Our Briefing on Blooming Ecommerce in Indonesia report last week generated a lot of interesting discussions during the Q&A phase. Questions were raised about specific players, the competition, new business models, etc.

Because of the time constraints, we could not answer all the questions on the spot. We thought it would be useful to share some of the questions and our perspectives on them here – so that a wider community might benefit.

As usual, you are welcome to write to us [email protected] if you would like to discuss further, or disagree with, any of the points.

On competitive landscape

1. Tokopedia has managed to surpass Shopee in Indonesia in terms of monthly visits in 21Q1. Although the gap is quite limited, will Shopee lose its market share? What has Tokopedia done to attract more visits?

Yes, according to iPrice’s Map of Ecommerce in Indonesia, Tokopedia had a higher number of monthly page visits in Q1 compared to Shopee in Indonesia.

However, we need to be mindful that page visits are only part of the picture – Shopee has focused on a mobile-first strategy and we believe a majority of the visits and sales probably came from apps.

As we can see, Shopee is still firmly number 1 in app ranking.

Another thing people should be aware of is that Q1 is typically the quietest month for ecommerce in Southeast Asia if not globally. A lot of the promotions and shopping festivals are in the rest of the year: Ramadan in Q2, 9.9 in Q3, 11.11 and 12.12 in Q4.

2. On the backdrop of the successful merger of GoJek and Tokopedia and even the IPO plan cited in the public source, what are the challenges you expect Shopee will face by the end of this year (user retention, customer acquisition, average order value etc.)?

An immediate consequence: if the combined GoJek and Tokopedia entity (GoTo) goes to IPO, it will replenish the cash reserve for a longer term fight. This will probably increase the intensity of competition in ecommerce as both will now be judged by the public market. Expect free shipping to continue.

A point on average order value, we actually believe that when GMV is equal, lower average order value means more to the platform. It shows for the same sales, much more transactions are created – and consumers are voting with more confidence on the platform, which in turn drives the flywheel.

3. How strong are the Tokopedia x GoJek synergies? Looks great on paper but success rates for M&As are low?

I have written about the perceived Tokooedia-GoJek synergy on SCMP when the merger negotiations further became public.

While we know that post-merger integration can be difficult, we presume the leadership of both companies know that as well. That’s probably one of the key reasons why they assured investors that both companies will still operate independently, at least in the short term.

The real immediate focus post IPO will probably be on clawing back market share from Grab and Shopee, rather than driving synergies within the group.

4. Tokopedia and GoJek are basically local players, they have little presence or success outside Indonesia. How would this impact their growth?

