Since we released our Rise of digital banks in Indonesia report earlier this year, we have received a lot of enquiries and questions about the ecosystem, which we tried to shed some light on during our ensuing seminar.

A few of you also asked us – how about digital banks in other countries in Southeast Asia, such as Malaysia, Singapore, Thailand and Vietnam?

After some internal discussions, we decided to make Digital banks reports a series. We wanted to cover the ecosystem and answer some key questions in each country, and also build a summary of global best practices.

Since Malaysia has recently closed its digital bank licence application process, we thought it would be timely to look at the country first:

The report seeks to answer fundamental questions from international inventors and key decision makers:

- How are the banking and financial landscape like in Malaysia?

- What are the prospects of digital banks?

- Which are the potential areas for digital bank disruptions in Malaysia?

- How does it differ from neighbouring countries in Southeast Asia?

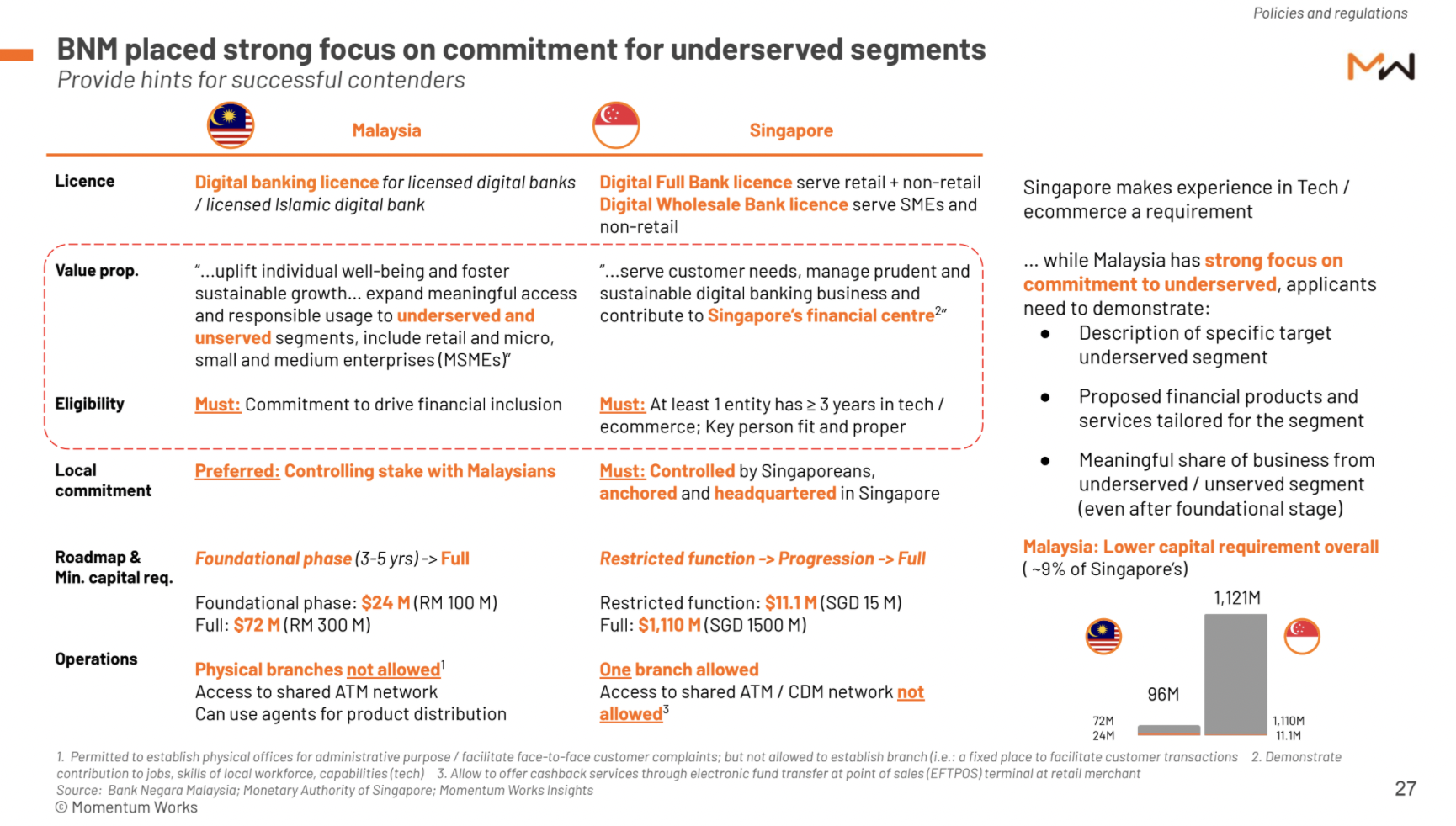

- What do regulators (Bank Negara Malaysia) look for?

- Who are the key contenders for Malaysia digital bank license?

Below are some of the insights from the report:

