managing transshipment cargo, regional budget carriers such as Air Asia Group (of Malaysia) and LionAir Group (of Indonesia) are dark horses which can throw a spanner into the works. They have the capability (and potential ambition) to be strong movers and shakers. Potentially disrupting or hindering Singapore’s hope in becoming the region’s eCommerce gateway.

To Singapore, execution is key for it to be successful in a dynamic eCommerce market. The old Singapore blue print should make way for change. Singapore can revitalise its positioning (and aspirations) as a key strategic eCommerce logistics hub.