")

Following the publication of our Food Delivery Platforms in SEA, we held a number of online briefings with investors, F&B industry practitioners, other relevant stakeholders and media to deep dive into this industry. Here are some of the key questions asked during these sessions, in addition to what we have already shared in previous posts here and here:

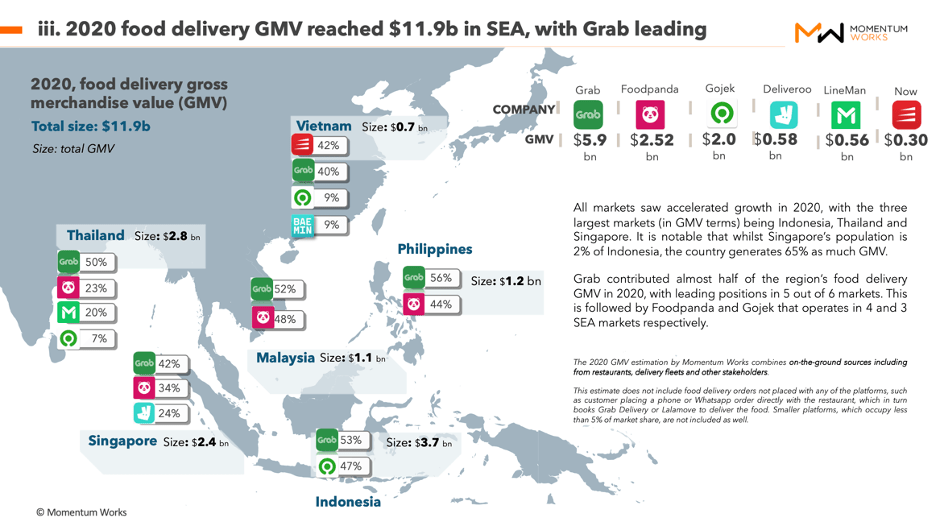

- Why does Singapore have such a high GMV compared to Indonesia?

Singapore is an outlier when assessing the Food Delivery GMV in SEA. Whilst Singapore’s population is only up 2% of the population of Indonesia, it’s food delivery GMV of US$2.4bil is 65% that of Indonesia.

A few reasons to explain this – Singapore had one of the strictest lockdowns in 2020 for two and half months. During those times, restaurants were strictly not allowed to open for dine-in, non-essential workers worked from home, and mobility was limited.

With almost 100% of Singapore residents urban, and good infrastructure including digital payment adoption, the city state rightly commanded such a high food delivery volume in 2020.

-

How will the food delivery market look like post Covid? Do you expect a drop in usage?

In Southeast Asia, there is no shortage of consumers, no shortage of riders, and no shortage of restaurants. Besides, infrastructure such as digital payment is growing fast.

We expect consumer behaviour in the region to have been permanently changed during the pandemic, taking the reference of SARS permanently changing people’s ecommerce behaviour in China. The total food service market numbers in the report will give us a useful reference point off the theoretical upper limit of the market. You can reference that to the percentage penetration of food delivery in total food services in China and US to get an estimate. The same way as we benchmark ecommerce as a percentage of total retail.

Besides, once critical mass is achieved, additional growth can be done in a much more cost effective way (operations wise). Adjacent business models are also possible as a result. Cloud kitchens, new F&B brands, food delivery enablers (like ecommerce enablers) etc.

-

What potential futures do you see in 2024 and 2028 in SEA and SG specifically? Who are the players and are they only delivering food or will they have moved to “quick commerce”?

Predicting numbers ahead was not part of the report, but we could conduct a scenario analysis. While we do expect continued growth, it is important to map out the factors that could impact the pace as well as the shape of that growth.

For example, in countries like Indonesia and the Philippines, the pandemic will still last for a while before it is brought under control – but we do not know the timeline. That affects the consumers’ behaviour.

In addition, another uncertainty is the timeline for investors. The public market is very good for the second half of 2020 and will probably remain positive for the next 18 months. That gives players a good way to raise more capital to accelerate the growth – how will the capital market behave after that is anyone’s guess.

Overall, we are quite optimistic about the macro trend in this market. As for the ‘quick commerce’, we believe the players will move into delivery of anything: food, groceries, general merchandise. Meituan is already doing that (in a promising way) in China. If you can get most things you buy delivered to you within the next hour, would you still wait for 2 days (or often, 3-5 days), as traditional ecommerce players process the order, send to fulfilment centre, sort, and deliver?

-

How the platforms differentiate themselves- in winning customers and merchants? How important are membership and loyalty programmes?

