Following the publication of our Rise of Digital Banks in Indonesia report, we held an exclusive briefing (here’s a summary of the event) and had the pleasure of sharing our insights with an amazing crowd from the banking, tech, investment industry and beyond.

Here are some key questions that were asked during the briefing and we’ve categorized them into 3 groups: Regulation, Competitive landscape and Growth.

Regulation

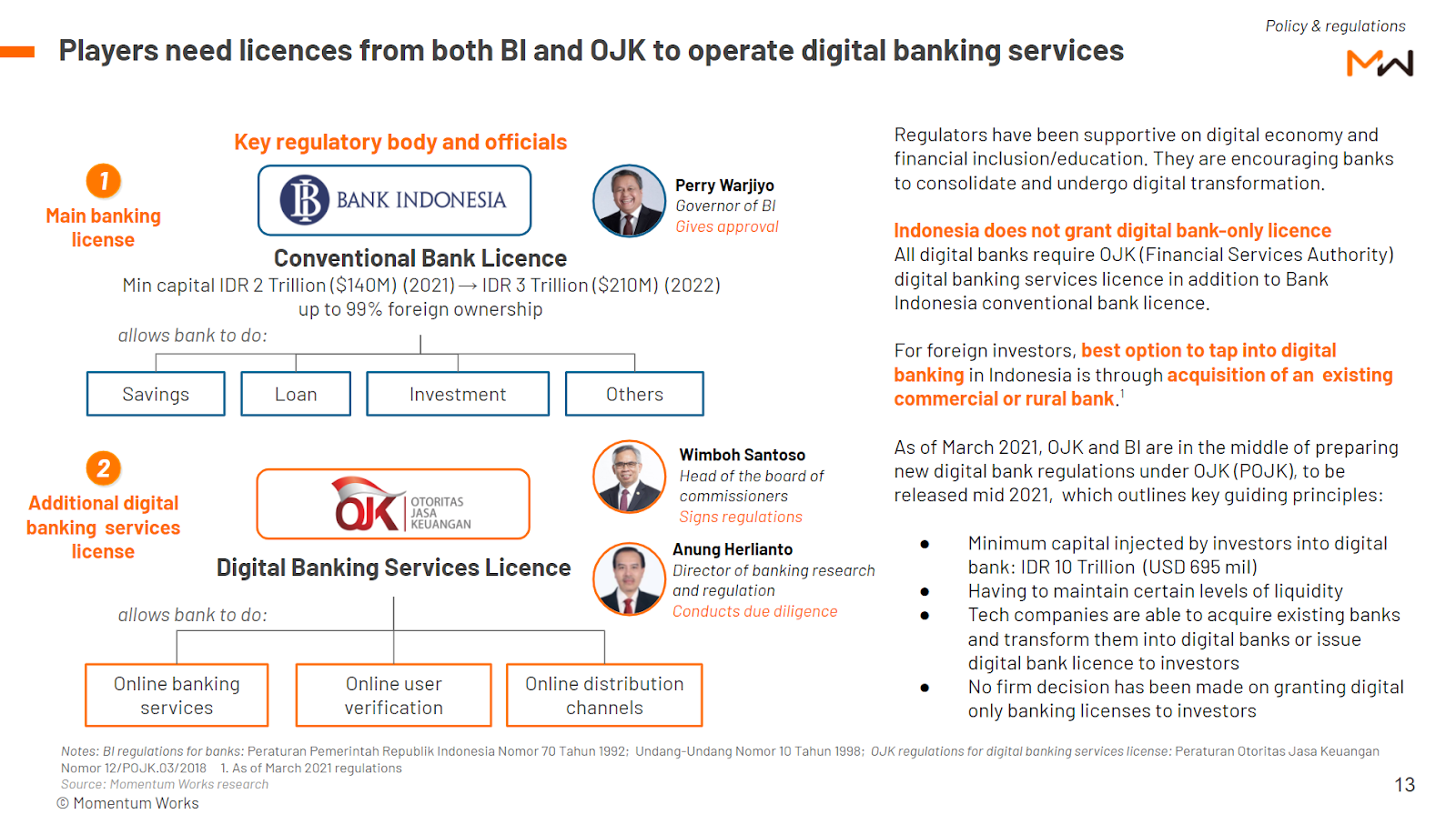

1. What are the licensing requirements for digital banks?

This is actually covered in the report. You first need a conventional banking licence from Bank Indonesia (the Central Bank); subsequently digital banking services licence from Otoritas Jasa Keuangan (OJK), Indonesia’s financial services regulator, needs to be obtained.