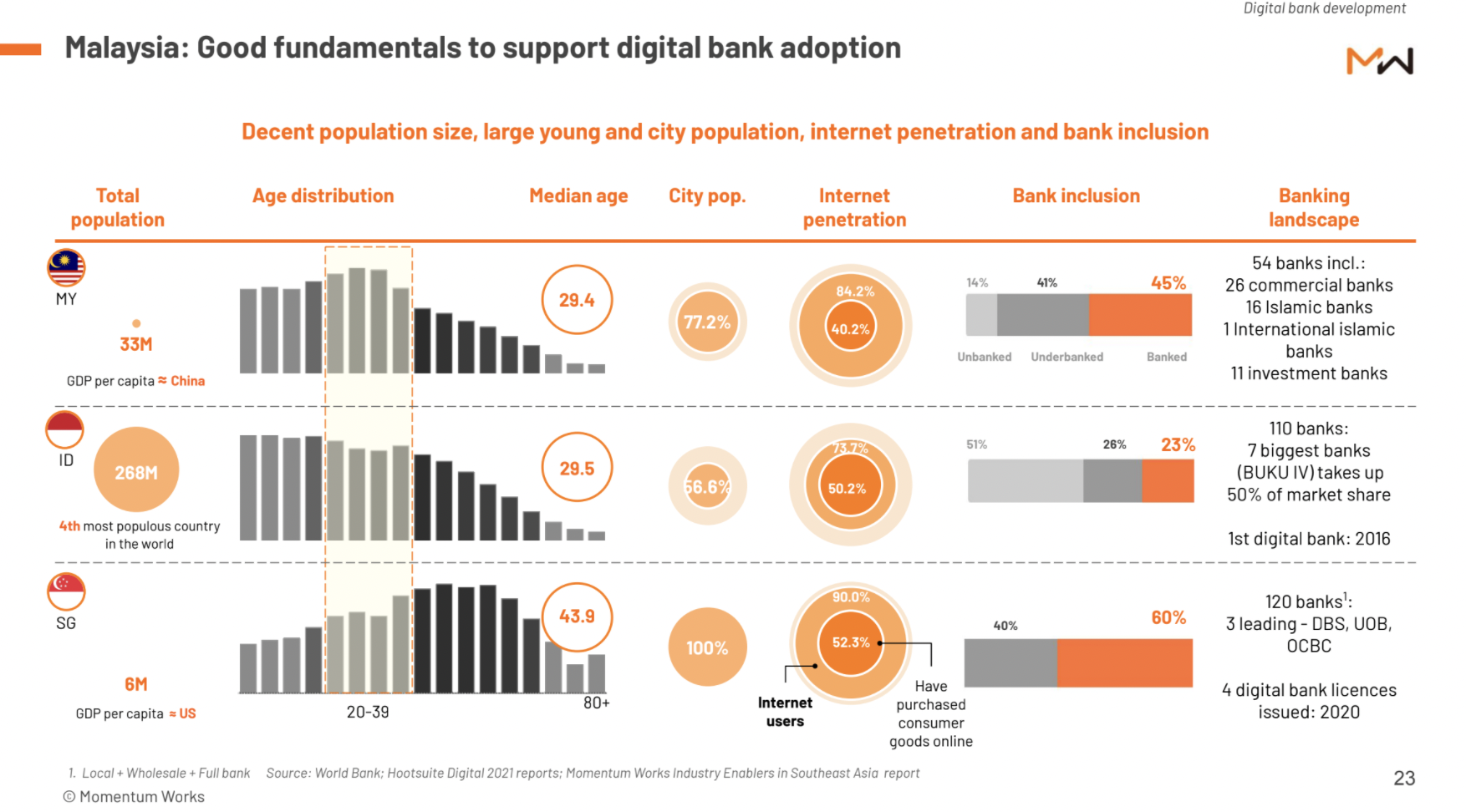

1. Malaysians have been banking online

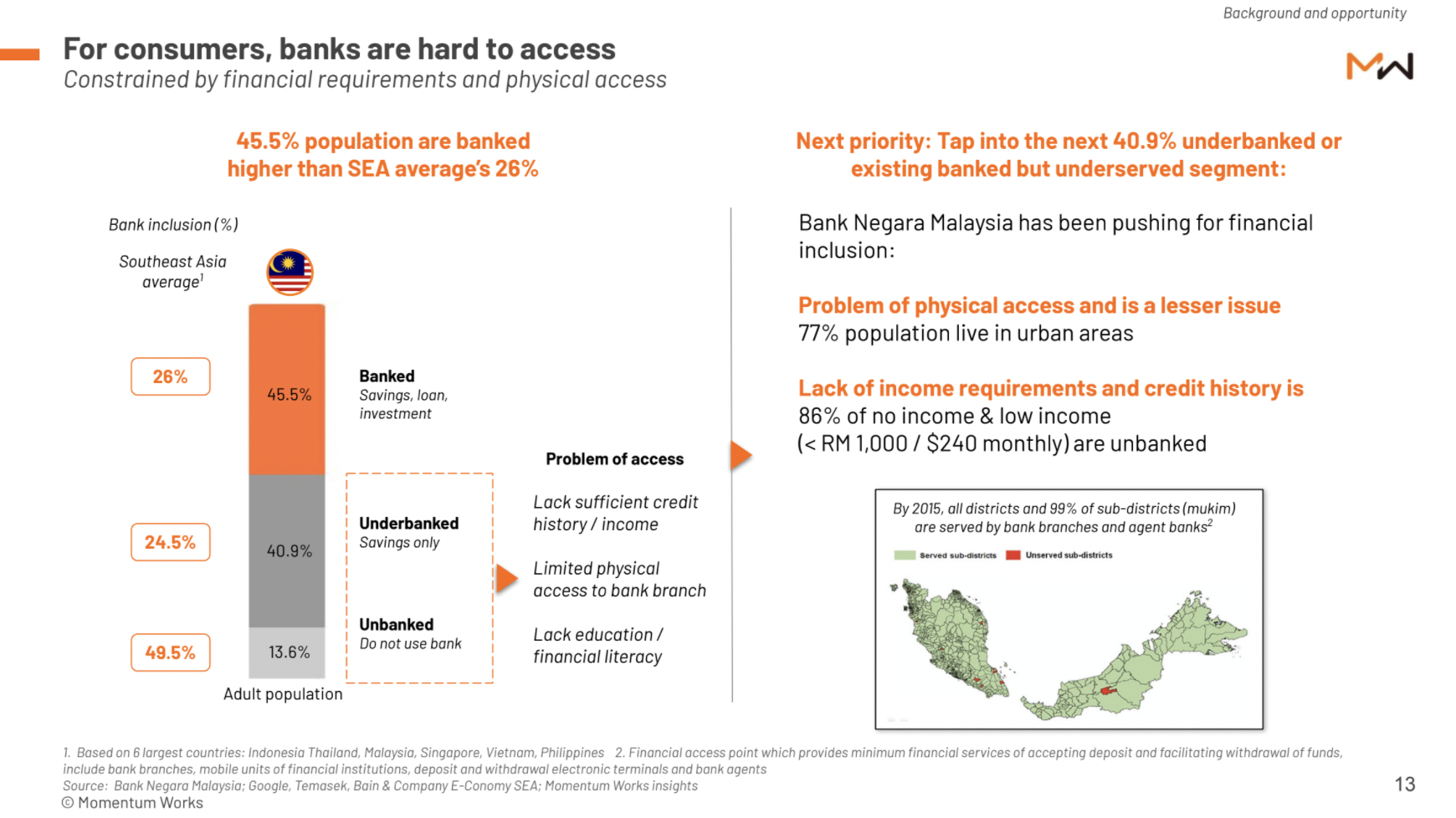

Malaysia’s demographics, urbanization, internet penetration and bank inclusion are quite advanced compared to the region in general. Malaysia’s underbanked communities, which are key focus areas of Bank Negara Malaysia (the central bank), are different from those of Indonesia or Singapore.

