Is there ground in the region, and who will win?

As Lyft and Uber are both becoming public companies, we are seeing a lot of chatter about the business model of these two ride-hailing juggernauts. A key point is whether the moat for them is strong enough, and the business model sustainable. While Uber’s delivery business is seeing some good results, neither has become the ‘superapp’, encompassing many daily services to the consumers.

Concurrently, Grab and Go-Jek, the two Southeast Asian unicorns, are aiming to build their superapp in this region.

This detailed analysis will examine whether that is feasible and whether emerging markets, in particular, Southeast Asia, are fertile ground for superapps.

Let’s start – what is a superapp?

Superapp, although the term is rarely mentioned, is a common (and probably unique) phenomenon in China. WeChat, Alipay, Meituan are all examples of that: users just need to download one app to enjoy many functions – including social, payment, ride-hailing, food delivery, ticketing etc.

The power of superapps to their owners is obvious: a successful superapp not only increases the lifetime value as well as the loyalty of users but also builds a strong moat around its core business, in theory lowering the pressure of competition.

Guoli Chen, Professor of Strategy at INSEAD, pointed out: “To many platforms in emerging markets, becoming a superapp is a natural progression for business rather than a choice. Internet businesses need to increase stickiness to consumers, and prevent consumers from switching by offering more value (and thus increase the switching cost).”

A question many have asked us is: “Since superapps are so important for a business, why is nobody doing that in the US?” Aside from Amazon, most US internet giants seem to be pretty focused on their core, be it social, ecommerce, fintech or content.

Why are superapps not hot in the US?

In the US, it seems that consumers still prefer to use different apps to perform different transactions/functions. Google and Amazon are all strong in particular areas.

Facebook – the closest to a superapp in the US is nowhere near what WeChat has achieved in China. Amazon has also tried to move towards the superapp model with multiple offerings through its Prime membership. However, it still does not offer multiple services through one app as an entry point.

We think a few factors are at play:

First, many users in the US gained access to the internet before the rise of smartphones. The landscape was pretty much set when iPhone was introduced: Facebook in social, Twitter in news, Google in search and Amazon in e-commerce.

When people moved their screen time and transactions to smartphones, such user habits and loyalty persisted. In the meantime, Facebook, Google and their counterparts were pretty agile in the shift to mobile, leaving emerging competitors no chance for disruption. Instagram and Whatsapp were both acquired by Facebook, and Snap is facing big uncertainties now – the macro landscape largely remained the same.

Meanwhile, in China, the changes brought on by the proliferation of mobile internet is revolutionary. When WeChat and Alipay were rising, most consumers in China did not have existing habits that needed to change. They are embracing the new functions as they were introduced by these superapps.

In the meantime, hundreds of millions of users were connected to the internet through mobile in just a few years, giving ‘superapp’ a fertile ground to acquire, educate, and retain users.

As discussed, in the US, when the relative position in the market amongst big internet companies is stable with boundaries clear, it is difficult for one to encroach into another’s territory. Users in China would know – because they have witnessed how Alipay has repeatedly failed to penetrate social, and Tencent’s multiple failings in entering ecommerce.

In addition, the average user value in the US – including consumption power and advertising value – far exceeds that of any emerging market, including China. There is still a lot of value to capture for internet giants to capture in their core areas, which are always lower hanging fruits than moving into an adjacent but unfamiliar territory.

Users’ privacy concerns and the role of regulators are also factors limiting the formation of superapps.

Therefore, the US market landscape persists as it is.

How about Southeast Asia?

We believe that Southeast Asia is a much more fertile ground for superapps, compared to the US, for the following reasons:

1、Similarities to China

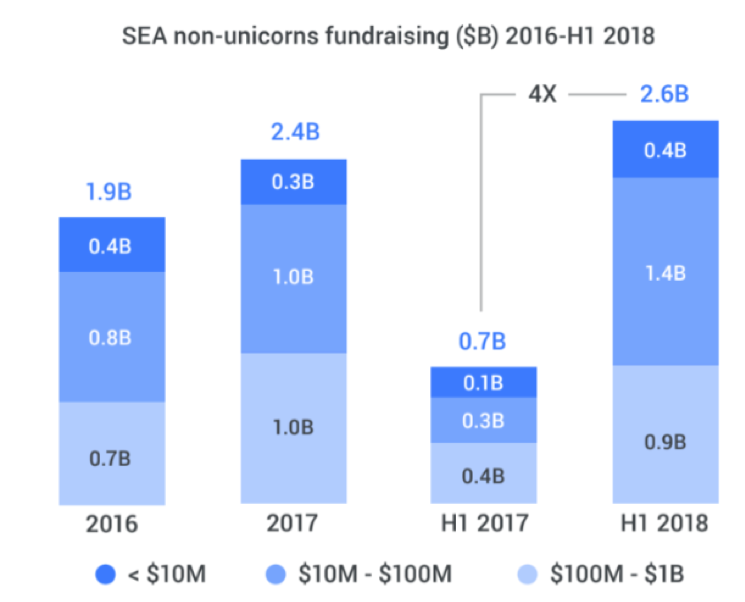

If you treat Southeast Asia as a whole, it is a relatively underdeveloped market. According to the report by Google and Temasek in 2018, the internet economy will reach US$240 billion in 2025, from US$72 billion last year (which was already a 37% YoY).

In other words, the growth market is MUCH BIGGER than existing stock – aside from ride-hailing, no other market has been completely dominated by only 1-2 players. And similar to China a few years ago, user habits are being formed, with largely no pre-existing habits you need to change.

During this phase, it is feasible, and even important, to capture as much ground as one can.

