We wrote a while ago arguing that Tencent is fundamentally still a sound company, despite the share price drops at that time.

Recently the stock price, with some ups and down, sank further, almost wiping out the gains over the last 12 months:

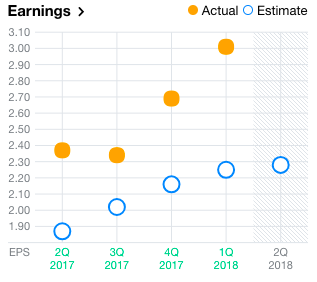

For a company that has almost consistently beaten analyst expectations for the last quarters, what happened?

The company specific worries are:

- Slowing gaming revenue: its “glory of kings” mobile game, which used to bring in tens of millions each day, is slowing down in terms of user growth and spend. There isn’t other game from the group that shows the same promise

- Still no big advertising income in sight: WeChat as a social media and chat platform is still largely free of plaster ads.

- The threat of products by Toutiao (called Byte Dance now), and notably Douyin (Chinese version of Tik Tok). The following image is telling – from July 2017 to June 2018: the time spent on Tencent’s product by Chinese internet users declined by 6.6%, while that of Toutiao products grew by 6.2%:

These are not the only reasons. There are external factors as well:

- The rising interest rates in the US and the appreciating US dollar draw funds back to the US;

- The slowdown of liquidity coming from Mainland China through the cross border investment channel;

- The rush to Hong Kong IPO by the many Chinese internet unicorns that further spreads the money in the market.

Fundamentally we believe Tencent is still a good company: the external factors are not perpetual; and Toutiao might receive further curbs from the government.

However, finding out a proper way to monetize through ads would probably be a main challenge for Tencent. This is similar to how Facebook could unlock the huge value of Whatsapp.

All eyes now are probably on 15th of August, when Tencent announces it Q2 and interim results.