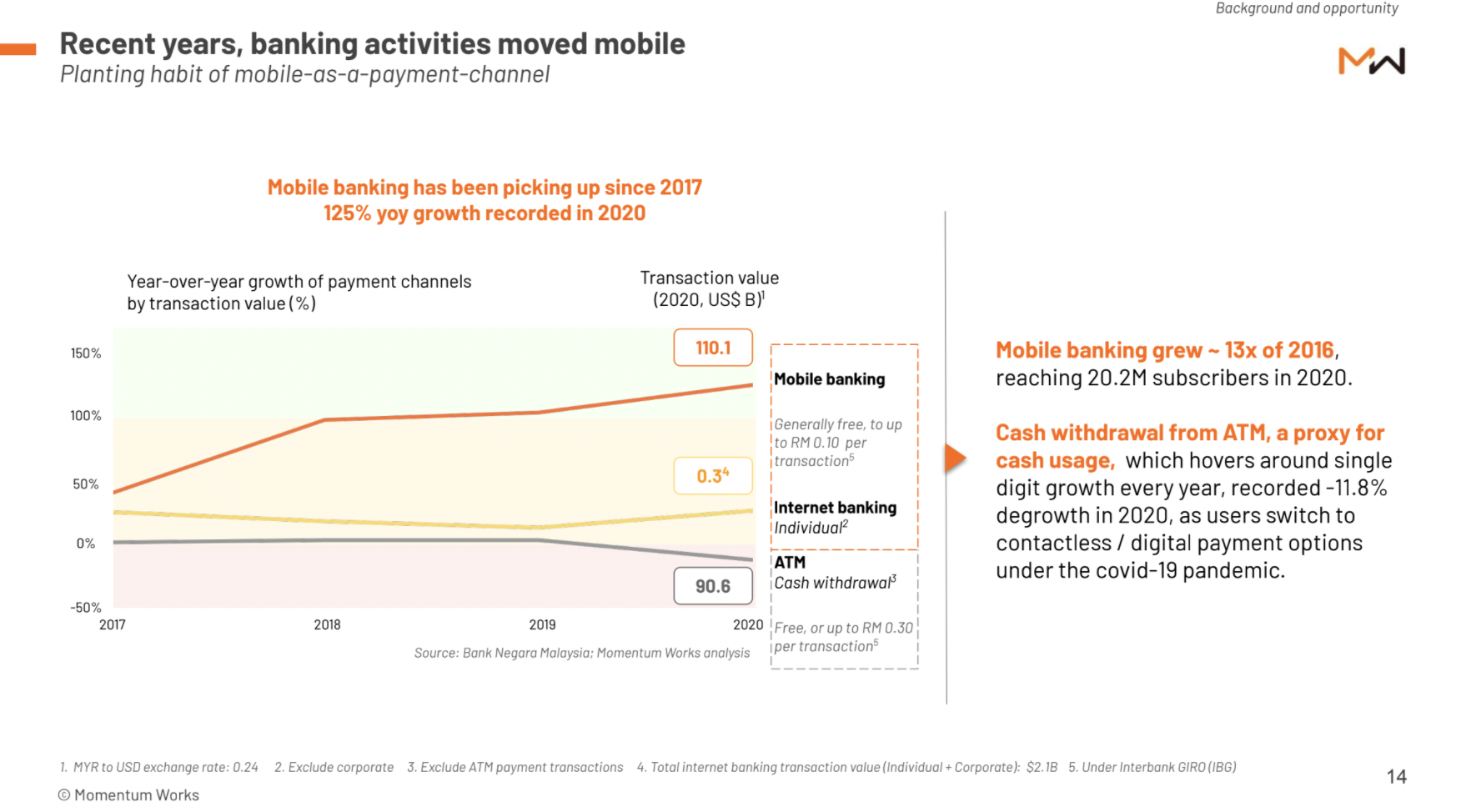

Mobile banking has also taken off, as compared to internet banking and traditional physical access through ATM:

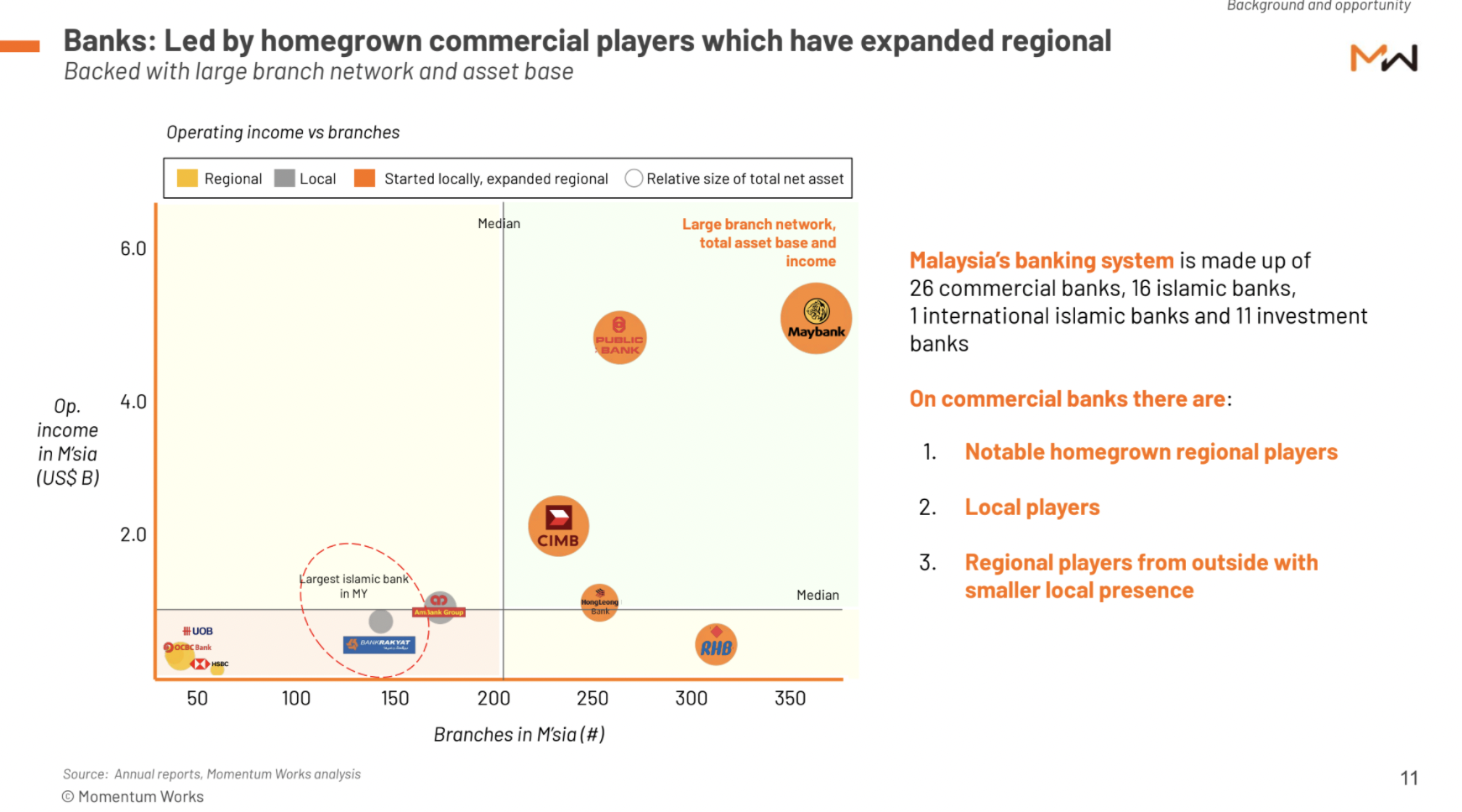

The banking scene is led by homegrown commercial banks, many of which have grown to become regional banks:

