")

Since we released our Fintech in Indonesia report in 2019, many people have shared their insights about the industry with us. Whilst fintech lending has been one of the fastest growing fintech business in the last few years, we observed that digital banking in Indonesia was starting to take off in 2019. Acceleration of digital banking in 2020 was opportune, strategic, and very well-timed.

In our ”Momentum Works Rise of Digital Banks in Indonesia” report, released in April 2021, we share our perspectives on the opportunities, development, regulations, competitive landscape and key dimensions to winning (and more importantly – retaining) consumers.

In our report, we seek to answer the following key questions:

- What is a digital bank? How different is it from online banking?

- How has the industry grown? Where is the room for growth?

- How big is the user pool and what is their demographic?

- Who are the key players to watch?

- What consumers look for and how are key players performing?

Below are some key insights from the report:

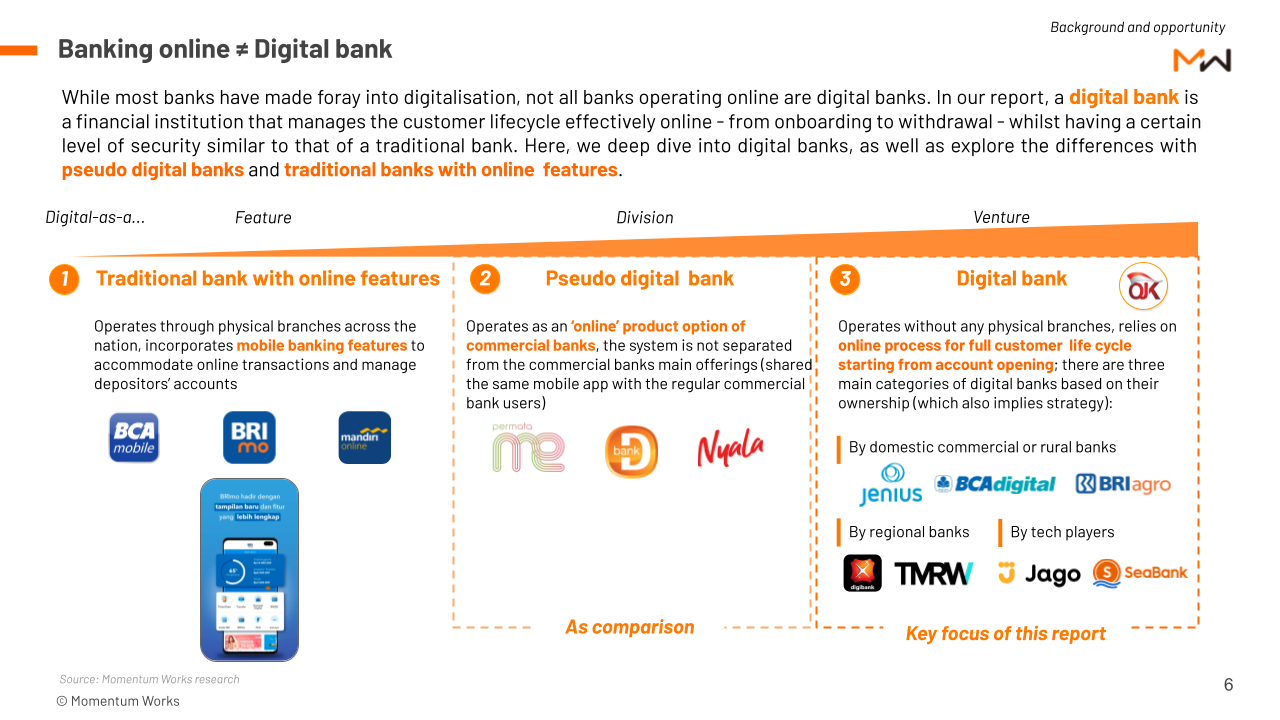

1. Traditional banks with online banking are not digital banks.

There are three types of “Online banking” services: Traditional banking with online features, pseudo digital bank and digital bank. We make it clearer in the report the difference between these 3 types of banks.