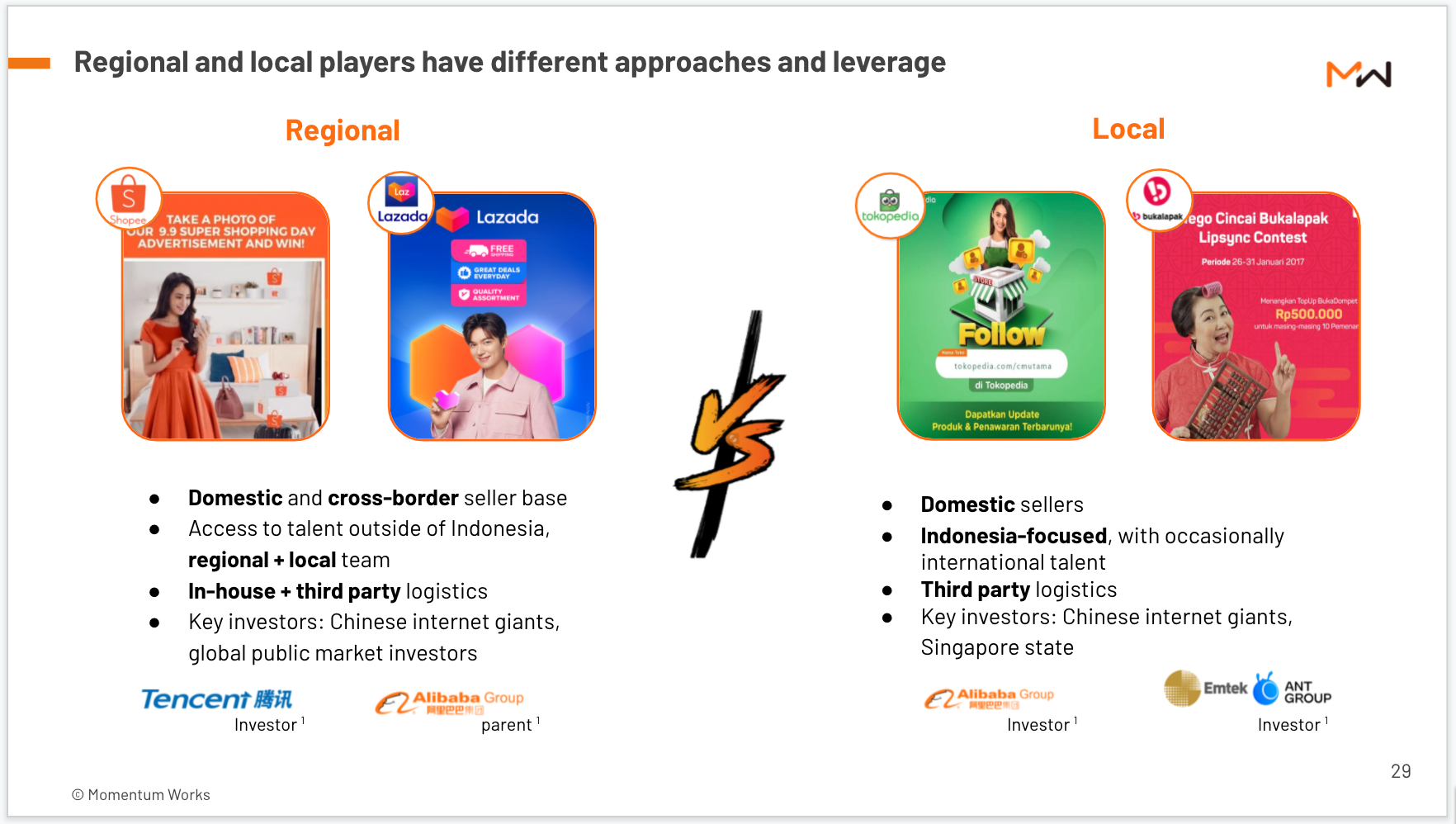

We have compared regional and local players in the report as well as the briefing deck:

A regional player thus far has better access to talent, ecommerce expertise and cross border seller base. Besides, other markets (especially the ones with better economics – such as Thailand, Malaysia and Singapore) also serve as a cushion for regional platforms to be able to invest in Indonesia for the long term. Having a bigger addressable market also gives a larger valuation potential.