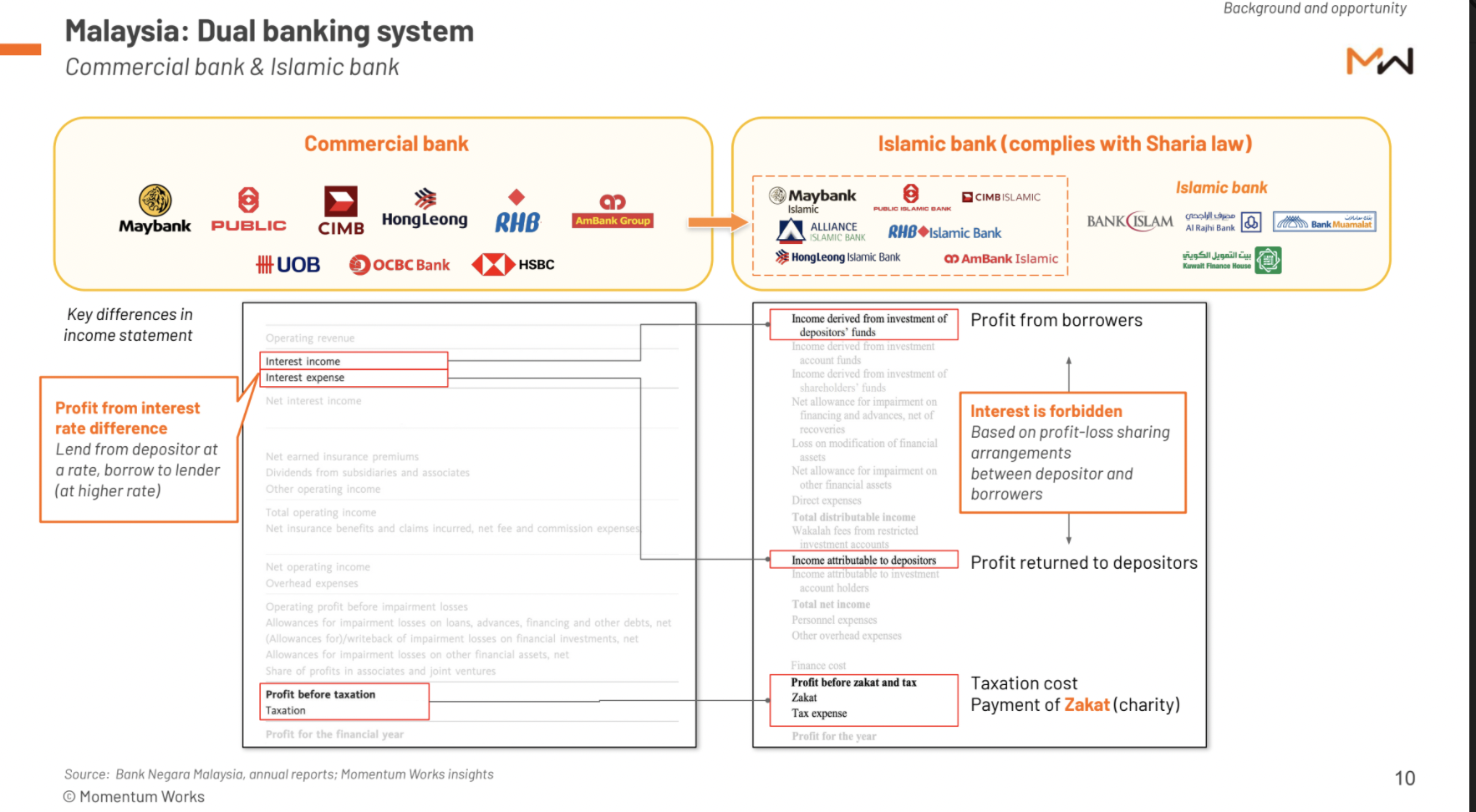

And not to forget that Malaysia is running on a dual banking system, with a fairly developed Sharia banking sector:

