")

This article was originally published in Chinese by Vision Plus Capital, translated into English by the Momentum Works team.

On November 11, Stori, a financial technology company in Latin America, announced that it has completed US$125 million led by GGV and GIC. The company has also secured US$75 million in debt financing from impact-focused debt capital provider Community Investment Management.

Not long ago, Advance Intelligence Group (hereinafter referred to as Advance), a leading financial technology company in Southeast Asia, announced more than US$400 million financing from renowned investment institutions including SoftBank and Warburg Pincus. Advance also secured a US$500 million credit facility from Standard Chartered bank.

Within one month, the two fintech companies set a new round of financing records in their respective regions, which is worth paying attention to. What’s more interesting is that Hangzhou-based Vision Plus Capital is the early investor of both companies.

This makes us wonder why Vision Plus will invest in these two companies? What is the VC’s cross-border investment strategy? With these two questions, we took Vision Plus Capital as a case study and chatted with their cross-border investment team, hoping to find some answers.

Early strategy for Latam market

According to Yiran Liu, a partner of Vision Plus Capital, it is fate that brought Vision Plus to invest in Latin America: In 2018, Yiran visited investment institutions in the United States and talked about the Latin American market during the meeting. Several American VCs looked at each other, thinking that the opportunity was still immature.

At that time, many investment institutions in Asia had actively invested in the Southeast Asian market (for example, Vision Plus had already invested in Advance at that time), but US VCs seemed to be not interested. Yiran realized that the Latin America market could be an opportunity as it is underestimated just like the Southeast Asian market. However, no suitable investment target was found at that time.

Coincidentally, Daqing Ye, the co-founder and CEO of Rong360 (NYSE: JT), was also expanding fintech outside China at that time. He and several founders of Stori were all old colleagues from Capital One (innovators in retail finance and financial technology in the United States). After the early angel investment from Daqing, the Stori team set the target market in Latin America.

In the summer of 2018, Ye Daqing and Liu Yiran met on a business trip in the United States, where they chatted about the Latin American market and Stori. After the meeting, Vision Plus decided to go to Mexico for field research.

Group photo of Liu Yiran (4th from the left, back row) and local Stori staff

Luo Zhang, vice president of Vision Plus Capital, recalled that during the trip to México, they found a very misplaced phenomenon- As a country with a population of over 100 million, Mexico’s per capita GDP is close to that of China.

Because of its proximity to the US, the entire country’s consumption and payment infrastructure is relatively sound. However, this country’s banking industry is dominated by European and US banks, and only concentrates on serving high-end users. A large number of middle-class and low-income people will spend several months handling savings accounts because of the inefficient service system.

“With the development of the Mobile Internet, inclusive finance in Latin America will inevitably show an explosive trend,” said Luo Zhang. “Under the existing financial system, the risk control data, risk control models, and operational talents required for inclusive finance need to be re-integrated and re-built, which gives a historic opportunity to the entrepreneurial team with risk control capabilities, risk control experience, and financial product service experience.”

After comprehensively inspecting the capabilities and experience of the Stori team in the financial field, Vision Plus confirmed investment intentions. Looking back now, Vision Plus’s prediction can be said to be very accurate. Just after they invested in Stori, the Latin American market began to heat up rapidly. Many American VCs went there, and many international capitals began to actively deploy in Latin America (for example, SoftBank established the first Latin American fund in 2018).

Now, Fintech has become the most attractive industry in Latin America. According to statistics, one third of Mexico’s financing for startup technology companies in the past 12 months has been concentrated in the field of financial technology.

Pathways: American Express vs Capital One

Looking back, although there were huge opportunities in the Latin American market, Vision Plus was still facing the question of how to do it and how to cut it in. Vision Plus first learned the development history of the leading regional giant Nubank in Brazil, and put forward different ideas on this basis: Brazil and México are both emerging markets- Brazil may be suitable for the high-quality service model similar to American Express by attracting existing customer base, while México needs CapitalOne’s ability to price risk by directly opening up the growth market.

