Digital banks are blossoming in many parts of the world. In Southeast Asia, competition is heating up as incumbent banks, fintech and diversified regional tech players are all vying to capture the digital-first customers.

This year, we have launched three reports as part of Momentum Works’s digital banks series: Rise of digital banks in Indonesia, Digital banks in Malaysia and Who is Nubank.

After reading the “Who is Nubank” report, many of you asked us – “this is interesting, is there more out there we can learn?”

Truth be told, there is a lot of materials out there – news articles, reports and interviews/videos – on digital bank experiences. But they come in bits and pieces – for those who are not familiar with the background of the globally leading digital-only banks, it can be hard to connect the dots.

Besides, many of the materials are focused on European and American digital banks, whose circumstances and regulatory environments are very different from what we face here in Southeast Asia.

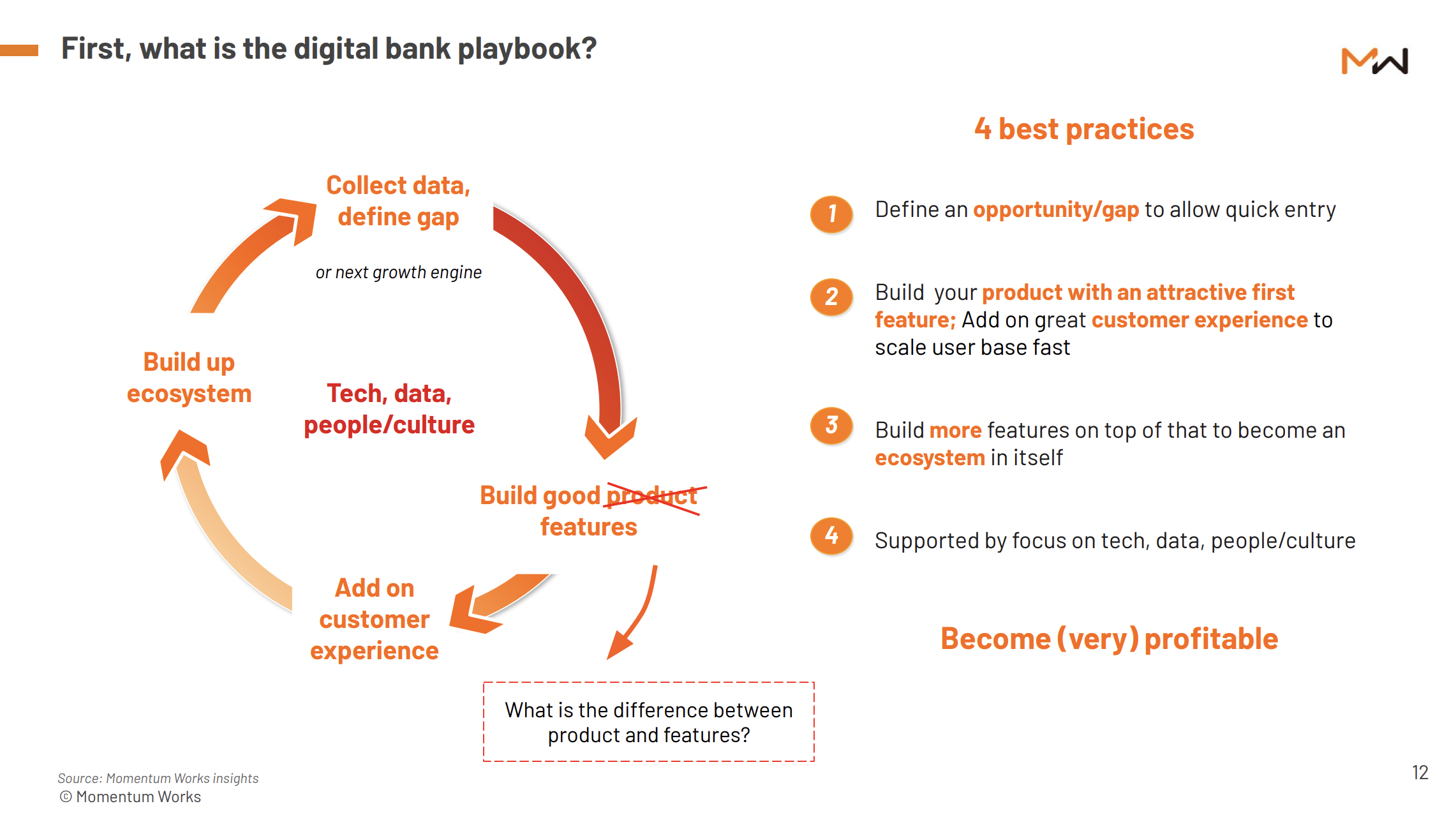

With the above in mind, we distilled our takes in the Decoding digital banks – best practices report, published today (26 October 2021). In this report we have highlighted 4 lessons from leading digital banks in Asia and large emerging markets: Russia’s Tinkoff, Brazil’s (soon to be global) Nubank, Mybank (by Ant Group), Webank (by Tencent) and Korea’s Kakao Bank.

