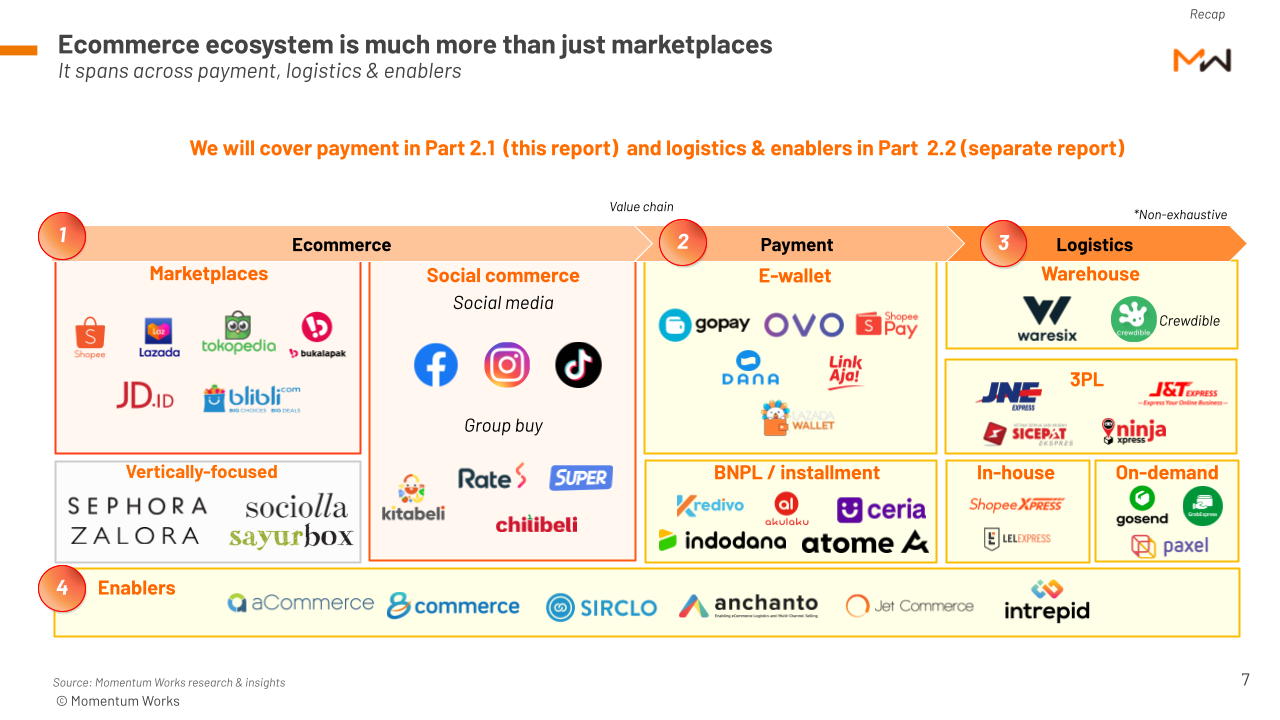

Following our first instalment on ecommerce marketplaces, Blooming Ecommerce in Indonesia Part 2.1 Ecosystem – Payment shares our perspectives on landscape, players dynamics and lessons we can draw from international players.