2. What are the foreign ownership limitations for digital banks?

Foreign shareholders can acquire up to 99% of shares of an Indonesian bank.

3. Are digital bank licences similar to those of traditional banks?

Yes. A digital only banking licence has been talked about, but we have not seen concrete signs that it is on the table soon.

Competitive Landscape

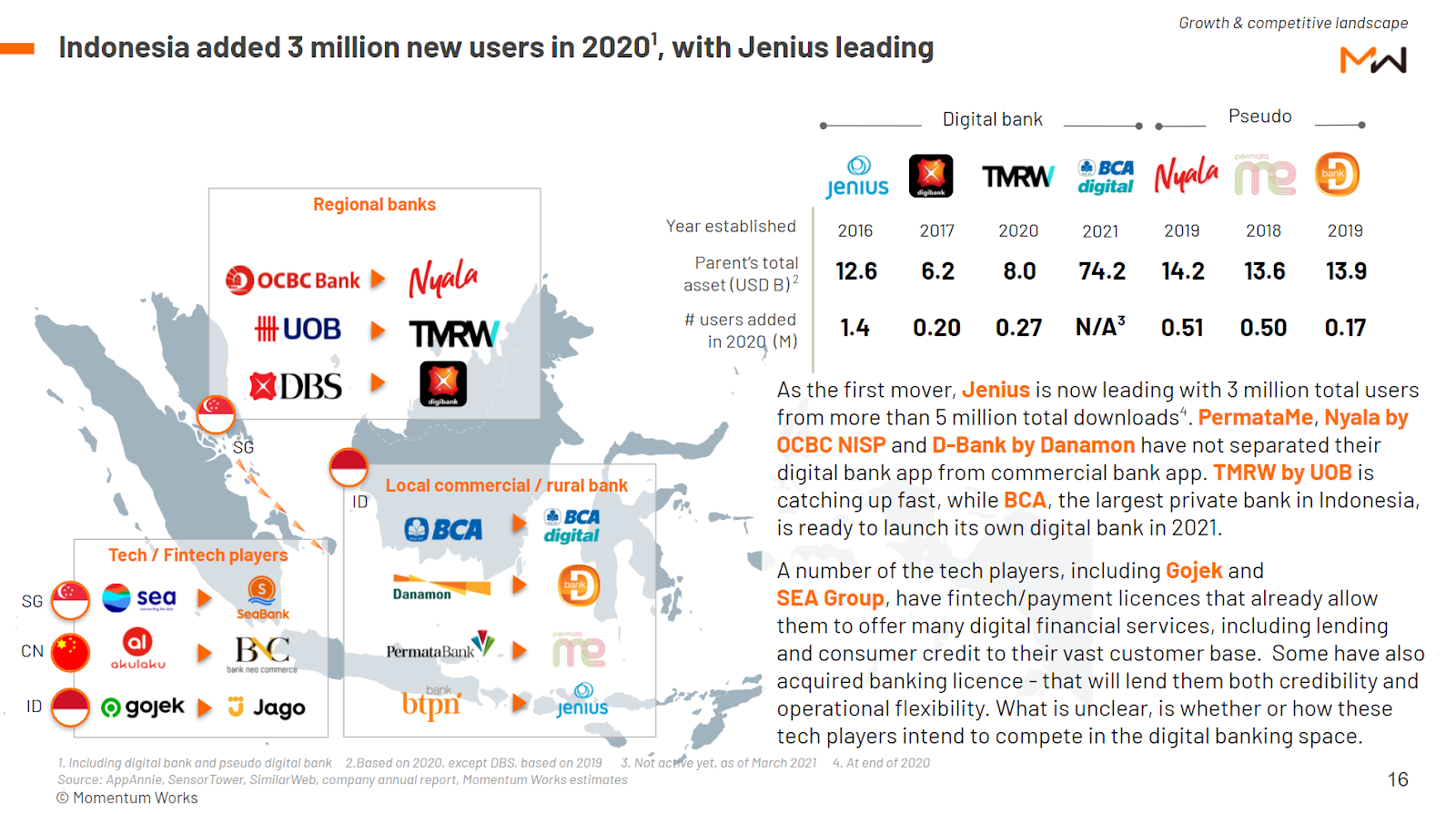

4. How is the competitive landscape for digital banks?

Leading players (in user numbers and traction) as of the end of 2020 are: Jenius by BTPN, TMRW by UOB and Digibank by DBS.

Pseudo digital bank players like PermataMe, Nyala by OCBC NISP and D-Bank by Danamon have not separated their digital bank app from its commercial bank app.

A number of tech players are also in the space like Seabank by Sea and Bank Jago by Gojek, however it is unclear to the outside world how they intend to compete in the digital banking space. We have our guesses.

5. I am particularly interested in understanding how the competition landscape will play up, given the aggressive tech players in the digital space and their tie ups with local banks.

Be it tech players or traditional banks – it’s crucial to understand the factors that are important to customers. The fundamentals of capturing the market do not change; however new players will have to be prepared as the competition will heat up.

Rational big tech players will prefer to have their profitable fintech services outside their digital bank (Check what has been happening with Ant Group in China). This will allow them more flexibility in leveraging their use base, and achieve profitability.

6. Who will lead this market, banks or fintech companies?

It’s too early to tell – but as mentioned, the fundamentals to capture the market don’t change. Banks and big tech companies have clear advantages over independent fintech companies in Indonesia.