These players are not traditional banks to begin with, but rather technology-focused startups or spin-offs of large tech ecosystems. Their overall strategy is very similar to what we see in successful large consumer tech players:

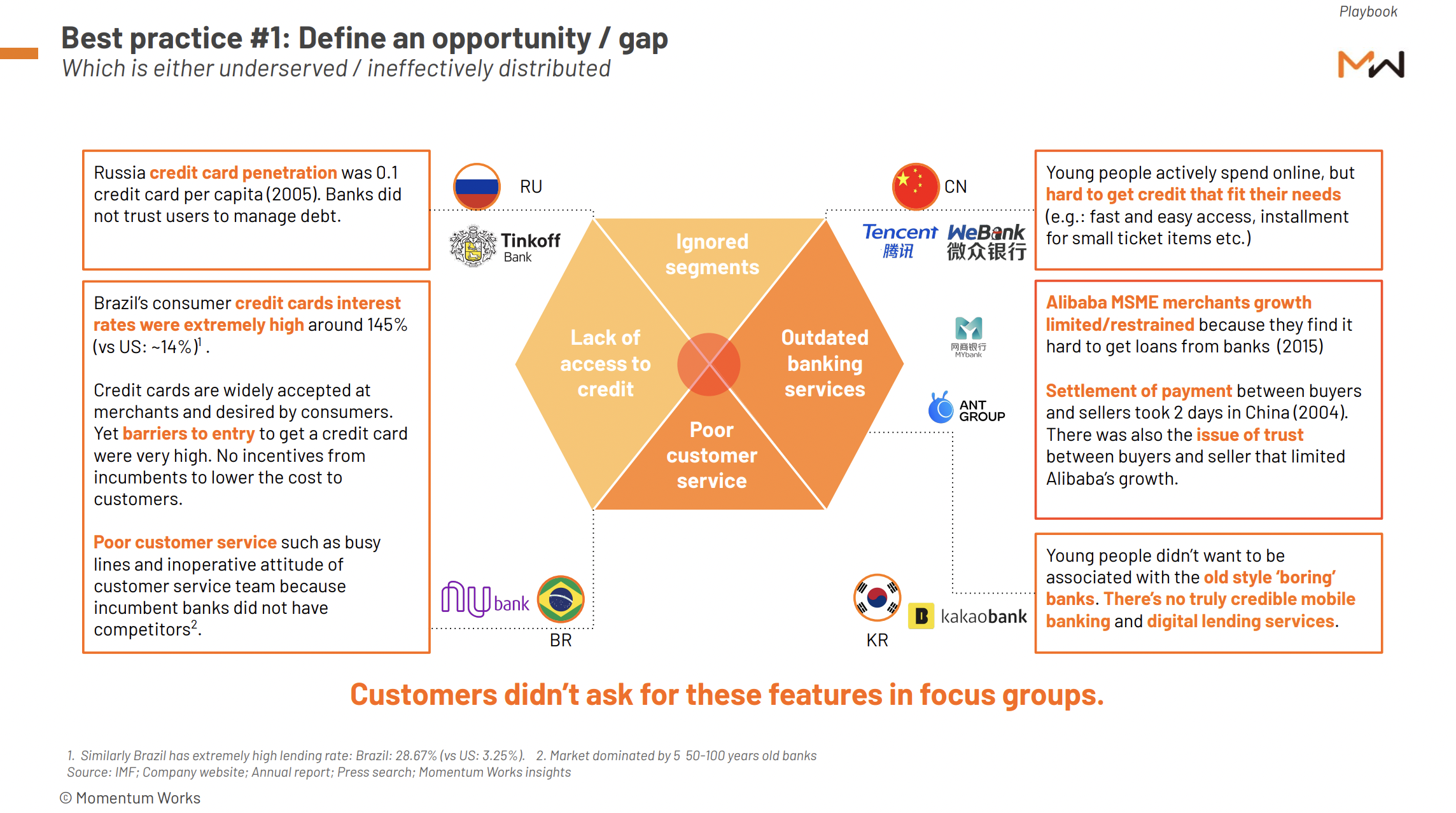

#1: Define an opportunity / gap

Leading digital banks make quick entries by serving underserved markets (e.g.: ignored segments with insufficient credit history) and / or by providing better product/services than incumbent banks.