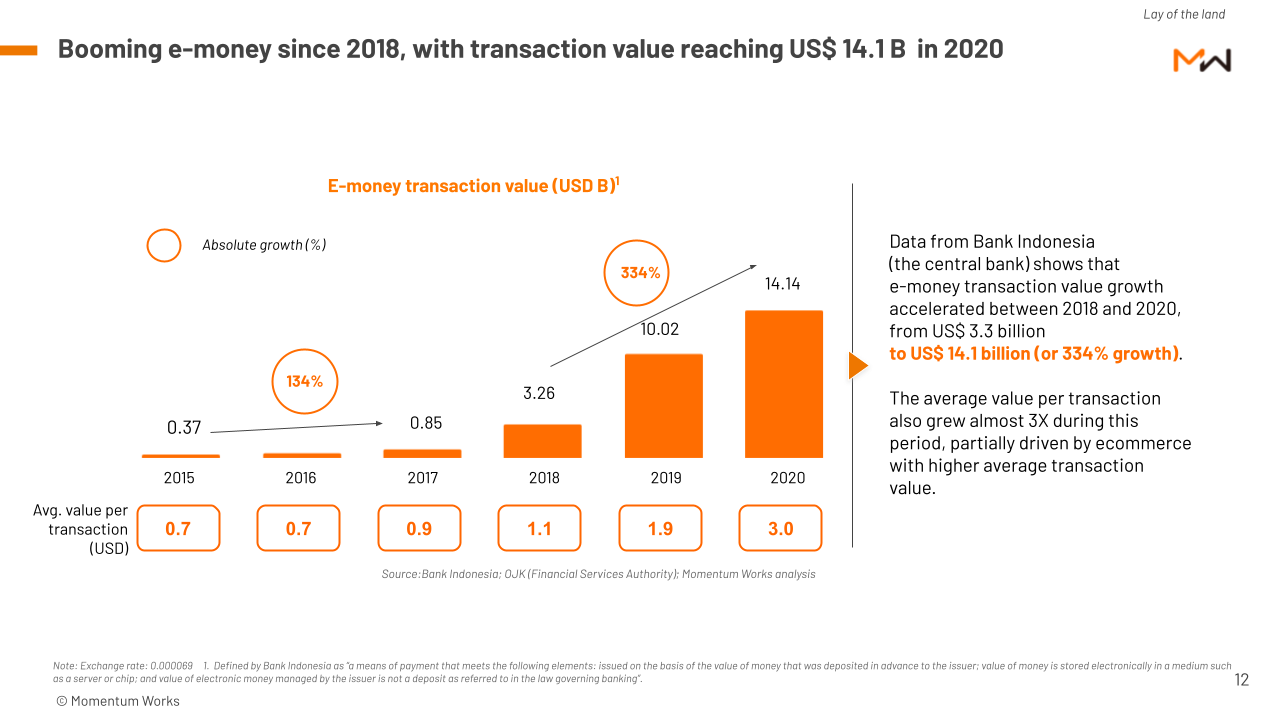

In Indonesia, ecommerce is increasingly a key driver for digital payment growth. Between 2018-20, we see that e-money transaction value grew by 334%. Fintech derivatives (e.g.: E-wallet, BNPL) are leapfrogging to provide innovative payment options that are convenient, fast and cost-saving (e.g.: cashbacks).

We will also deep dive into key e-wallet players: Dana, LinkAja, OVO, ShopeePay, and GoPay, as well as BNPL players: Akulaku, Kredivo, Ceria and ShopeePayLater.

Below are some key insights from the report:

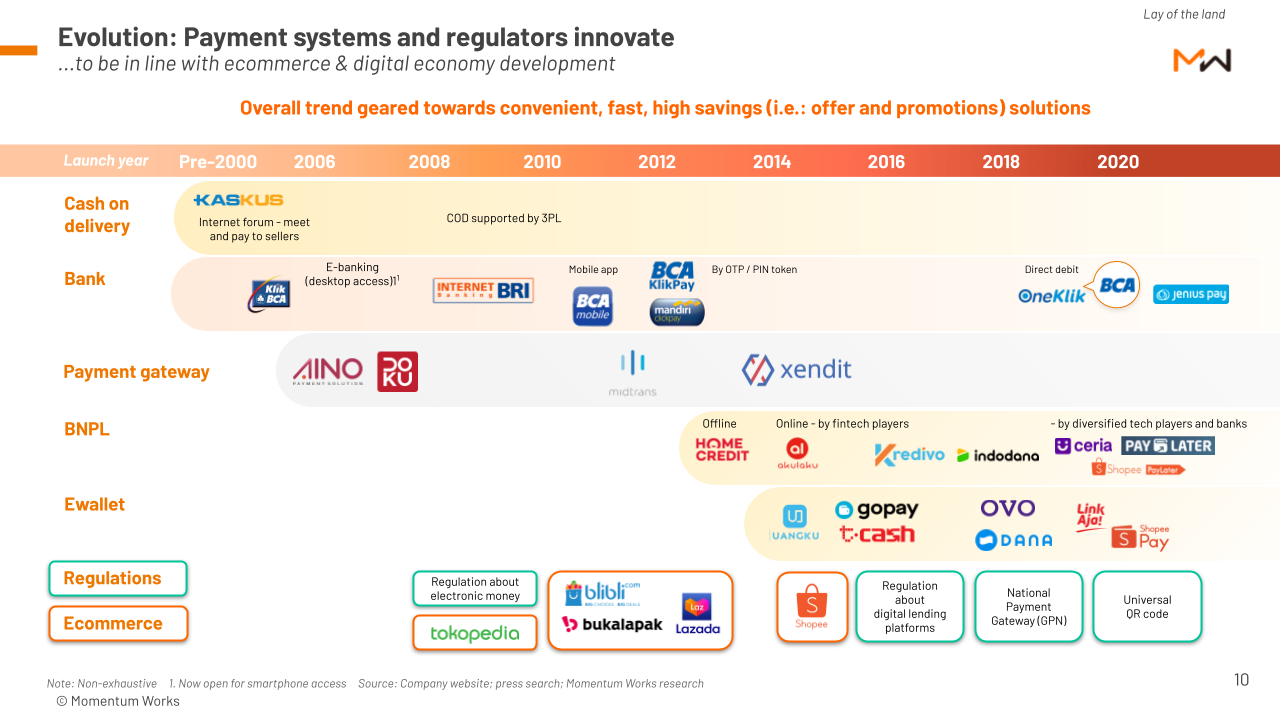

1. Payment systems and regulators innovate alongside ecommerce & digital economy development

Since 2001, banks have been innovating to provide convenient payment solutions in line with ecommerce development. Fintech players have also emerged to provide simpler, easier and faster payment solutions.

However, cash-based payment remains one of the key modes of ecommerce payment in Indonesia as it provides trust among the unbanked and new-to-ecommerce population.

2. E-money transaction value grew from US$ 3.3 billion in 2018 to US$ 14.1 billion in 2020

The average value per transaction also grew 3 times during this period, partially driven by ecommerce with a higher average translation value.