The reason for proposing this different idea is the different financial patterns of the two countries. One is for historical reasons – it is very rare for Brazil to have a high credit card penetration rate (about 50%) while having a high recurring interest rate (about 200% annualized). That is to say, although a large number of users have credit cards, they are actually “underbanked”. Therefore, NuBank’s model came in and gained a huge success by providing digital products and high-quality services to convert existing users (with bank risk control and credit records).

On the other hand, Mexico’s credit card penetration rate is only 15%, but the revolving interest rate is more reasonable (annualized less than 100%). A large number of blue ocean markets have not been tapped, and the users here are “unbanked”. This situation is more like the early US credit card market years ago. Capital One, where Stori team members have worked before, is a famous financial giant that started with subprime risk pricing in the history of the United States. Today’s mobile internet era has injected more data and vitality into Capital One’s methodology. This model has also been fully proven by new markets such as China.

After such investigations and judgments, Vision Plus took the lead to invest in Stori’s Series A when there was almost no business data in the very early stage. The development of the past few years after the investment has also initially verified Vision Plus’s judgment at that time. While Stori is rapidly growing, the risk level has been maintained within a stable and reasonable range. Along the way, Stori has gradually been recognized by other investment institutions.

In addition, Vision Plus also shared some other interesting comparisons. For example, it is generally believed that the Mexican market has limited space, but this may not be the case after careful calculation.

México is the second largest economy in Latin America and the tenth most populous country in the world, with a population of 120 million (compared to 210 million in Brazil). Brazil’s excessively high credit interest rates have led to a very low percentage of users’ recurring interest rates (cannot afford to borrow), while México’s recurring interest rates are closer to a mature market, like the United States, and the user lifetime value is more mature. Both markets have great potential.

In addition, compared with emerging markets such as Southeast Asia, Latin America has another difference in marketing: the Mexican market has a strong response to the new inclusive credit card products, and a large number of users voluntarily recommend this kind of product to their relatives and friends, which significantly reduces the cost of customer acquisition.

On the other hand, in the Southeast Asian market, because the credit penetration rate is too low, the cost of acquiring a high-quality credit customer is often too high. The mainstream approach of startups is often to introduce higher interest rate online loan products as introductory products to screen and select high-quality customers. The difference between these two introductory products has also become an interesting epitome of the different stages of credit penetration in the two markets.

Pandemic accelerates fintech development

Yiran Liu said that from a global perspective, financial technology is still a huge opportunity worldwide. The financial industry and the retail industry have similar market sizes. Therefore, Fintech, as the digitized financial industry, also has huge development prospects in emerging markets just like e-commerce, which digitizes the retail industry.

Take México as an example. According to statistics, more than 60% of the population do not have suitable financial credit services, but nearly 70% of the population have used mobile internet or e-commerce services, and about 90% of the consumption is still in the form of cash. This mismatch allows financial technology companies to usher in leapfrog development- a large number of inclusive finance and consumer finance businesses can be reconstructed, various innovative models such as digital banking and virtual credit cards have emerged, and transactions and payments are deeply integrated.

The outbreak of the covid-19 pandemic in 2020 has accelerated the rapid penetration of financial technology. With the restrictions on offline activities, it is inconvenient for people to go to offline financial institutions, and cash payments have become unsafe and inconvenient. A large number of consumer transactions by individuals and companies have begun to shift online. The demand for digital financial services has exploded rapidly.

At the same time, due to the turbulent employment and economic environment, the demand for flexible payments and loans has also risen sharply. The new generation of financial technology companies adopt online digital models to directly acquire customers, operate and control risks, and provide more inclusive and flexible financial solutions based on data and AI, reducing the dependence on offline networks and service labor, while greatly expanding the customer base not yet covered by traditional financial services. The Fintech industry has entered the best time for development in history.

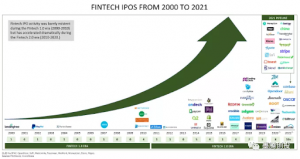

In the past 12 months alone, many Fintech super unicorns such as Affirm, Upstart, Sofi, Robinhood, CoinBase, Marqeta, and Wise have gone public one after another. It is believed that several large companies such as Chime, Stripe, Klarna, Nubank, and Plaid are also preparing for IPO. Fintech is in an unprecedented explosion.

