Last week, in a blog post titled “We all heard Didi charges driver a high commission, why does it still lose money”, Didi ‘revealed’ its unit economics:

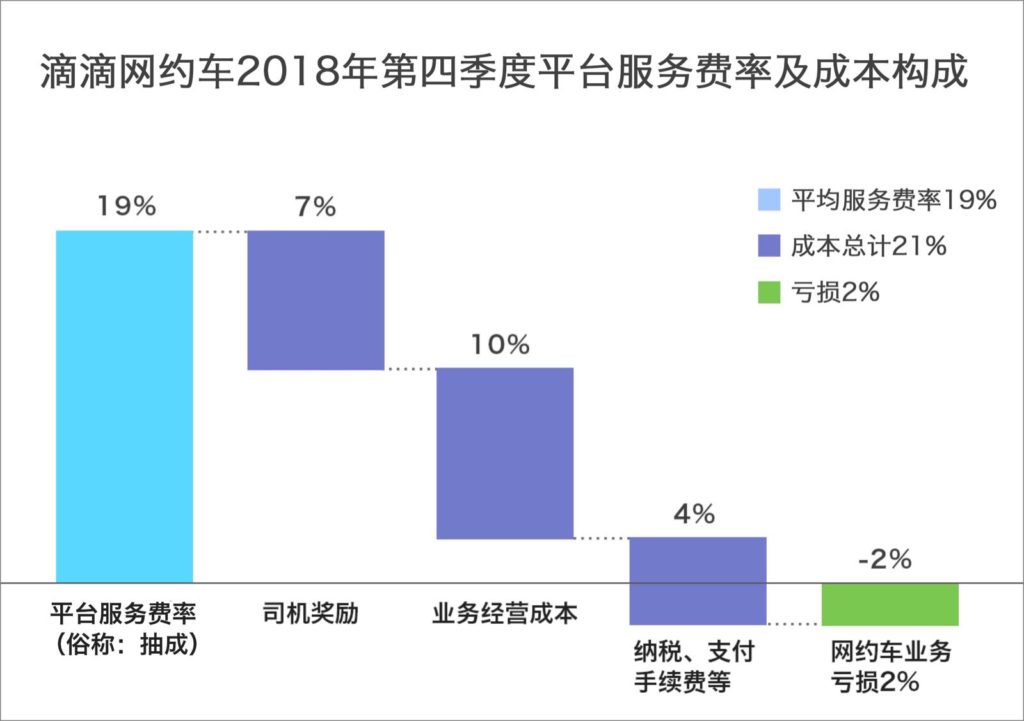

According to the graph above, Didi’s average take rate is about 19% of the fare. On the other hand, 7% of the total fare is given back to drivers as rewards/incentives, 10% operational cost, 4% tax and payment transactional costs etc.

In total: 19%-7%-10%-4% = -2%. This is the loss that Didi makes on each order.

This story is widely reported in media – however, many did not notice that the blog post is actually pushed to average users of Didi on their app. The objective seems to create some sympathy amongst average users, rather than sending out a message to the business/investor community.

Fundamentals

There are only two questions here worth asking:

- Is Didi’s market share defendable?

- Is Didi’s valuation sustainable?

Failing to become a super app, both are actually in doubt. We asked a few people familiar with the company’s operations, the numbers (of daily rides) we get are between 12 million to 26 million, with an average ticket size of CNY25-30.

With that in mind, you can work out how much Didi should be worth – if you use the take rate as a benchmark.

That said, Didi is still a relatively young company. They still have time ahead of them to figure out how to answer the two questions above.

Give it some time.