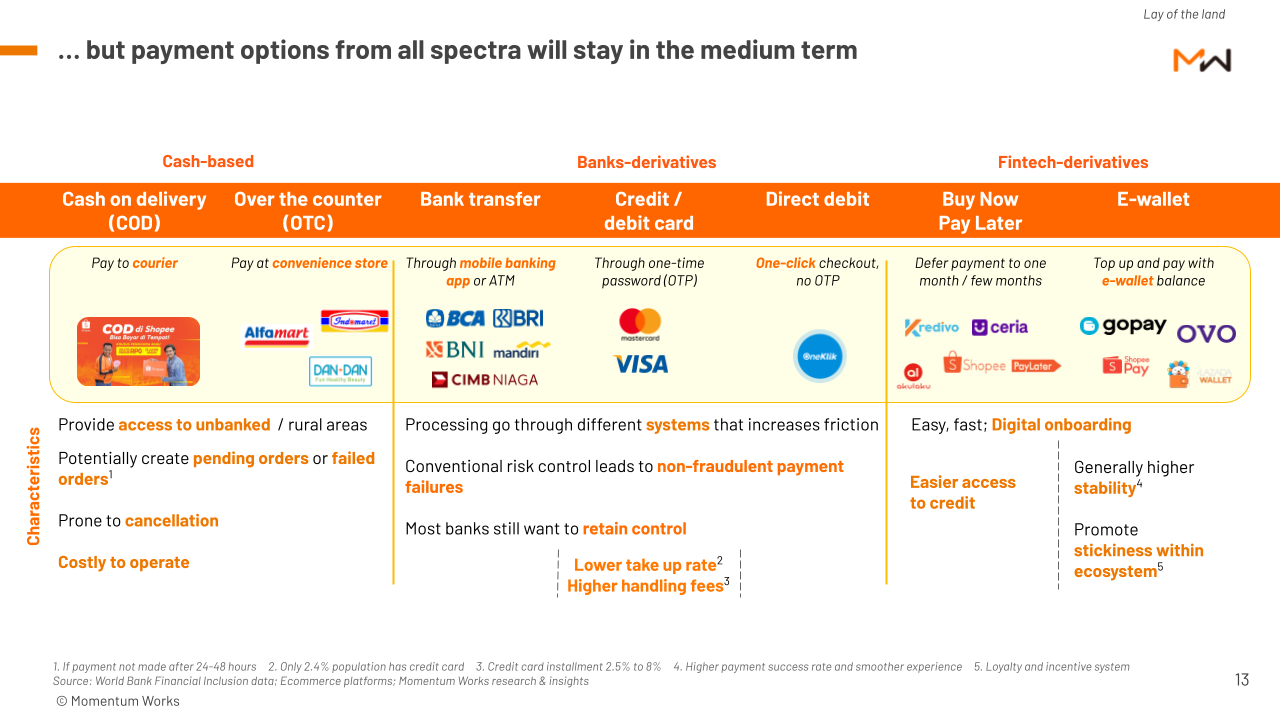

3. Despite high interest in e-wallet, payment options from all spectra will stay in the medium term

Each payment option has its own characteristics. Cash is popular but costly to operate. Bank-derivatives is preferred but usage is still lower, and many still rely on legacy processing systems. Fintech-derivatives payment methods are fast and easy to use, but there are still many new barriers to entry. E-wallets generate greater stability and promote stickiness within the ecosystem, whereas BNPL gives easier credit access.

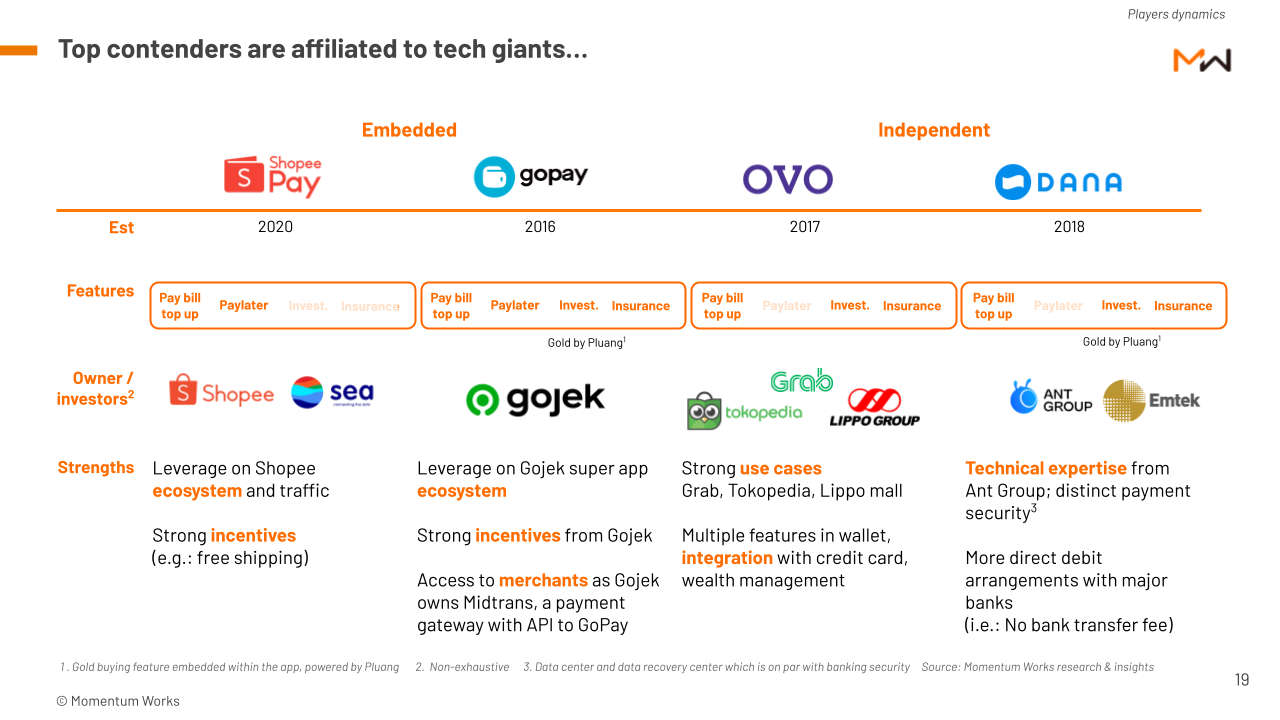

4. Top e-wallet players are affiliated with tech giants

The top e-wallet players can be divided into 2 categories – embedded and independent. Embedded players include ShopeePay and GoPay. Independent players include OVO and Dana.

