Last week, the Investment Alert Task Force or SWI (Satgas Waspada Investasi) from Indonesia’s Financial Services Authority closed several fintech scams in Indonesia. This closure was carried out in line with the discovery of 86 illegal peer to peer lending platforms and 26 unlicensed business activities that could potentially harm the community throughout April 2021.

Among those 26 unlicensed businesses, one of them is the Saling Jaga program that belongs to KitaBisa.com, a social crowdfunding platform. SWI suspects that the SalingJaga is an insurance activity. Therefore, KitaBisa must obtain an insurance business license from the Financial Services Authority (OJK), as stipulated in UU 40/2014 on Insurance.

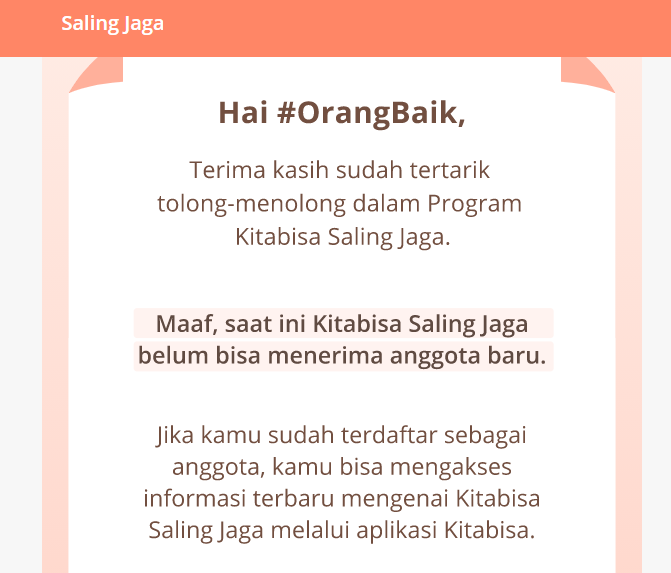

For those who are not speaking Indonesian language, here’s the message:

KitaBisa.com is a social crowdfunding platform. Kitabisa provides a platform for people to raise funds in a transparent manner. Every donation that comes in is recorded by the system so that it can be accountable for the amount of donations collected to both donors and the public.

Previous campaign on KitaBisa featuring Indonesian influencers:

So, how does Saling Jaga work?

Kitabisa’s Saling Jaga is a donation program tailored among donors to help them when they are in need – in this case if they are diagnosed with specific illness. By joining Saling Jaga, donors can help other members as well as ask for assistance if they are diagnosed with one of 54 critical illnesses or COVID-19.

To join this program, users need to register in Kitabisa platform and verify their ID. And only 17 to 59 year old users are eligible to register. And users can register their family members too.

After registration, users need to donate as minimum as IDR 10,000 (~ USD 0.7) to be considered as active members. Later, when the donation is disbursed to help the other members, our balance will be deducted accordingly. And to keep the active membership, we just need to keep our balance as minimum as IDR 10,000 (~ USD 0.7).

Active members with critical illness can get up to IDR 100 million (~USD7,044) donation while COVID-19 patients will be given IDR 5 million compensation, roughly around USD 350.

Saling Jaga adopts the concept of Tabarru’ fund in accordance with sharia principles. Literally, Tabarru’ means goodness. Tabarru’ fundraising means fundraising aimed at good and helping others.

From this point of view, the basic principles of Saling Jaga are different from what insurance does:

- It doesn’t cover all medical bills – very different if we compare it to Indonesia’s BPJS Kesehatan (National healthcare insurance) that covers all the medical expenses.

- Medical assistance is provided as long as shared cash is available and only given once – This is different from the insurance, which is guaranteed by service providers.

- There’s no periodic fees (payment monthly or annually)

However, I can see that they play in a very gry area – it is very similar to insurance but it’s not insurance. On the other hand, they also tried to sell sharia insurance (from BRI Life) on the same page in which they need to have a special license to sell the insurance product.

This is similar to the Shuidi (a.k.a. Waterdrop) business model in China which recently went public (NYSE: WDH). We wrote about them back in 2019.

Based on their stock market debut, their share price dropped 20% because of regulatory concerns. It will need to demonstrate that it’s business model (i.e. insurance distribution) is not breaching any regulations, and is sustainable.

Here in Southeast Asia, Kitabisa is in a similar situation (sans IPO). I am sure that they, as well as the regulators are scrutinising the next steps of Shuidi.

In any case, fintech in China and Southeast Asia are agile in nature – each party is watching and assessing what is their next chess move.