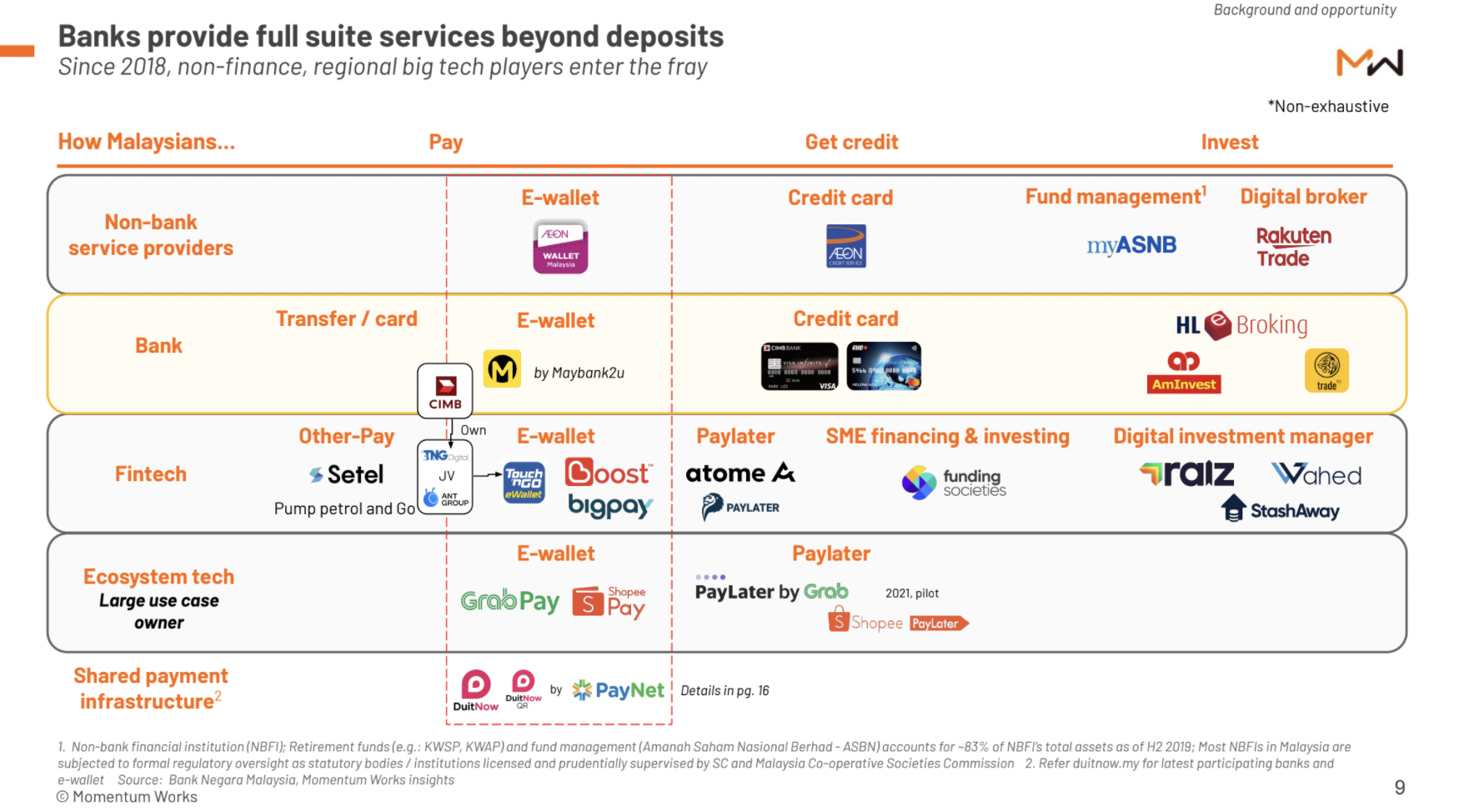

2. The rise of fintech is enriching the country’s financial ecosystem

Financial services have traditionally been provided by banks and non-bank service provides, and the rise of fintech as well as ecosystem tech players is making the ecosystem more competitive:

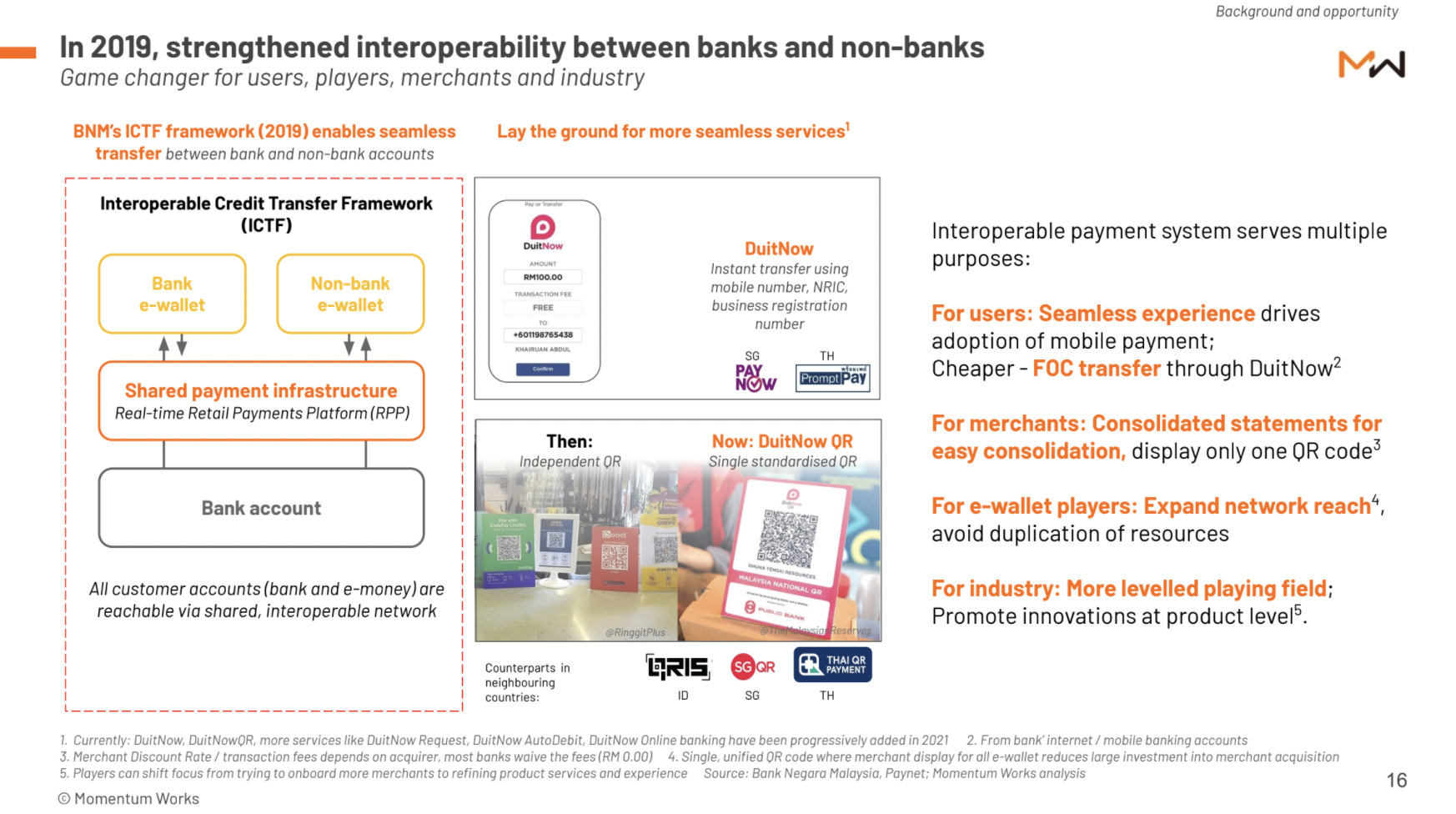

And as many of its neighbours, Malaysia has also been working on interoperability of its banks and non-banks:

3. The case for digital banks (and will they disrupt?)

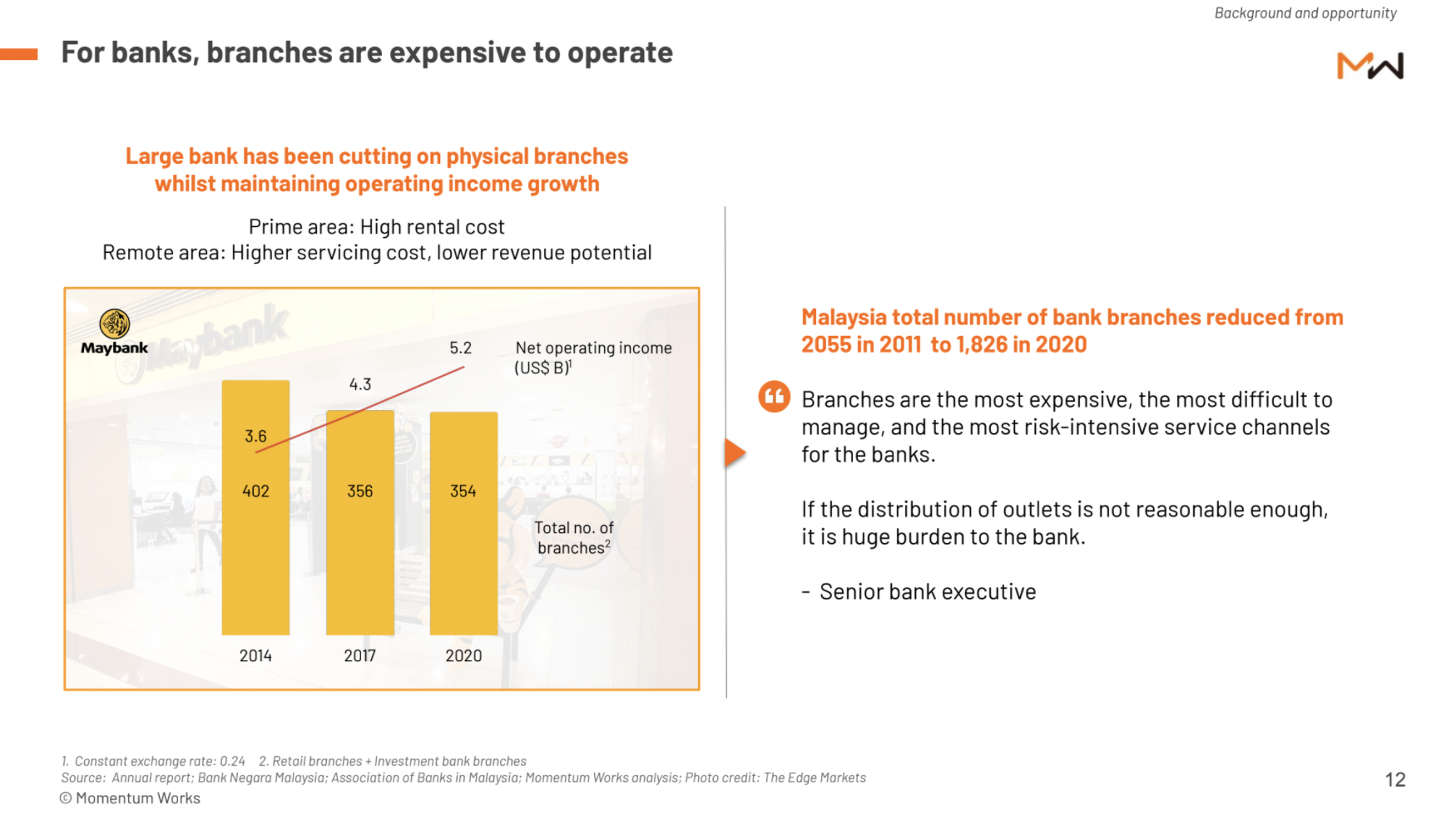

For banks, branches are quite expensive to operate. Malaysia’s banks have been reducing their number of branches over the past decade:

That creates problem of access especially for the population leave in rural and remote areas beyond the densely populated west coast of West Malaysia (which most of the major cities are):

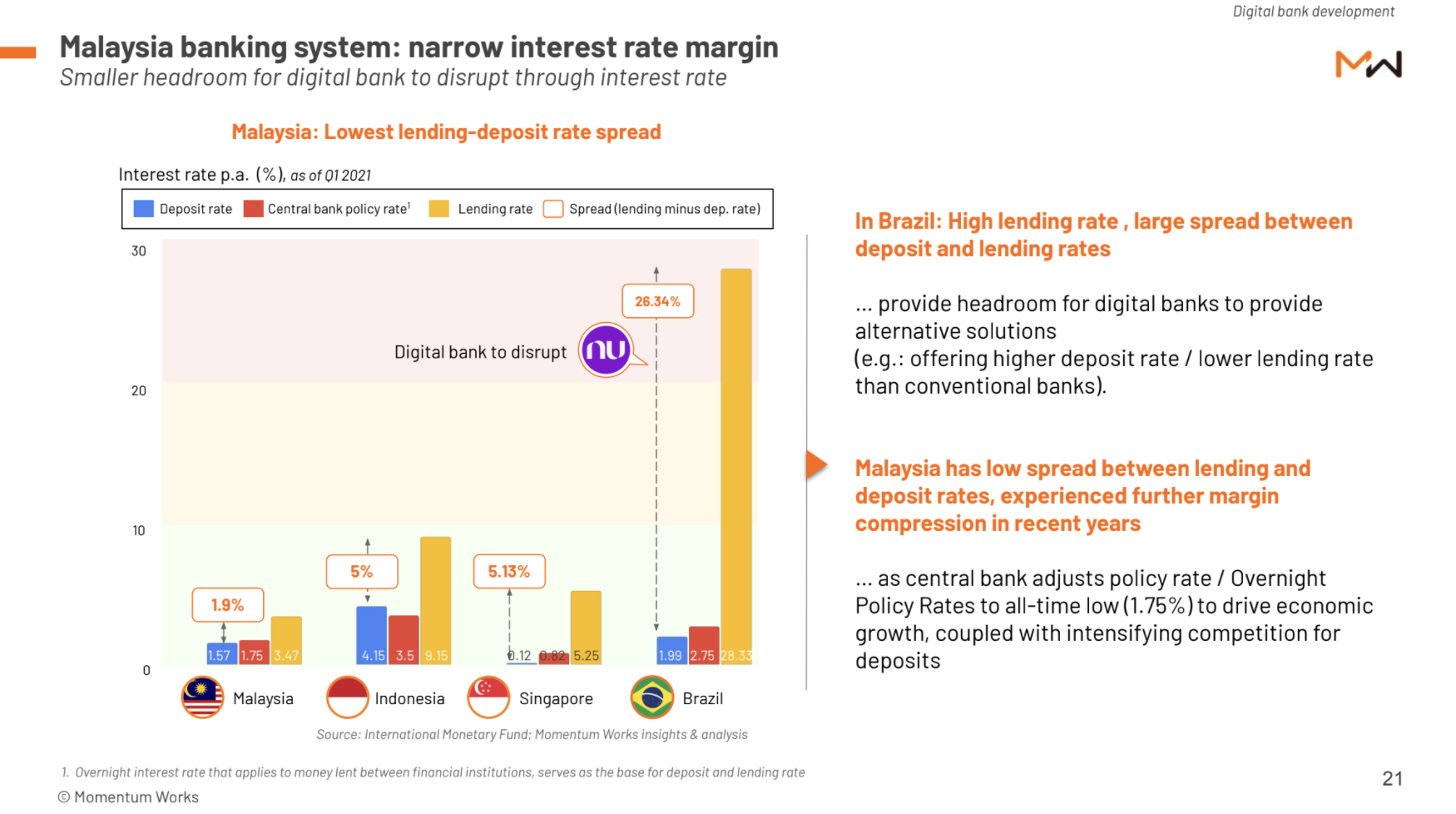

Compared to Brazil, which hosts the highest valued digital bank unicorn Nubank, Malaysia has relatively modest interest spread, which means digital banks will need more creative ways to attract customers (rather than offering interest rate incentives):