Case in point, Nubank was able to leapfrog through digital bank innovation, riding on the extremely high credit card interest rates in Brazil (145% vs US’s 14%) and poor customer service of large incumbents.

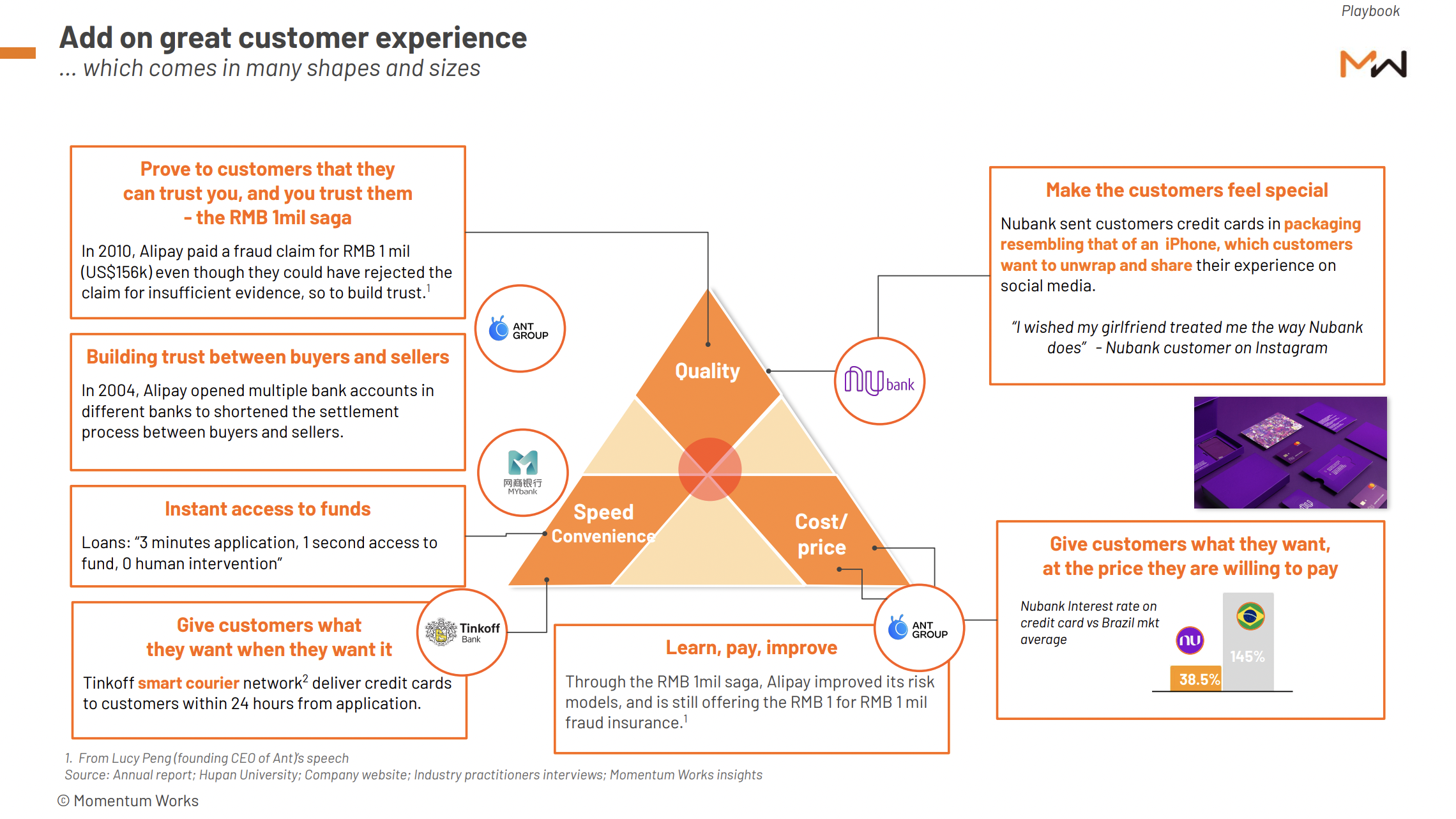

#2: Build first product with attractive (instead of perfect) first feature, add on great customer experience

Customer experience can come in the forms of quality, speed and savings. For example, Ant Group, Mybank’s major shareholder, provides instant access to funds: “ 3 minutes application, 1 second access to funds, 0 human intervention”.