Each has its strengths and characteristics. ShopeePay and Gojek leverage their respective ecosystems. On the other hand, OVO has strong use cases and Dana has technical expertise from owners/investors.

Independent and embedded e-wallet players need to be benchmarked differently, as their strategy and focus could be quite different.

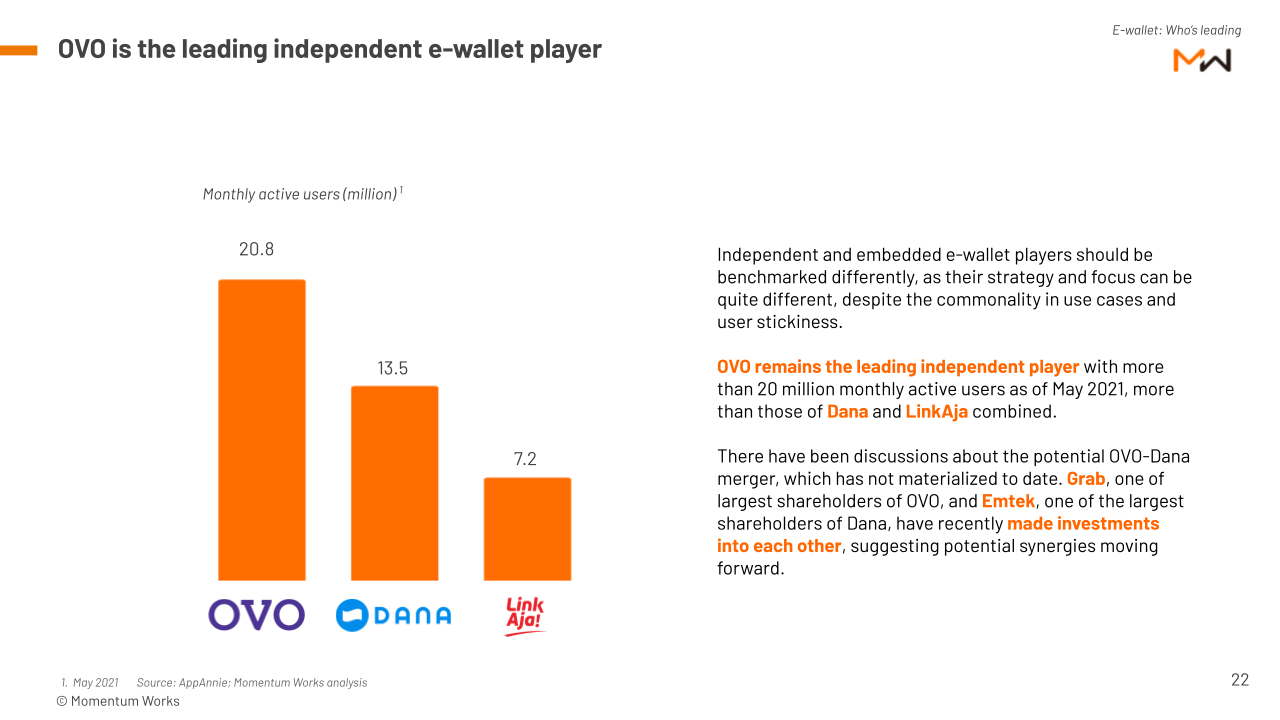

5. With more than 20 mil users, OVO is the leading independent e-wallet player

There could be potential synergies or mergers between OVO and Dana in the future. Watch this space.