Vision Plus’s own portfolio companies also developed rapidly during the pandemic- Atome under Advance launched its BNPL service, which has been widely accepted by online and offline merchants, because BNPL serves as a new channel to attract consumers during the pandemic; Stori’s credit card business has sprung up in México as a lot of new users joined through referral. The word-of-mouth marketing allows the number of cards issued to quickly approach one million. The reason behind this is that the demand for credit card payments, with surging user numbers, has been further amplified during the pandemic.

Vision Plus’s Investment Logic: New Time Machine Theory

From our understanding, Vision Plus has always been researching and exploring cross-border investment. In fact, as early as 2017, Vision Plus put forward the “time machine” theory for cross-border investment. They believe that the development of China’s PC internet has learned from the path of the United States in the past ten years, and the development path of China’s mobile internet in the next decade will be a reference for other emerging markets.

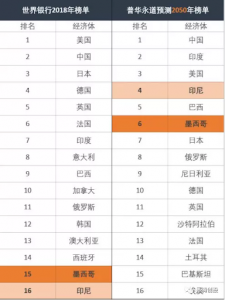

Interestingly, in 2019, PWC released a world economic forecast, predicting that market sizes in emerging markets such as Indonesia and Mexico will increase significantly in the next 30 years, and eventually surpass developed countries such as Japan, Germany, and the United Kingdom. This also represents the growth potential of these emerging economies.

As cross-border entrepreneurship continues to bloom in the past two years, VisionPlus has updated their “new time machine” theory: a wave of structural opportunities is emerging around the world. As emerging markets continue to embrace the mobile internet, more and more use cases will shift online, but traditional financial services and payment methods have not kept up in time, so there is a mismatch between high online penetration and low financial coverage.

“Cross-border investment is to find opportunities from mismatches in various fields in emerging markets.” said Qi Wang, another partner of Vision Plus Capital who focuses on cross-border investment.

Therefore, in addition to Fintech, Vision Plus is using a full coverage strategy to deploy a complete ecological layout of all cross-border fields. The business areas include e-commerce, branding, finance, logistics and others.

E-commerce: Fordeal, a cross-border e-commerce company invested by Vision Plus in early years, has rapidly grown into a quasi-unicorn enterprise. With the advantages of Chinese goods, Fordeal has expanded its business scope from the Middle East to Europe and other regions. Since then, Vision Plus has made early investments in brands in many fields such as smart home appliances, consumer electronics, and beauty products. The entrepreneurs are all mature teams that are familiar with China’s supply chain and needs in the target countries.

Logistics: Vision Plus has successively invested in several companies such as Speedaf Express and Joying Box in the past two years. Among them, Speedaf Express’s main business is China-Africa logistics and local delivery services in Africa. The founding team comes from Transsion, who has a deep understanding of the local market and Africa’s express delivery system; Joying Box team comes from the leading cross-border payment company Lianlian and cross-border e-commerce company JollyChic. Joying Box is committed to establishing a full-process digital, efficient, real-time and stable cross-border logistics aggregation platform and infrastructure.

Ecosystem Enabler: In the past two years, Vision Plus’s cross-border investment has gradually expanded to ecosystem-enabling SaaS business, including cross-border marketing, placement, customer service and others, striving to serve cross-border merchants and to solve the pain points behind the industry chain. The team has many senior executives from industry giants such as Alibaba, who have a deep understanding of cross-border business and the needs of small and medium-sized merchants.

In addition to the investment logic “new time machine”, we believe that Vision Plus’s cross-border investment in all-round ecosystem coverage is also inseparable from the knowledge and experience of its management team. If you look closely at the Vision Plus’s investment team, it is not difficult to see that many of the senior executives in Vision Plus’s team come from leading domestic e-commerce companies and have investment experience in large e-commerce and trading platforms.

“Cross-border entrepreneurship at the beginning was more of the output of platform models and experience, but with the continuous development of logistics, financial and other infrastructures in recent years, more innovative categories, brands, channels, and vertical industrial collaboration all have huge opportunities. And our cross-border investment has gradually spanned from platform opportunities to cross-border smart products, cross-border supply chains and brands, and the entire ecosystem chain around cross-border service provision.” Qi Wang said.