In March, we wrote about Chinese AI unicorns have their IPO applications terminated. One of the concerned companies is YITU Technology in the visual space.

On 30 June, the company and its investment bankers finally officially withdrew their IPO application, first submitted on 4 November 2020:

We heard from the industry that the company intends to lay off 70% of its headcount, and try again. The lay off would boost the profitability.

We heard from the industry that the company intends to lay off 70% of its headcount, and try again. The lay off would boost the profitability.

Negative equity

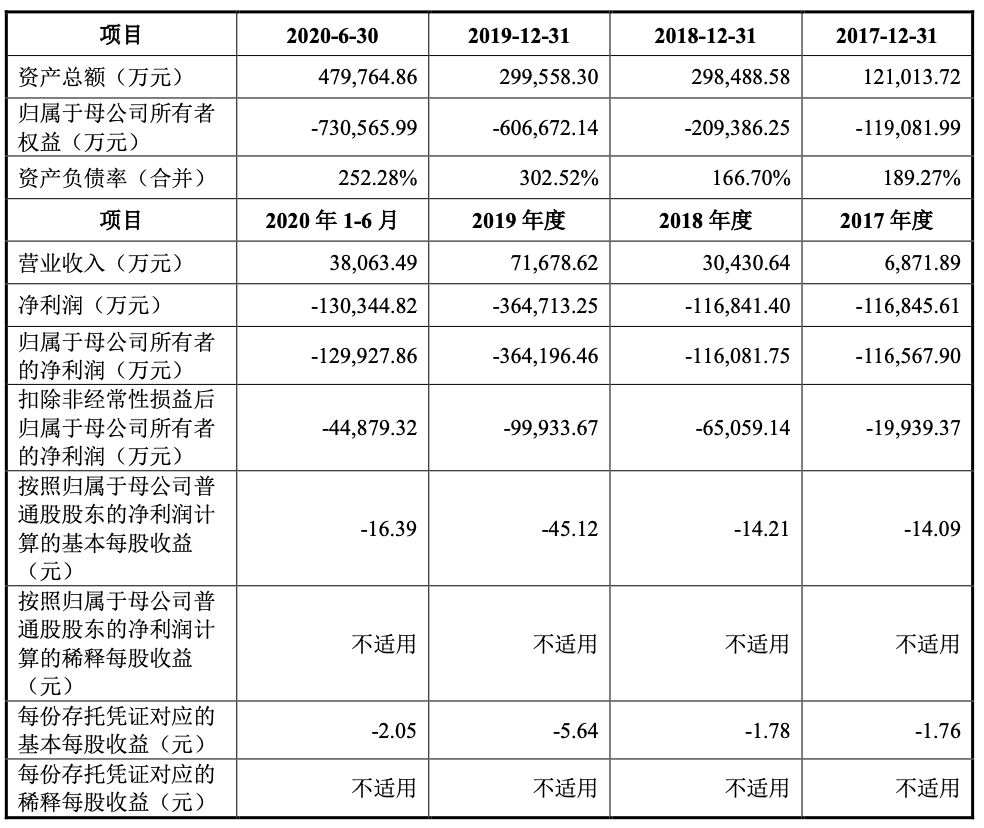

As you can see from the financials below (in Chinese) – Yitu had a negative equity of CNY 7.3 billion (US$1.13 million) as of 30 June 2020. Its revenue in the first half of 2020 was CNY 380 million, while it net loss was CNY 1.3 billion:

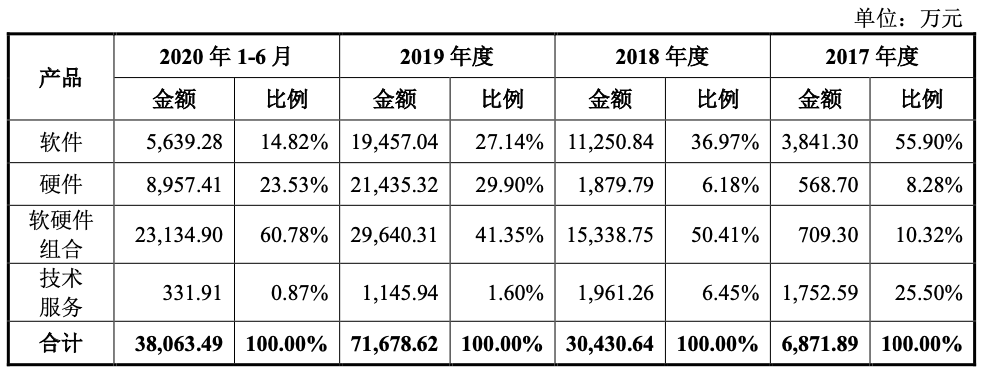

The revenue comes from (the same order as in the following table): software, hardware, combination of software and hardware, technical services. The combination represents 60.78% of the total revenue in the first half of 2020, a sign that Yitu does a lot of SI work.

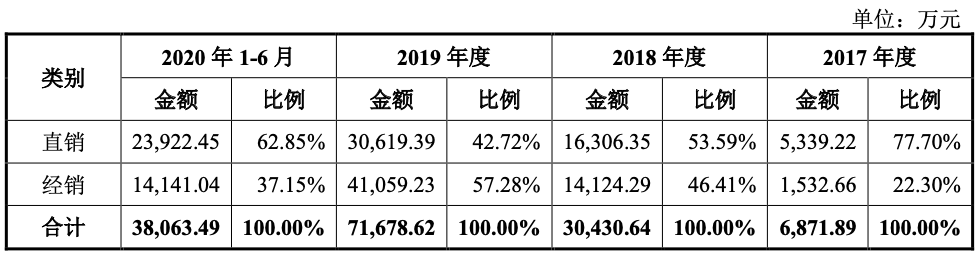

In the first half of 2020, 62.85% of the revenue came from direct sales, while the remaining came from channel. This is again a sign that Yitu is by itself a system integrator:

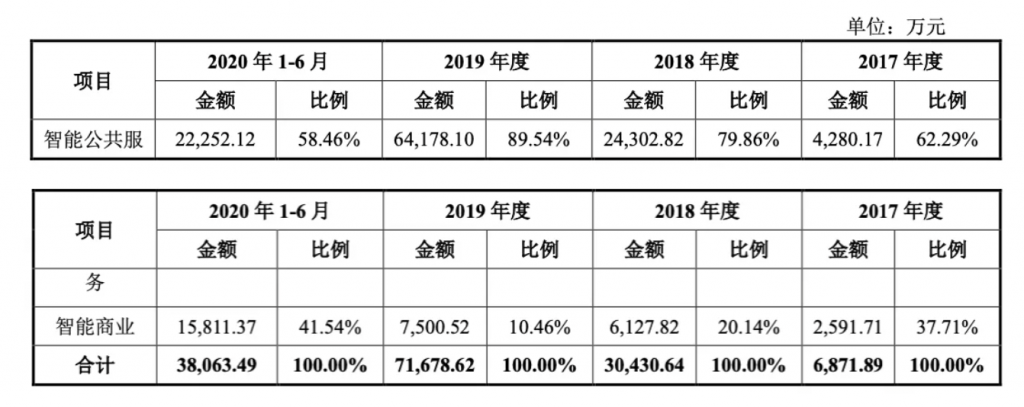

Public sector and domestic customer base

More than half (58.46%) of the revenue came from the public sector – this was already down from 2019, where 89.54% of the revenue came from the public sector.

This is another reason why Yitu probably can’t go anywhere else for IPO except in China’s domestic stock exchanges:

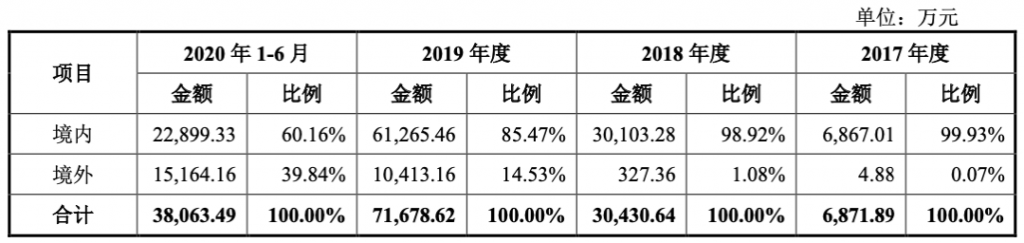

In the first half of 2020, 60.16% of revenue came from domestic customers – down from 85.47% in 2019:

The top customer in 2020 was VSTECS, a Singapore based distributor, and its Chinese subsidiary. The fourth biggest customers, interestingly, is Indonesia’s Salim Group, which contributes 10.91% of the revenue:

The top selling products include (in the same order as the following table): servers, cameras, work stations, technical service, and data services. Servers represented close to 40% of total sales in 2020, down from 66.93% in 2019:

R&D and salary costs

Another cause of concern (or a sign of long term commitment) is that the R&D cost of 2020 exceeded the revenue. In 2019 and 2018 R&D costs were almost as big as the revenue:

In the first half of 2020 alone, Yitu received CNY 65 million of government subsidies related to revenue, a significant surge from previous years:

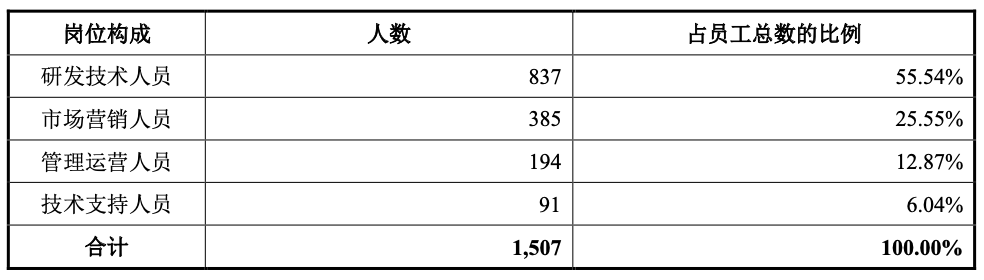

The company had a headcount of 1507, amongst which 837 (55.54%) are in R&D:

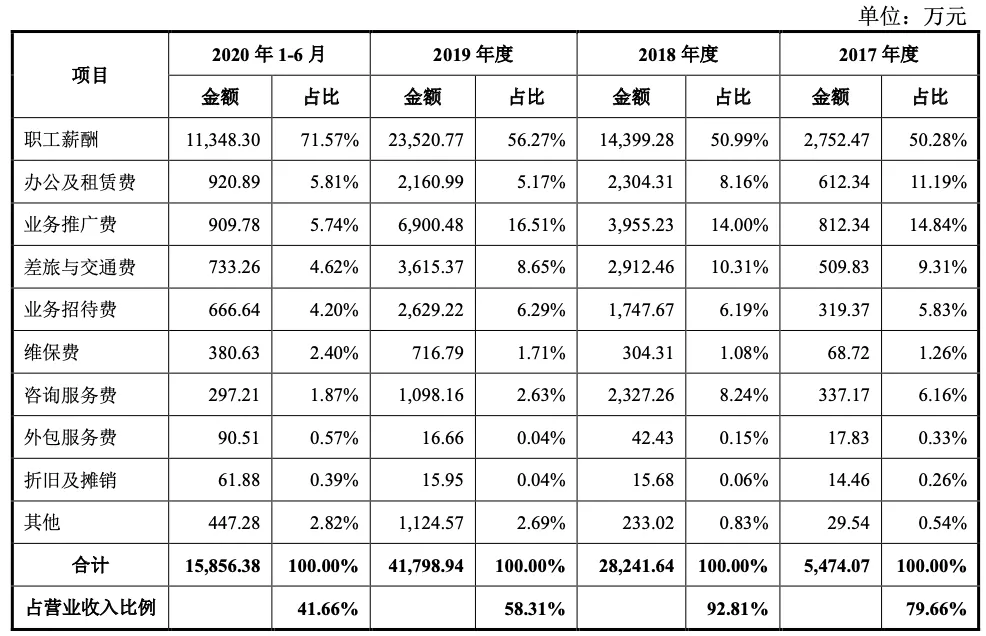

Half of the costs are salaries (which means recurring) – probably a key explanation why they are expecting large layoffs:

Now does this look like a solid company to you?