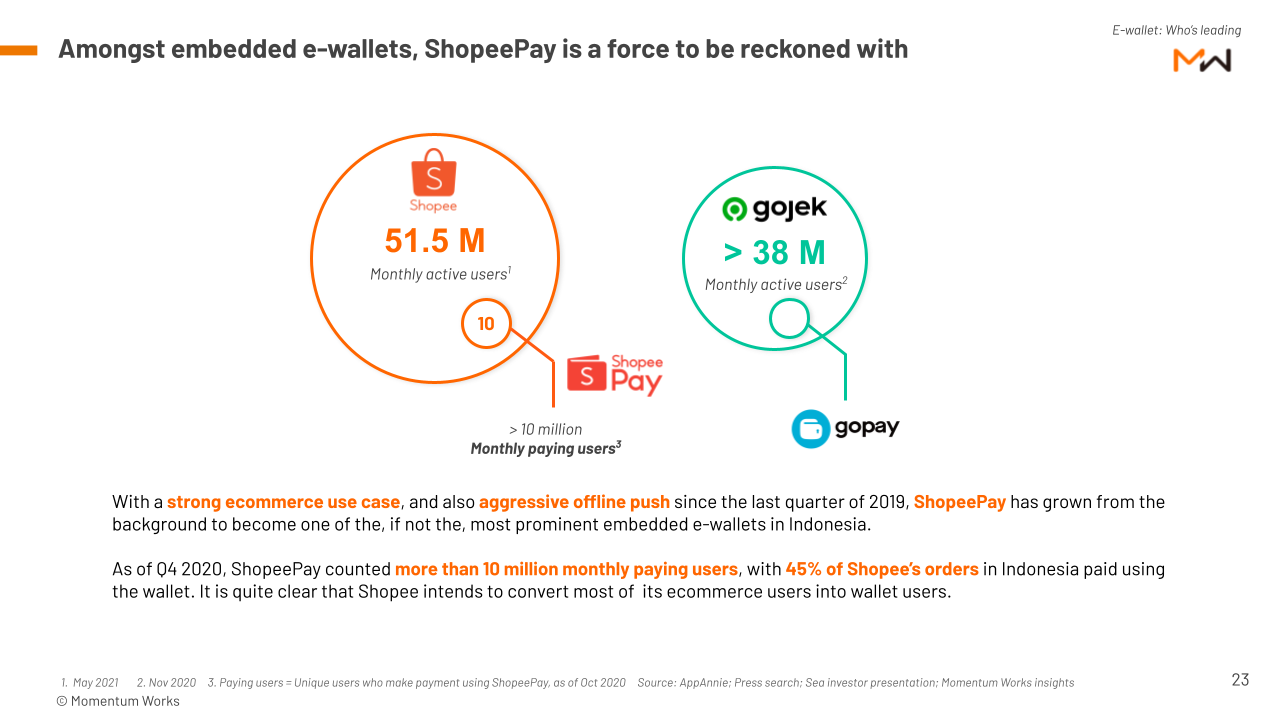

6. ShoppePay’s position among embedded e-wallets should be recognised

The growth of ShopeePay has been prominent through strong ecommerce use cases and aggressive offline push. In Q4 2020 it had more than 10 million monthly paying users, with 45% of Shopee’s orders in Indonesia paid using the wallet.