7. How does Indonesia’s digital banks fare against international banks (in terms of features etc.)?

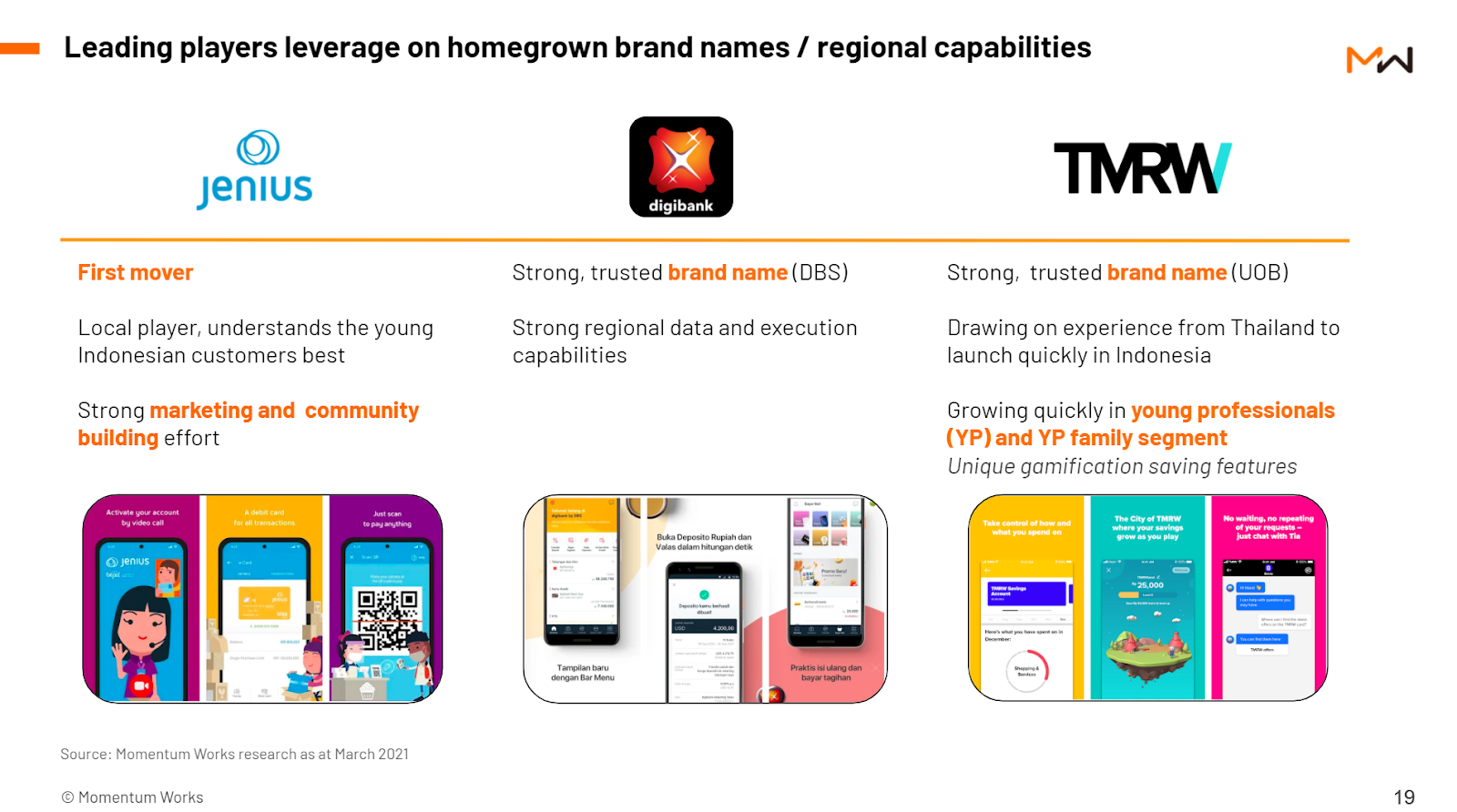

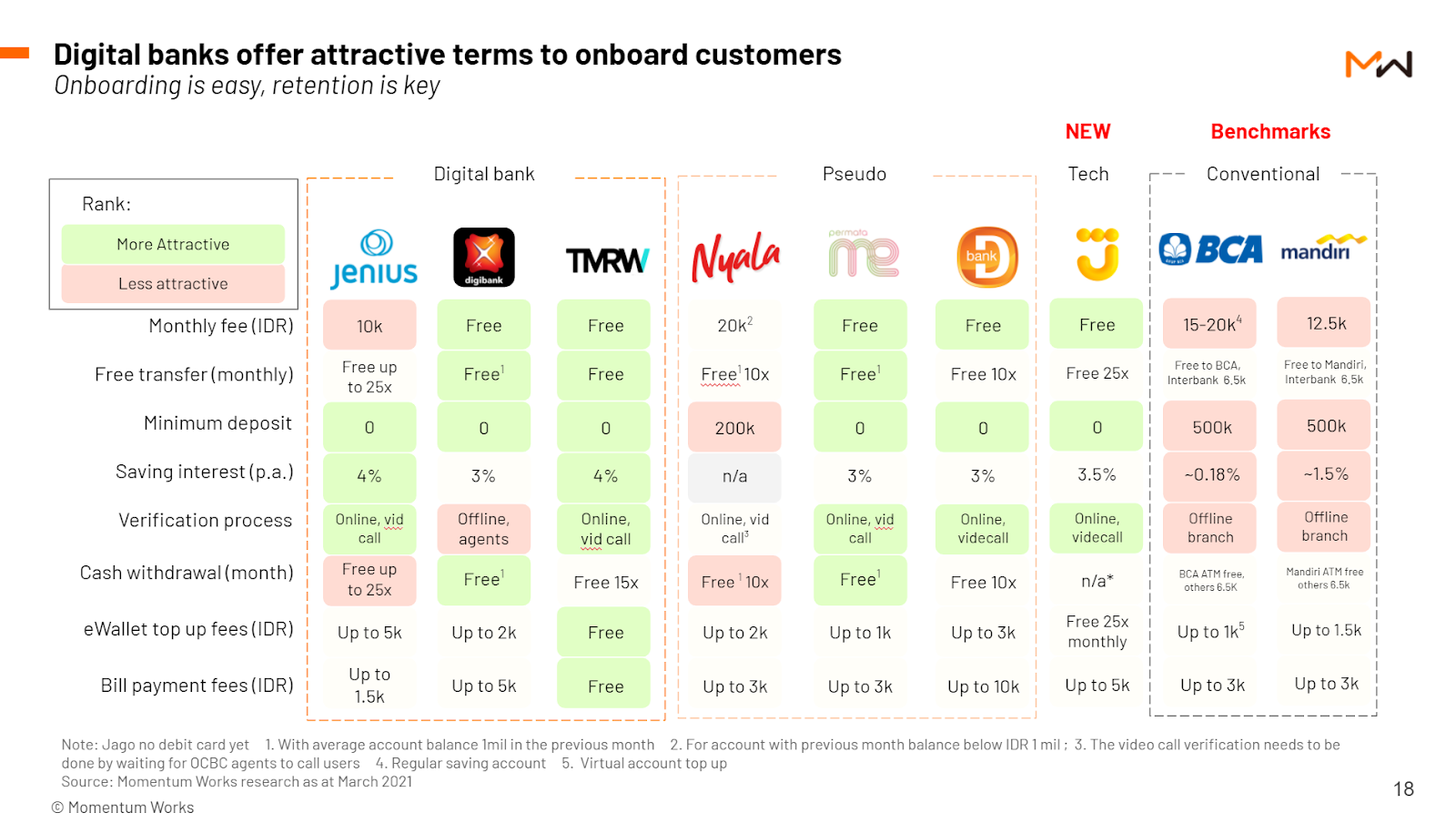

Currently, local digital banks offer a more localized product – for example Jenius has a feature to open multiple accounts for different purposes. However, international players bring interesting features from their experience in other markets, and adapt in Indonesia – like TMRW’s saving gamification feature. All in all, it’s still early and features are something that can be easily tweaked and improved.

The newer international digital banks like Digibank and TMRW currently offer attractive terms like free administration fees, transfer fees etc. They will probably adapt their tactics in response to evolving market dynamics.

8. What are the current initiatives undertaken by traditional banks to compete against digital banks?

Our colleagues in Indonesia say that traditional banks have started to refine their digital and mobile experience. Bank Rakyat Indonesia (BRI) and Bank Central Asia (BCA), two of the largest traditional banks are also preparing to launch their own digital banks. Traditional banks like BRI are also expanding into other fintech services, such as BNPL product BRI Ceria.