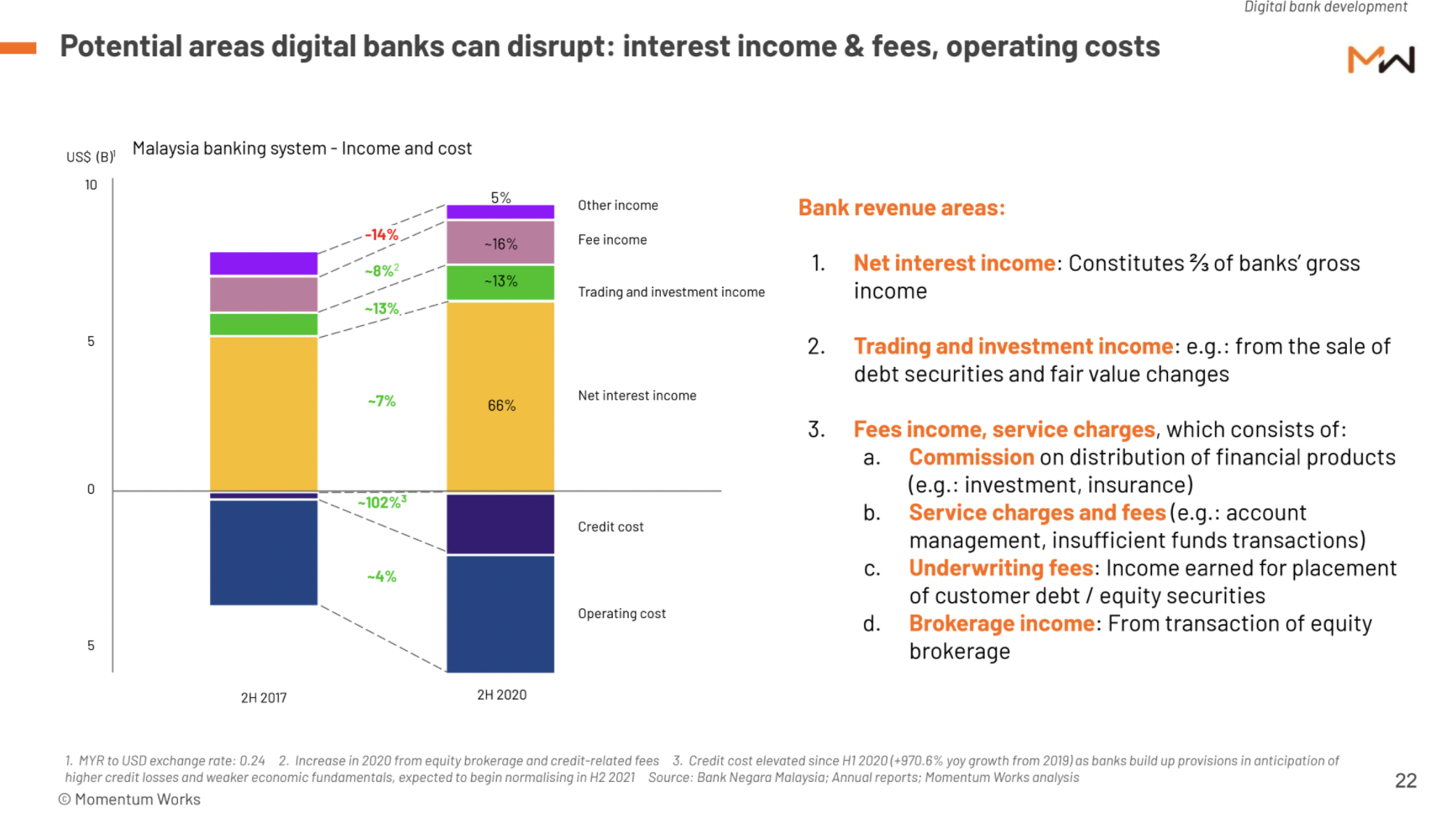

A good way to think about how digital banks could disrupt, or build up its initial hold, is the P&L of conventional banks:

4. Who are the leading contenders for digital bank licence?

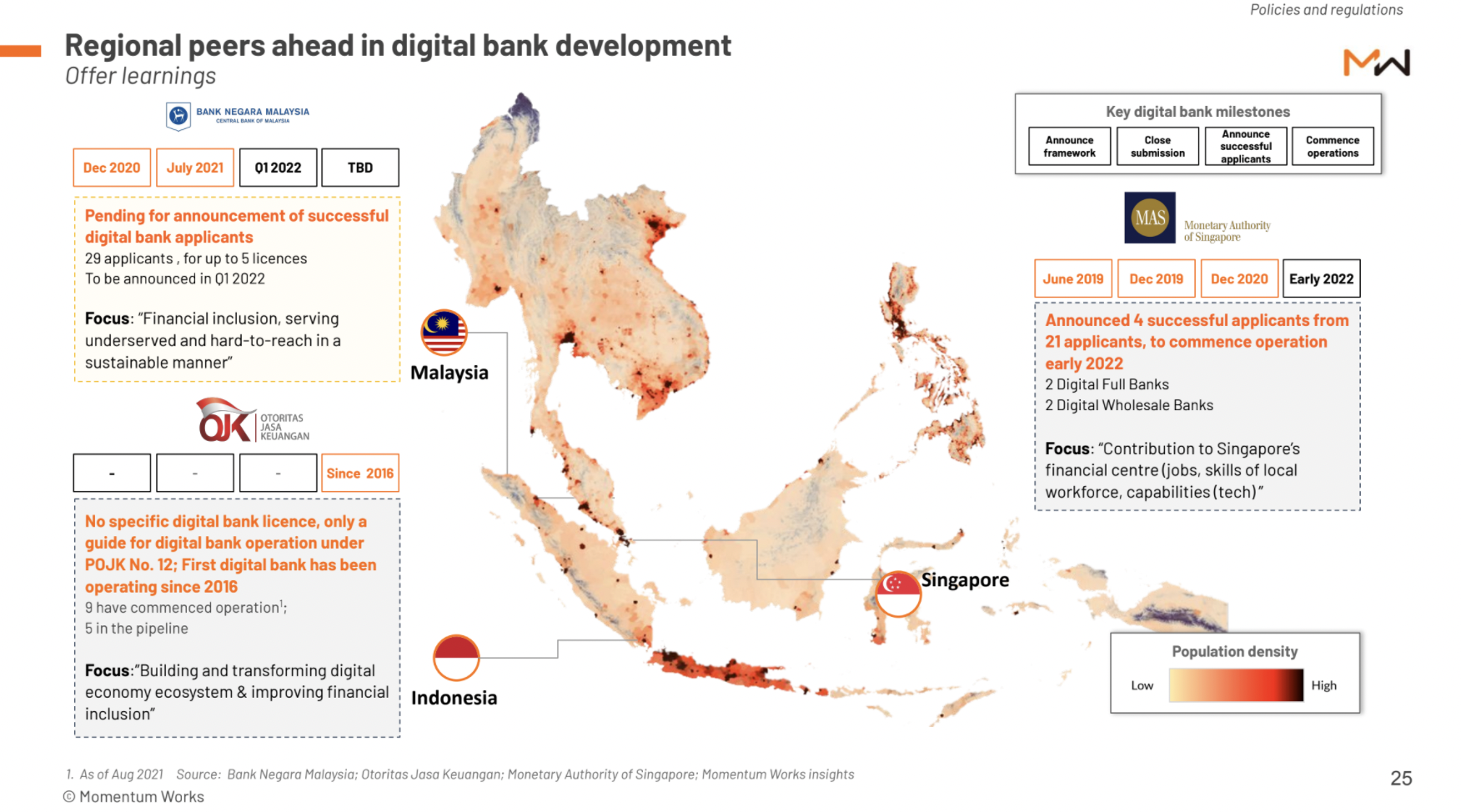

Malaysia’s digital bank licences come after regulator-led and industry-led developments in Singapore and Indonesia respectively:

As mentioned above, Bank Negara Malaysia, the central bank, has been focusing on serving the underserved communities as a key consideration for granting digital bank licences:

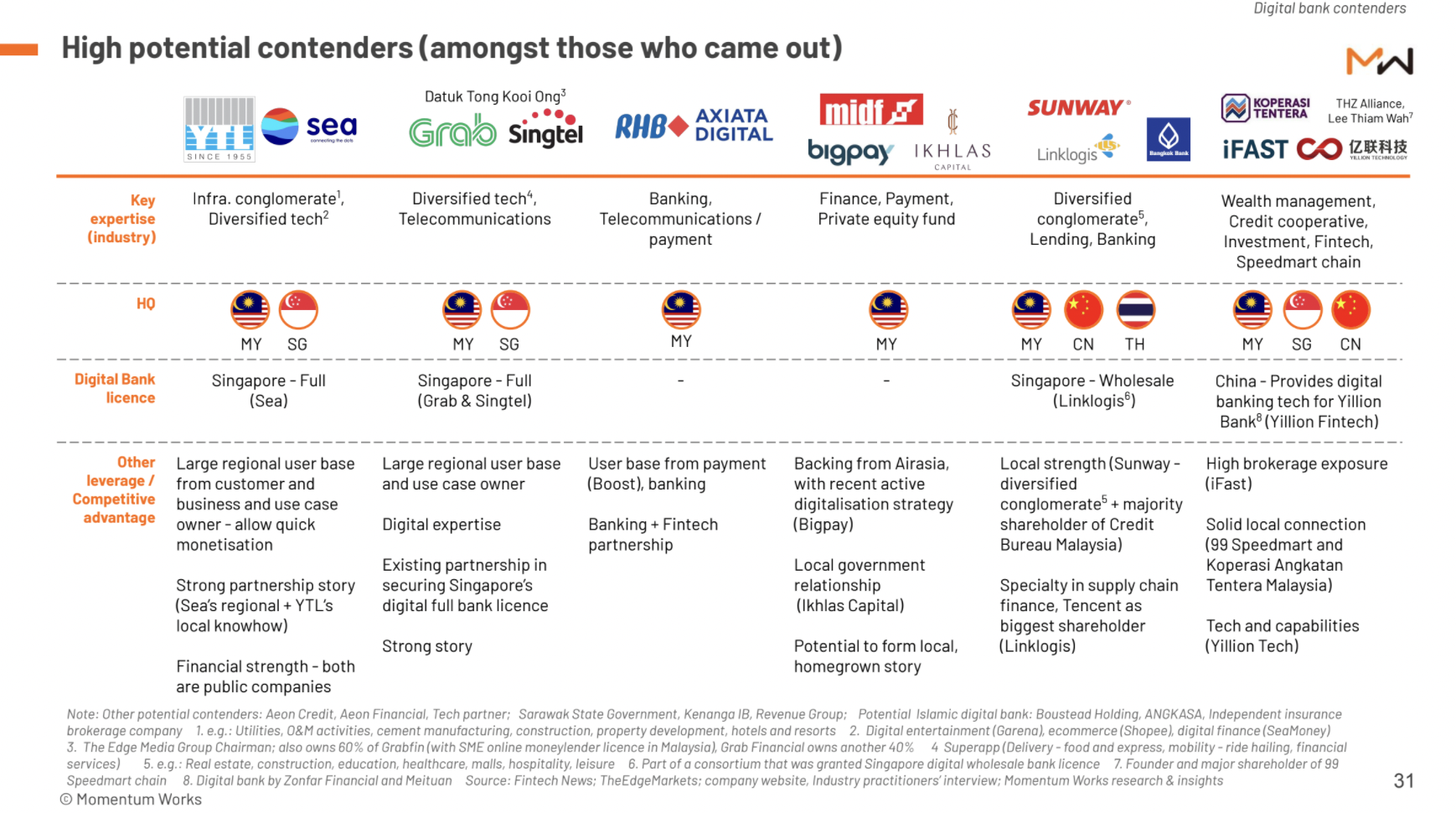

Amongst the 29 players/consortia that have applied for Malaysia’s digital bank licences, the following publicly known ones probably stand a good potential to race to the finishing line:

5. Our perspectives

- Malaysia has one of the more advanced financial/banking systems in Southeast Asia, with higher banked population (45.5%) , lower interest spread and a dual conventional/Islamic setup. Yet there are still significant underserved communities in the country.

- The 40.9% Malaysians have limited use of banking service represent very diverse groups. Serving these groups is the key objective/requirement by Bank Negara Malaysia when granting the digital bank licences in Q1 2022.

- The advanced internet (84.2% penetration), mobile and digital economy (40.2% ecommerce penetration) infrastructure in Malaysia make digital bank penetration possible. The shift to mobile is further accelerated by the covid-19 pandemic. The current revenue / cost structure of banks offers room for disruption.

- However, success is not given. To start with, low deposit/lending interest spread is a challenge, not to mention Malaysian banks ability to dominate traditional banking scene against strong foreign players.

- Amongst the 29 contenders (mostly in consortia) vying for up to 5 licences, there are tech players with large use cases, successful bidders for Singapore’s digital bank licences, and strong local providers of non bank financial services.

- On successful contenders, potentially we will see large ecosystem players, together with more specialised players focusing on specific segments (e.g.: SMEs, as well as Islamic banking).

- Compared to developed Singapore, Malaysia offers a better test ground for providing digital banking services across the region. The lower (capital and other) requirements/restrictions will allow players to be innovative.

Access the report

The report is complimentary for industry players, ecosystem stakeholders as well as investors and people who work in the industry in general. Get your copy here.

We welcome questions, enquiries and sharing – you can email [email protected].

We will be conducting another briefing on digital bank after the next instalment, subscribe to our newsletter to stay tuned!

, China CCP – No More Covid")