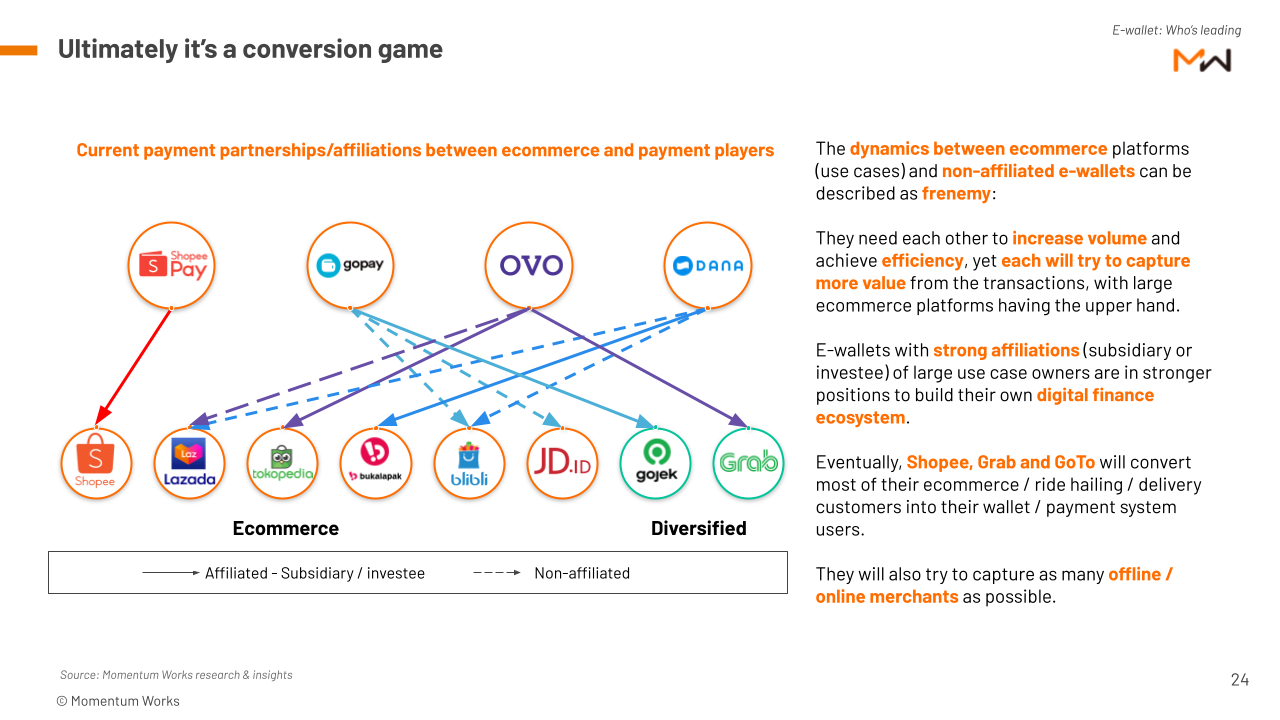

7. Ultimately, it’s a conversion game

Ecommerce platforms and e-wallets need each other to increase volume and efficiency. E-wallets with strong affiliations with large use case owners are in stronger positions to build their own digital finance ecosystem.

Eventually, large use case owners like Shopee, Grab and Goto will convert most of their traffic to their respective wallet / payment system.

