In a previous article, I talked about Indonesia’s next ‘thing’ after fintech being insurtech, as well as the challenges players face to build it.

The digital insurance model has yet to be popular – I can only name one company, Simplr, which is doing that. Nonetheless, there are many aggregators, including Qoala, which recently raised US$13.5 M series A funding.

It is understandable why everyone went to become an aggregator. It does not take the long process and stringent requirements (including capital) as compared to fully licensed digital insurance manufacturers; and they can work with multiple insurers while customer acquisition cost is low.

That said, they still need to acquire customers. How about companies which already have a large customer base (therefore it does not cost anything for them to acquire – just need to convert)?

For example, Grab has already made a number of initiatives in insurance. Tokopedia, which probably owns the largest consumer traffic for ecommerce platforms in Indonesia (and facing pressure from the fast growing Shopee), does not want to be left behind too.

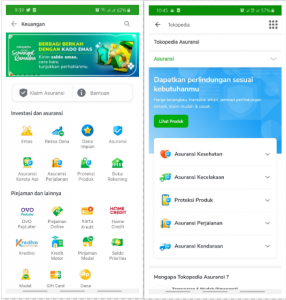

It has an insurance section under its ‘Finance category’ – a friend has been telling us about it. This is how it looks like:

Various kinds of insurance products are being offered here, including health, accident, product protection, travel, and vehicles.

It seems they are quite serious about this – and they have secured partnerships with big insurance companies including MSIG, Tokio Marine, Zurich and Etiqa.

Tokopedia facilitates people who want to apply for those insurance products in a very intuitive, browsing way. I am not sure about the numbers but I have done a lot of browsing while under lockdown these days.

What it does certainly makes sense – giving its existing customers more choices and more products to buy (Alfamart and Indomaret does something similar, offline).

Whether Tokopedia will capture this market, or how much of this market they might capture, depends on a number of factors, including customer awareness, ease of use, competition as well as the inherent decision making process for specific products (e.g. it is hard to buy life online without someone explaining to you in person).

As explained before, educating people is quite a challenge, and crucially you never know how much effort is needed.

However, as a side business to keep its existing users engaged, Tokopedia is already doing a not bad job. Even by browsing, my friends and I are already spending quite a bit of time on the Tokopedia app.

Would they go deeper by seriously capturing the market against the independent players (and Grab, with whom it shares Softbank as a major investor)? Or will they even apply for an insurance licence to own a digital insurance company?

There are many factors, internal and external, which might affect this evolution. Definitely worth watching for the next 2-3 years.