Growth

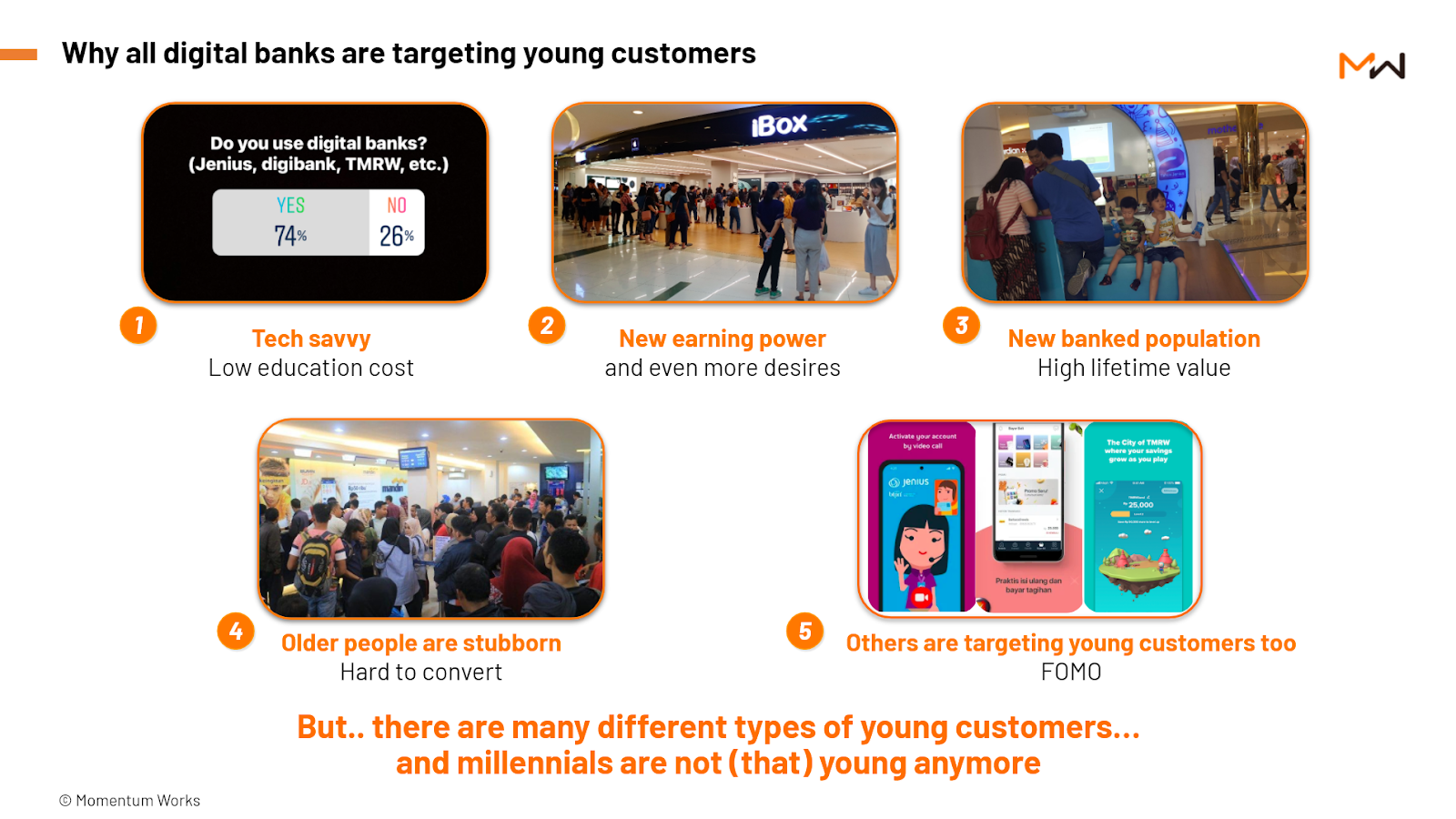

9. What are the key user acquisition channels?

As noted in the report, digital bank players are targeting young customers. Similar to what happened in the payment scene in Indonesia, digital banks offer attractive terms and promotions like cashbacks that would appeal to the younger population who want to stretch their dollar but still maintain a lifestyle.

Influencers and social media campaigns are also used extensively. We find community building efforts of Jenius quite interesting too.

With digital banks becoming more mainstream (at least to the urbanites), along with its fast and easy KYC process, it’s easy for customers to have 3-4 digital bank accounts. What will make them ultimately use one over the other will be the type of features, ease of use and product reliability – and of course, good terms.

10. How might players win deposits?

In the short term, players would probably need to try everything to create as many touch points as they can with customers. But ultimately it would be the points mentioned about in the question above, as well as trust. DBS, UOB and the large Indonesian banks like BCA have no problem in trust.

11. How does the infrastructure layer differ between traditional and digital banks?

Digital banks are ultimately still a bank – and need core banking and other essential systems. For digital banks, there is legacy baggage preventing them from moving faster. How do new players acquire the right talent to build such systems in a flexible, scalable but yet secure and compliant way is worth watching for.

12. Can you shed some colour on potential unit economics, or how it will evolve?

This question will require a more detailed analysis – especially on the potential and evolution part. We look to include that in a future update of our Digital Banks in Indonesia report.

13. How will the growth trajectory differ from international markets (local nuances)?

Each market is significantly different from each other. We expect the competition to heat up in the country as leading players continue to expand, and improve, while more new players join the fray.

Over time, there will be a few dominant players that will lead the space (won’t be winner takes all in this instance).