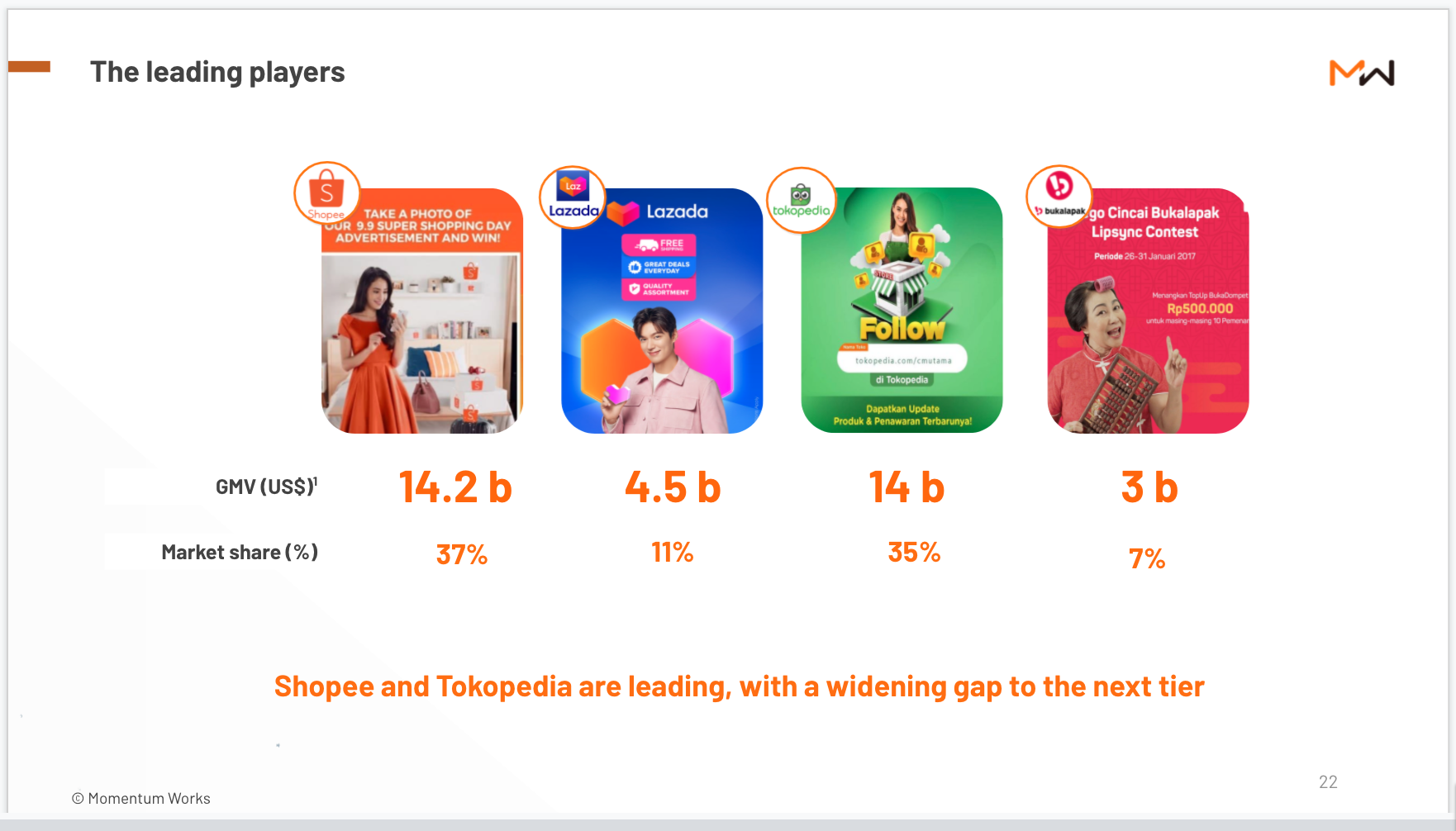

5. How do you see Bukalapak and what’s their competitive advantage? Is the GMV mainly coming from Mitra Bukalapak

Mitra probably contributes about 20-30% of the GMV of Bukalapak, with the remaining still B2C.

Bukalapak has been operating in a relative niche compared to other players – the majority of the urban users we have spoken to use other platforms, while many Bukalapak users use only Bukalapak.

However, we expect that the overlap will increase. Other large players will be targeting Bukalapak’s segment to look for further growth. Shopee and Tokopedia are formidable players, and Bukalapak will need access to the capital market to defend.

One sign of worry is that Bukalapak’s founders have all departed. The only other large ecommerce player in the top 4 in Indonesia not run by its founders is Lazada, which has not done a great job.

6. Do you have any numbers comparing Shopee/Tokopedia in the Jabo area vs the other areas? Is GMV concentrated in Jabo still? How about acquisition costs for areas outside Java?

We have not examined this particular breakdown of GMV by provinces in detail. The rough information we have is that the Jabodetabek area still accounts for probably more than 60% of total ecommerce volume in Indonesia, although the volume outside Jakarta, especially through social commerce, is growing fast.

The concentration in the Jabodetabek area is understandable as the region has a significant concentration of consumption power, ecommerce infrastructure, and traffic/parking issues. Many of the users we spoke to in the Jakarta area buy more than half their purchases through ecommerce.

We also know that the interest in Shopee is significant especially in provinces.

As for the acquisition cost outside Java, what we have seen is that social commerce and bulk purchase have been two important growth areas.

The regional balances in actual ecommerce volume, as well as customer behaviour, probably warrants a dedicated study. We will look into it.

7. Would Grab acquire an ecommerce player even though they are denying it, saying it will burn too much cash?

Grab has focused on building infrastructure that is more catered to on-demand delivery compared to normal ecommerce delivery.

From China’s experience, this is one step ahead of normal ecommerce – Meituan has been offering ecommerce delivery in addition to food and grocery, based on the same infrastructure. When consumers can get their ecommerce parcels in 20-30 minutes reliably with sustainable unit economies, nobody will probably want to wait for a few days.

In that case, buying a normal ecommerce platform will probably be a distraction for Grab.

Besides, Grab and Emtek (the biggest shareholder of Bukalapak) have investments into each other. We expect more such deals and alliance building in the future.

8. When do you expect the fighting will be over? Will there be 3 ecommerce marketplaces in the end?

I do not expect the fight to be over. Even in China when many assumed that the ecommerce fight was over a few years ago with Alibaba and JD dominating, Pinduoduo came about and took market share rapidly. In addition, Meituan is now undermining the whole premise of ecommerce with on-demand fulfilment.

We expect new models in Indonesia as well – though in the short term it will probably be harder because leading players have access to what is going on in China in order to pre-empt.

We think it is hard for 3 marketplaces operating similar models to thrive.

Going social

9. What’s your opinion on the competition between TikTok ecommerce and marketplace ecommerce given TikTok has such big MAUs?

We mentioned “watch out for TikTok” in the conclusion of the briefing:

TikTok has already experimented with Shopping Cart and Seller University for Indonesia – their ambitions for ecommerce is very evident.

An advantage that TikTok has, which ecommerce platforms do not have, is the influencers. Thus far most influencers in Indonesia earn money by advertising (with some dropshipping), TikTok might allow them to sell directly through a much more smooth process. This is something that the Facebook ecosystem has not been focusing on as well.