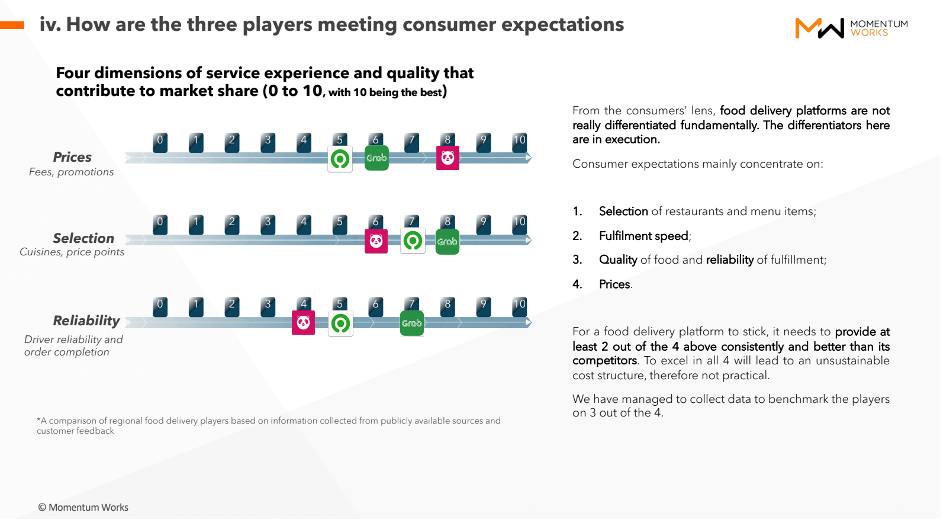

Customers care about four things: selection, speed, quality/reliability and price. Restaurants care about, primarily, platform’s ability in bringing in more customers, and subsequently an affordable commission level.

As far as the customers’ concerns, we have done an on the ground survey about three out of the four metrics (below). Membership and loyalty programmes are important retention tools, but they only work once the platform has successfully addressed at least two out of the four concerns:

-

What is your view on the pure play players- especially from Europe and America ?

Pure play players work well in niche areas where average order size is higher than the general market and specific requirements are needed (for example, Mainland Chinese cuisine restaurants targeting customers originally from Mainland China in Singapore; or specialty Japanese food delivery in Bangkok). However, in general pure play platforms targeting the mainstream markets in Southeast Asia might be a challenging play. For the reasons mentioned in the report: they find it hard to keep the customers sticky to justify the acquisition costs as well as infrastructure investment, in markets where order value is low.

-

How do you think Grab could beat Gofood in Indonesia? And will Foodpanda re-enter Indonesia?

Grab is already beating Gofood in Indonesia. If you look at the market share on the ground, Gofood probably had more than 90% back in 2016, and by our estimates for 2020, it has reduced to less than 50%, with Grab taking the slight majority.

The larger warchest to invest was a key factor but not the only factor. While Gojek attracted some of the best tech talents from Indonesia, Grab undoubtedly has more professionalism and discipline in execution – in areas of product, marketing, operations as well as government relations.

Its regional presence, and leadership in some of the higher value markets in the region, also contribute to its ability to invest in Indonesia for the longer time, while maintaining investor confidence in the company.

We can’t say about Foodpanda’s plans, but entering Indonesia now would be a very costly (and long term) exercise that the company needs to be very careful about, having not exactly proven its business model elsewhere.

-

What’s your opinion on how Doordash is beating Uber Eats in the USA? And what did they do right? And what and differently versus what Uber did?

We don’t know enough detail, or whether DoorDash is indeed beating UberEats in the US. One advantage Doordash has is its Chinese founder, who is still running the business. The company would have no problem tapping into the learnings of Meituan and the market in China, where fierce competition forces players to constantly evolve, and innovate. The fact that DoorDash does not have global markets, or ‘long term’ projects such as autonomous driving, would also contribute to its advantages over Uber.

-

Now under Shopee is currently number one in Vietnam. If Shopee’s food delivery business enters Indonesia or other countries, will it be possible to overturn Grab’s leading position?

In theory, it is possible. If Shopee enters other markets in the future, it will be a strong opponent of Grab. However, Grab has a strong market leadership across Southeast Asia, and good access to capital, having its recent bond issue oversubscribed and IPO in progress. The question for Shopee, the public market darling at the moment, is amongst all the possibilities (including financial services, and Latin America market), which should be its priorities.