2、Concentration of capital

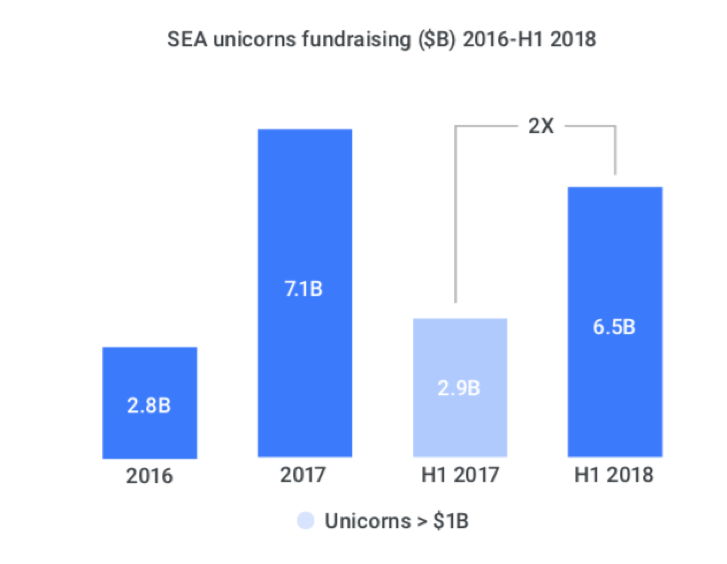

In the last four years, the unicorns in South East Asia had attracted a total of US$24 billion investment, with Grab bagging US$6 billion alone. Capital from the US, China and Japan are generally very interested in making these leading companies grow even further.

Such availability of capital in the short period of time gives the unicorns the firepower and confidence to become superapps.

Also important is that the companies do need to build a strong moat in the market of high growth. If you look at how Traveloka has been fighting the assault of Tiket.com, backed by Indonesia’s largest conglomerate Djarum, you would know.

3,Relatively low user value in the short term

Compared to the US, most Southeast Asian countries offer limited lifetime value per user – Indonesia’s GDP per capita is only about 6% that of the US, and while Singapore is at comparable levels with the US in terms of GDP per capita, its population is less than 2% of that of the US.

Therefore in the short term, it is important to cover more services to capture more customer value. However, do not underestimate the potential of these countries. Indonesia’s GDP per capita is equivalent to China in 2009 – i.e. not that long ago and not that bad at all. With Jokowi’s re-election, another few years of solid economic growth is predicted.

Attempts by leading players

Superapps in China were started by ecommerce, O2O and social companies. In Southeast Asia, ecommerce penetration is still low (and market fragmented). In social, aside from Line’s domination in Thailand, Facebook and its affiliates (Whatsapp and Instagram which are largely non-transactional), are the main players.

It seems now that the ride-hailing companies have the best potential to become superapps. In fact, Grab and Go-Jek are also the most active in that front.

Go-Jek has built a suite of services around its core two-wheeler transport, including payment, delivery, ticketing, moving, and cleaning.

On the other hand, Grab is something different. Aside from ride-hailing, food delivery and payment, which it controls, it has built many other services, including hotel booking, video, ticketing and travel through working with partners.

In the SEA market, ride-hailing, food delivery and payment are regarded as the three core areas of superapps.

“While it is hard for ride-hailing to making a good profit, it generates high-frequency transactions. This is what many other services lack,” says Professor Nitin Pangarkar of NUS Business School. “In comparison, the food delivery business has good prospects for profitability, and the combination of both creates a very good ground for payment services.”

Owning everything vs. building an ecosystem

Grab’s approach is interesting because it does not provide everything on its own but through partners. The hotel booking service is through Agoda, video streaming through Hooq, and ticketing through BookMyShow. The platform provides an entry point for customers while the services are actually provided by ecosystem partners.

Its venture arm, Grab Ventures also focuses on fostering startups whose offerings can be included in the Grab ecosystem.

Go-Jek took a path of owning everything, acquiring MVCommerce, LOKET, Kartuku, Midtrans, PT Ruma, Promogo along the way and building its own brands including Go Box, Go Tix and Go Glam.

Both approaches aim at expanding the core and increasing the value to consumers (and thus capturing more user value). Professor Pangarkar points out “Services like cleaning and moving are often low frequency and not very transparent in pricing and service quality, putting them together in one platform makes each of them stronger.”

Professor Chen says, “In emerging markets, lack of trust is often the issue, especially for smaller players. The branding effect that a superapp brings to a particular service offering is therefore extremely important. Especially for smaller players, connecting their apps to Grab provides a short cut to grow their services.”

Ajisatria Suleiman, founding Director of Indonesia’s Fintech Association adds that in Indonesia, his sense is that an open system with many partners is stronger than a closed one.

This would sound familiar to people in China – Baidu wanted to own everything in O2O, while Alibaba took an approach of controlling the core (of payment and food delivery) but working with partners to offer many other services – the results are obvious.

Who would win?

Both Grab and Go-Jek have far exceeded others in the region in fundraising – Grab has completed US$4.5 billion in the US$6.5 billion it planned to raise in this round, while Go-Jek has so far secured US$1 billion in the planned US$2 billion round.

For both, it is pivotal that the superapp strategy actually succeeds.

Professor Pangarkar points out: “The superapp will bring their owner huge room for growth, while in the short term it requires a lot of investment. The role of capital is very important here.”

“Comparing the two, Grab has a better chance,” says Professor Chen. “The key reason is that while Go-Jek has a solid core in Indonesia, it is built for Indonesia from day one, while Grab has been a Southeast Asian app from the very beginning”

“The more likely outcome is, Go-Jek becomes a superapp for Indonesia while Grab is the superapp for Southeast Asia,” Professor Chen adds.

Or maybe, Line will become a superapp for Thailand?

The original article was written in Chinese by Yating Zhao and translated into English by Miriam Trocha.