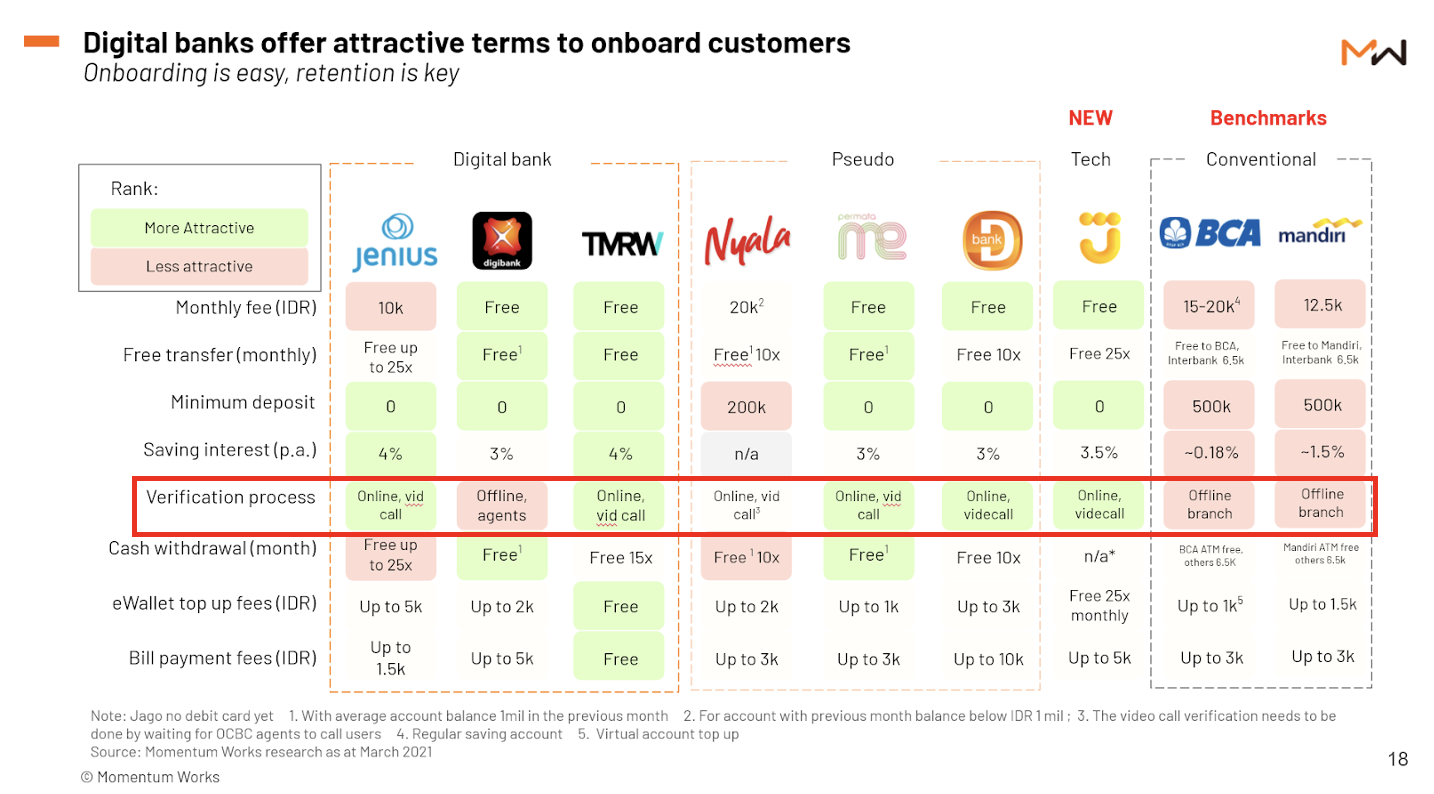

14. Can you also shed some light on the KYC process? How different is it for digital banks, compared to traditional banks?

Mostly online (and pretty fast), with no branch visit required. Refer the following screenshot from the report for more details:

15. Are existing digibanks building all the tech for core banking in-house? Or are they powered by BaaS?

Established banks would already have the core banking system – and hopefully capabilities to build a new one if necessary.

We know a few new players who have hired folks to build core banking in-house. A few BaaS players have touted their ware – we are not sure about the take up yet.

16. Do you know any core banking companies that are entering the Indonesia market?

Refer to the answer to the question above.

17. From your view, do people tend to seek basic banking features (simple transactions, balance, etc) or all in one banking app (mortgage, bonds purchase, etc)?

You will end up having all-in-one, but you need to start from a key offering so as not to confuse initial users who are yet new to your platform.

That methodology is not that different from that of super apps.