-

In Indonesia, Shopee and Tokopedia have Shopee Food and Tokopedia Nyam. How do you see the competition for food delivery between Gojek, Grab, Shopee, and Tokopedia in Indonesia? How would the Gojek-Tokopedia merger affect the competitive landscape?

Indonesia is undoubtedly the largest market in Southeast Asia, which hosts the best long term potential. It is also a complex market that requires a lot of strategy, execution and patience to win over.

We expected Grab and Gojek to consolidate, which would allow the merged entity to focus more on growth than competition. However, this seems not to be the case, with the Gojek-Tokopedia tie-up that’s rumoured to happen.

We believe that the Gojek-Tokopedia merger will not change the competitive landscape, as both companies will continue to lose market share to Grab and Shopee. We can hardly see any synergy between the operations especially when it seems to be a holding company with the two operating still relatively independently.

The tie-up, however, will create a good story to the public market and no doubt some investors will buy into it. That said, note that Shopee is already part of a publicly traded company, and Grab is also heading or IPO. If the leading players are still growing in market share, why should investors bet on the next players?

-

Many platforms in Indonesia start to release cloud kitchens (Grab Kitchen, Dapur Bersama GoFood, etc.). How do you see this trend, will this be a significant trend for the food delivery ecosystem in the future especially in Indonesia and Southeast Asia?

In Indonesia there is no shortage of restaurants, so cloud kitchens are complementing existing supply while allowing owners/entrepreneurs to adapt online delivery with a different cost structure.

Cloud kitchen also allows testing of new culinary brands/concepts without having to rent a physical space and renovating it (which cost both money and time). Successful brands/concepts can be expanded while those not successful can be retired easily.

This only works when the delivery platforms become big enough with customers as well as delivery infrastructure. Experiences in China have also proved that.

-

In Indonesia, food delivery gives new opportunities to lots of new F&B players. For example, there’s Hangry, where they focus only on food delivery and they got some investment from a few famous investors. Will this trend also be the new trend in Vietnam, Philippines, Malaysia, Singapore, etc.?

Yes, we believe so.

-

In Singapore, there seems to be a bottleneck of rider supply. Is that an obstacle to the industry’s growth?

That is a problem specific with Singapore, where there is very limited supply of labour. Note that during Covid as many people who gave up previous jobs jump into food delivery, the rider supply issue is alleviated.

For the long term, it requires food delivery platforms to increase efficiency (and utilisation) instead of counting on recruiting more riders. That would also help the platforms test new systems and operational procedures that could be adapted into other countries.

-

Why would the players, including Grab and Gojek-Tokopedia, rush to IPO now while profitability is still not proven? In your growth, is growth or cash flow more important?

First, we assume the question is actually comparing growth versus profitability, instead of cash flow (which is a different concept). At this stage, growth is more important than profitability – because the market is not yet saturated.

A key capability of growing a tech company is tapping into the right investors at the right time. Currently as well as over the next 12-18 months, public equity market is on a good run with both ample liquidity and good sentiment on Southeast Asia tech (see Sea Group’s stock performance). It makes sense to tap into this opportunity to power further growth.

-

With the increased demand in food delivery, will it be making restaurant food just for delivery? How should restaurant chains respond to that?

Food delivery, same as dine in, is a distribution channel for food services. As we discussed in the report, restaurant chains were the first to adopt food delivery, even ahead of food delivery platforms.

The question here, though, is that each restaurant chain in the region is different in brand recognition, customer appeal and growth strategy. They should all see food delivery as a key component of that strategy, especially now the infrastructure is ready.

Whether tapping into the platforms, or managing their own delivery (maybe with Lalamove), or both, is a question that the leadership needs to figure out.

There are now more growth opportunities for restaurant chains if they tap into the delivery trend well.

-

The data looks impressive, how to get the data sources that you use to process the analysis and findings in this report, especially data about players?

We are not a market research firm, so we did not take their usual methodology based on subscribed databases and trade/customer interviews often facilitated by third parties. Structured data is scarce and the market changes very fast (for example, Baemin’s rapid expansion in Vietnam in 2020).

Instead, we did lots and lots of on the ground interviews, with people including restaurant chain operators, logistic providers (fleet owners, riders, and logistic platforms), customers and other stakeholders. We extrapolate the data obtained from different sources and then verify with the stakeholders we have interviewed, with calibrations afterwards.

As we are practitioners in tech/internet, and some of us used to work in the exact industry. We are glad that we have an existing network that we could quickly tap into, and that introduced us to even more relevant stakeholders.

We are, in fact, taking the same approach with all our sector focused reports. Do look forward to more numbers and reports coming from us in 2021. 🙂