To make it work at scale, TikTok will probably work hard to attract more sellers, so the whole transactions could be done within its platform (instead of redirecting to ecommerce sites).

10. Will Shopee be able to get to social distribution faster than the social commerce guys get to ecommerce monetization?

We will discuss this in more detail in the 3rd part of the Ecommerce in Indonesia Report, which covers new business models 🙂 We will have a briefing afterwards to address this and other issues.

We will send invites to TheLowDown subscribers and Impulso community members by the end of this month – stay tuned!

11. How about social commerce in Indonesia, like Facebook, do you have some research?

The short answer is yes – refer to the answer to question number 10.

12. What do you think of livestream commerce?

Still in its early days in Indonesia – our colleague wrote about it on TheLowDown before. Many players are experimenting and that is how you typically push a sector to grow.

TikTok will probably be leading – but it would be interesting to see Shopee and Tokopedia, both of which are experimenting, will achieve something similar to Taobao in live streaming audience, interactions and sales

13. Could you comment a bit about Shopee’s strategy on Shopee Live?

It is in its early days. They are definitely trying to make it work, though it will take a bit of time to get the whole ecosystem ready.

Strategy-wise, there are very sophisticated strategies and pathways they can reference from China.

Brands

14. In Southeast Asia, besides platform e-commerce, do merchants of a certain scale have the opportunity to operate and promote their own e-commerce websites or apps?

Yes, though for non established merchants/brands, this might be much harder as platforms will drive up the overall acquisition cost in the market.

15. Is the market too nascent yet for D2C brands?

I think the market is ready for D2C brands – in fact, many D2C brands have been created on Instagram, and many Chinese D2C brands have been tapping into cross border sales into Indonesia.

The real question, in our opinion, is whether the market is big enough for large, venture-funded D2C brands. These will probably still take some time to emerge.

16. Do you think the brands’ sales growth(similar to TMall or Taobao) on Shopee will surpass 3rd party sellers’?

Not any time soon.

17. When can we see a visible consumption upgrade trend on ecommerce in Indonesia (from c2c to b2c model)?

Even in China, whether ‘consumption upgrade’s is really taking place is still highly debatable – seen from how much volume Pinduoduo can generate by targeting lower-end consumers.

For Indonesia, it is relatively easy to calculate the consumption power of each consumer segment and derive the total addressable market of ‘consumption upgrade’ consumers.

However, if we broaden the definition of “consumption upgrade” – good sellers that emerge from “natural selection” in the platforms will probably create brands, even if the market they target is mass.

18. In China, C2B seems to be appearing. What do you think about the C2B model in Indonesia?

We believe that it is already happening outside the platforms (on social media etc.).

However, whether this can happen at scale, and if so, when it will, is a question worth more study. We do not have a ready answer for that.

19. If we can categorize Tokopedia, Bukalapak, Shopee as Shared E-Commerce, Is there any player that plays in Dedicated E-Commerce? Because in my opinion the weakness from shared E-Commerce is that the merchant cannot explore more on the uniqueness of the merchant (Price War)

Again, watch out for TikTok 🙂

General questions

20. How did you derive the GMV numbers?

Same as how we derived GMV numbers for food delivery early this year. It is a combination of the numbers that we have evaluated through different sources with a lot of on the ground interviews with people across the ecosystem.

Momentum Works is grateful for the support of its community, including Impulso members, in providing not only insights, but also proxies that allow us to derive and calibrate the numbers.

21. How much bigger would ecommerce (as a percentage of total retail) grow? It seems that it’s already close to 20% in the USA?

2020 was an exceptional year. Not only ecommerce grew in leaps and bounds, but also we saw a dip in overall retail. That combination led to ecommerce taking a far larger share of retail than expected.

Penetration of areas outside Jabodetabek is still low, and social commerce is driving growth as well. Moving forwards we would still expect the percentage to grow in the medium term – and I would not be surprised if it reaches 35%.

Traditional retail in Indonesia is not as efficient as the US in terms of selection, speed, quality and savings. Once the infrastructure is ready, ecommerce can play a bigger role there. We saw the same happen in China.

In addition, ecommerce flywheel can drive other sectors, such as digital lending, groceries and services. So growth potential of large ecommerce platforms is still good.

22. Although SEA is winning, from an investor’s level, would Alibaba (as the key investor in Lazada, Tokopedia and Bukalapak) be the ultimate winner?

Not really. They (and their affiliates) acquired/invested in Lazada, Tokopedia and Bukalapak over time through various initiatives and with various agendas. There has not been great synergy amongst these companies in a way benefiting Alibaba.

On a pure monetary return point of view – Tencent, being the biggest shareholder of SEA Group (parent of Shopee), has probably made a very good investment. Alibaba’s investment from a monetary standpoint will become apparent after GoTo and Bukalapak get to the public market.