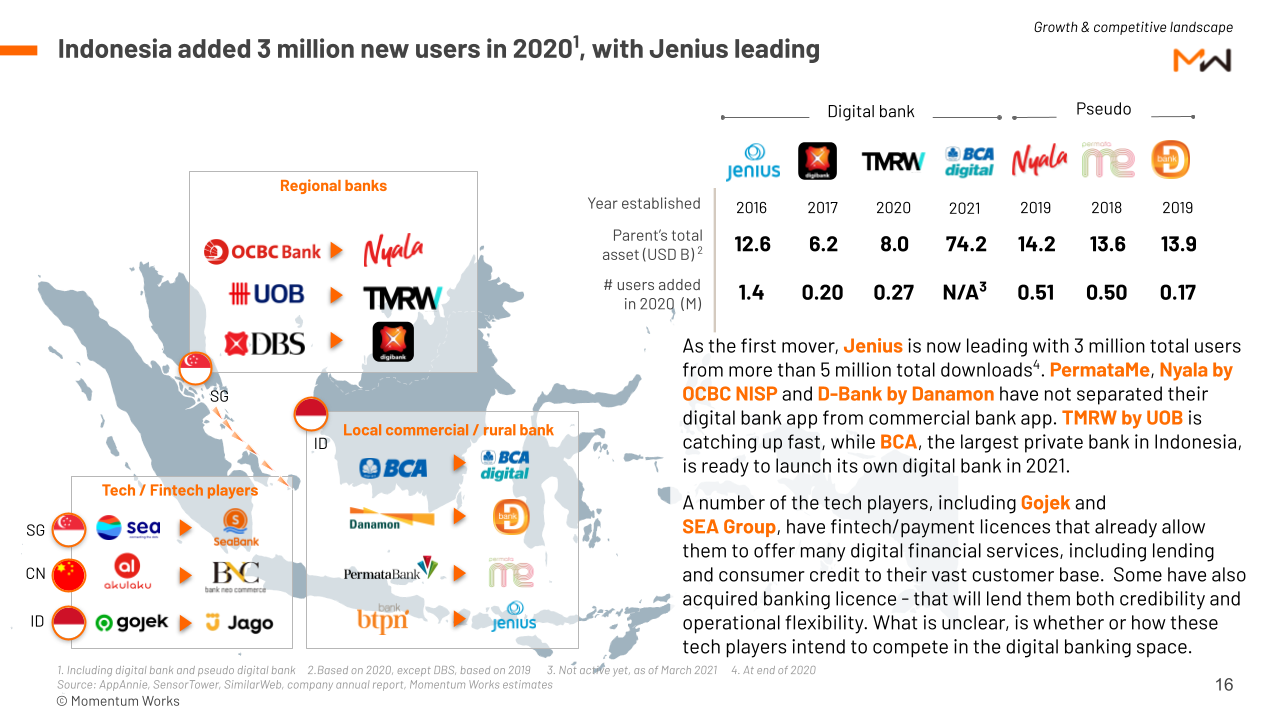

2. Indonesia digital bank app downloads grew 7% in 2020, but new players strike hard and fast, at 2-5x growth.

Newer players like OCBC Nyala and UOB TMRW are emerging strong and fast, at 2-5x of 2019. UOB TMRW in particular, on aggressive growth due to its strong appeals to the younger generation, through unique gamification features (i.e.: You can watch your virtual city grow as you save).

One interesting observation was that current digital bank penetration remains among the more tech-savvy banking population, and that many Indonesia digital bank users tend to download multiple digital bank applications and explore around. Whether these users would stay would be another question.

3. We estimated that there were 3 million new users in 2020, led by Jenius. Deep-pocketed players have joined the fray.

To understand competitive landscape of digital bank in Indonesia, we observed that there are three types of players, with different expertise, motivations and resources:

(a) Local commercial / rural banks (Bank Danamon, Permata Bank, Bank BTPN) know the local banking scene; want to get their feet into the game and leapfrog other conventional banks peers before disruption happens.

(b) Regional banks (OCBC, UOB, DBS) have trusted, established brands; look to apply regional capabilities and grow in Indonesia.

(c) Tech / Fintech players (Sea Group, Gojek, Akulaku) have customer base, merchant networks and data capabilities; look for additional pillar to strengthen their ecosystem play.

4. When choosing digital bank, consumers in Indonesia weigh products’ friendliness, price, features and customer service

Often, managing both high velocity growth and capabilities expansion in these key dimensions is a challenging balancing act. Case in point, we hear first-hand users and avid supporters of Jenius leaving the service as the product does not seem to be able to cope with the rapid growth, with user experience deteriorating over time (i.e: extremely slow to load).

Digital banks will need to prioritise value propositions that serve actual customer needs without being distracted by the noise in the market.

Our perspectives

Digital banks in Indonesia have great potential to accelerate: There is a huge underlying market), with significant room for penetration, accelerated by an increasingly competitive landscape, receptive population and supportive regulations.

However, they will need to keep their eyes on the long haul to establish its share in the market in a sustainable way.

With different types of players joining the fray, the race is just starting to get more interesting.

In the end, it is again, survival of the fittest. Ultimate gainer will be users and the economy.

If you are interested, you can get a copy of the full report here

[1] Digital bank and pseudo digital bank