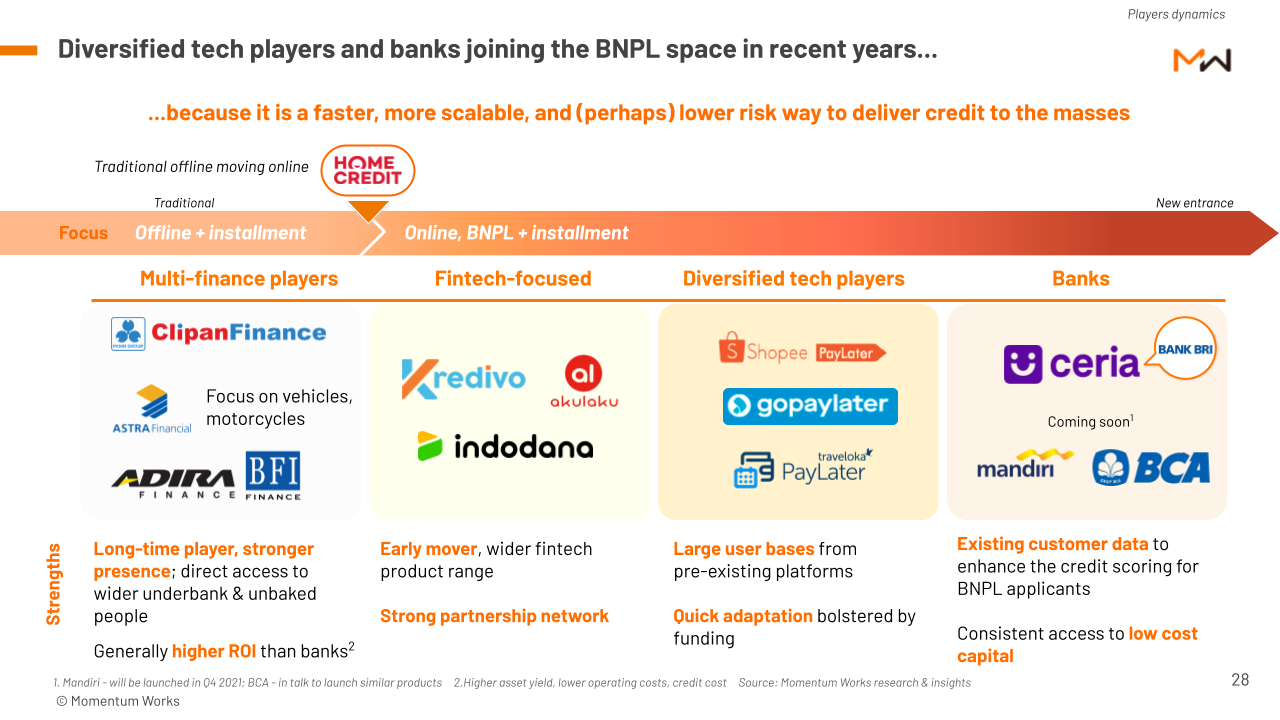

8. In recent years, the multitude of diversified tech players and banks have joined the BNPL space

The BNPL mode is a faster, more scalable and probably lower-risk way to deliver credit to the masses. Fintech-focused companies, diversified tech players, and banks are all joining the bandwagon and each player comes with different leverages.

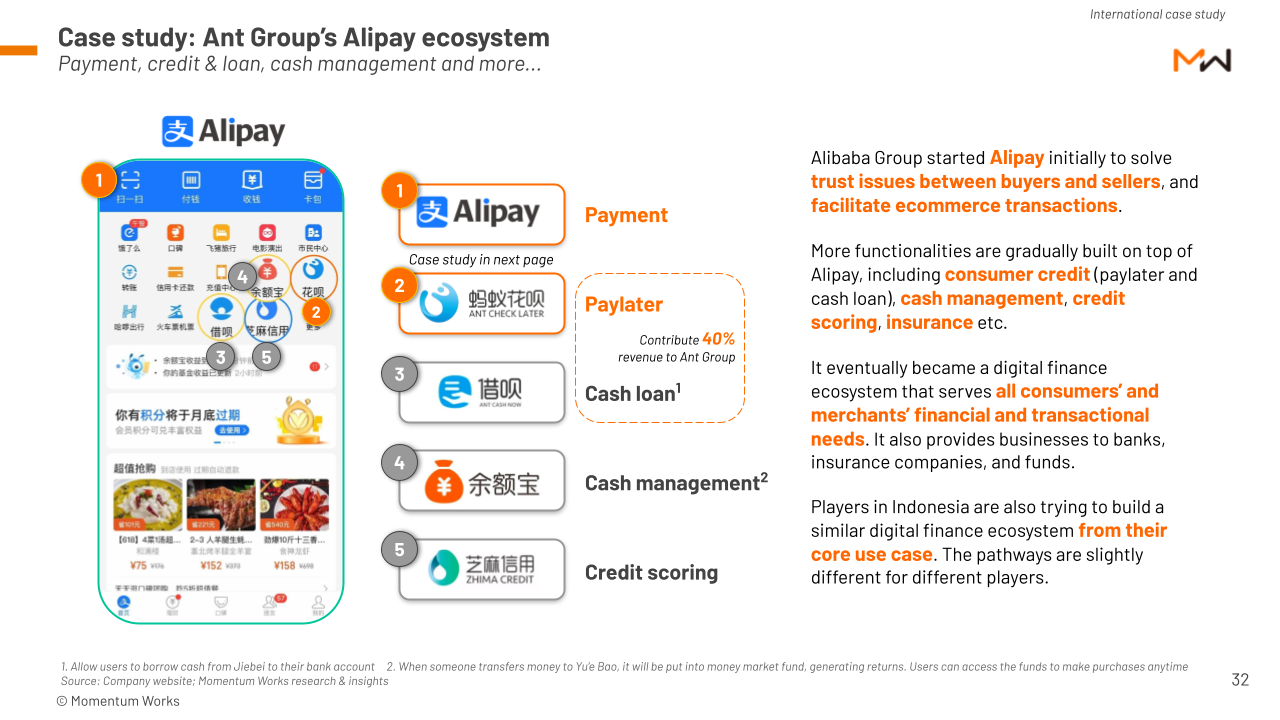

9. Case study: Alipay ecosystem spans across payment, credit, loan, cash management and more

Alipay, as we know today, is a digital finance ecosystem. However, it started off simply to facilitate ecommerce transactions, and subsequently, consumer credit (paylater and cash loan), cash management, credit insurance features were added. There are many references that Southeast Asian ecommerce payment companies can take from Alipay.

Get the Blooming Ecommerce in Indonesia Part 2.1: Ecosystem – Payment

You can get the full report by clicking here.

4.0")