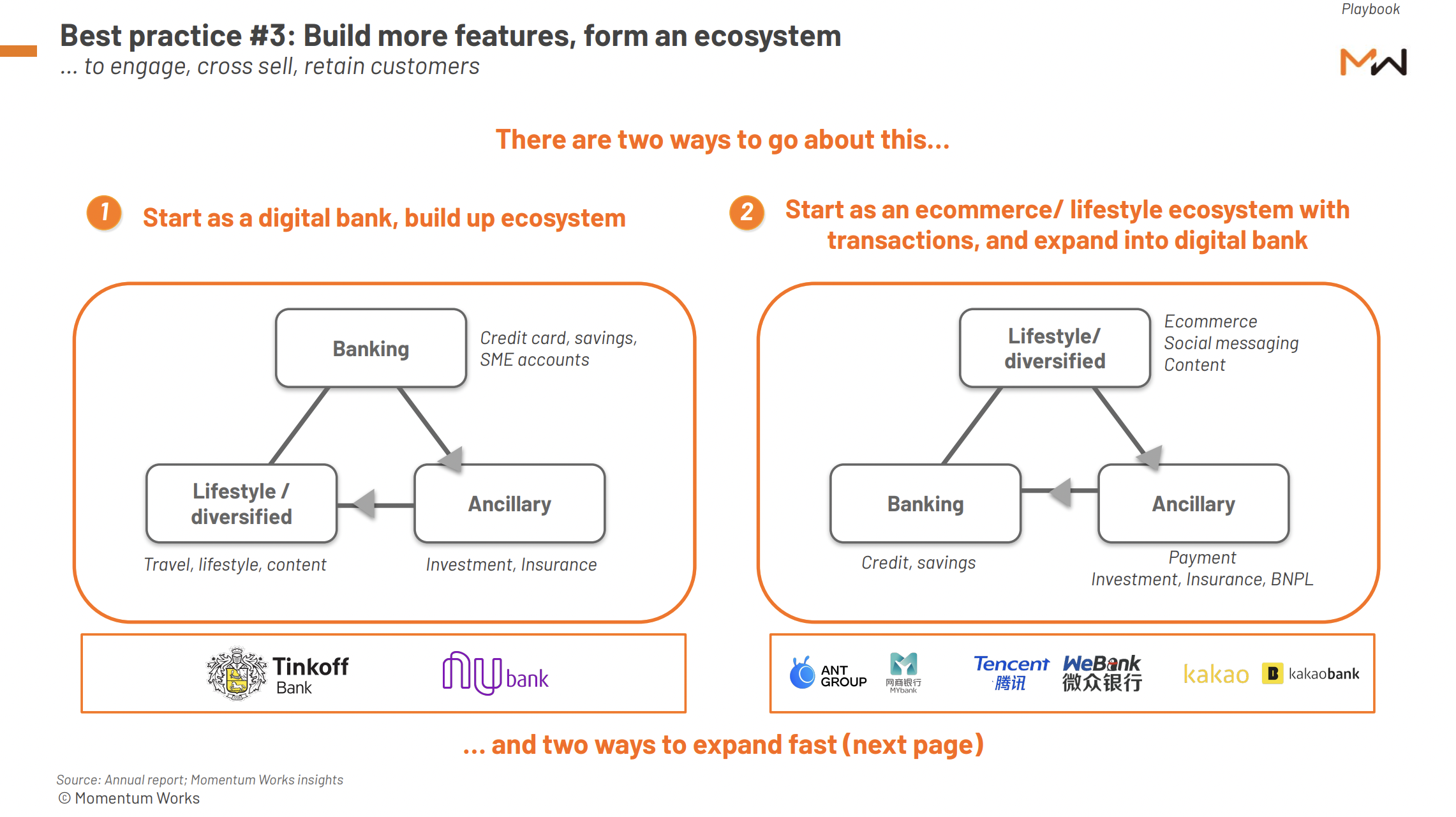

#3: Build more features on top to form an ecosystem in itself

Regardless of the starting point – either as a digital bank (e.g.: Tinkoff, Nubank), or as the banking subsidiary of a diversified tech player (e.g.: Mybank, Webank, Kakao Bank), we believe a digital bank has to form an ecosystem, a closed-loop customer retention cycle.

Here, there are two ways to expand (features) fast:

First, through strong partnerships (e.g.: Tinkoff).

Second, leverage on own / parent’s use cases (e.g.: Mybank with Ant group and Alibaba’s ecosystem).

#4: Support customer journey with focus on tech, data, people and culture

Data is often highlighted as the new oil, for many sectors including digital banks.

In more successful digital-only banks highlighted in the report, data is often not something that hundreds of PhDs and data scientists play with. Rather, they serve specific purposes including efficiency, risk control and customer targeting.

No rocket science, though the clarity of such purpose and the smooth execution are often what differentiates a better digital only bank than their mediocre peers, especially over the long term when effects of venture funding wear off.

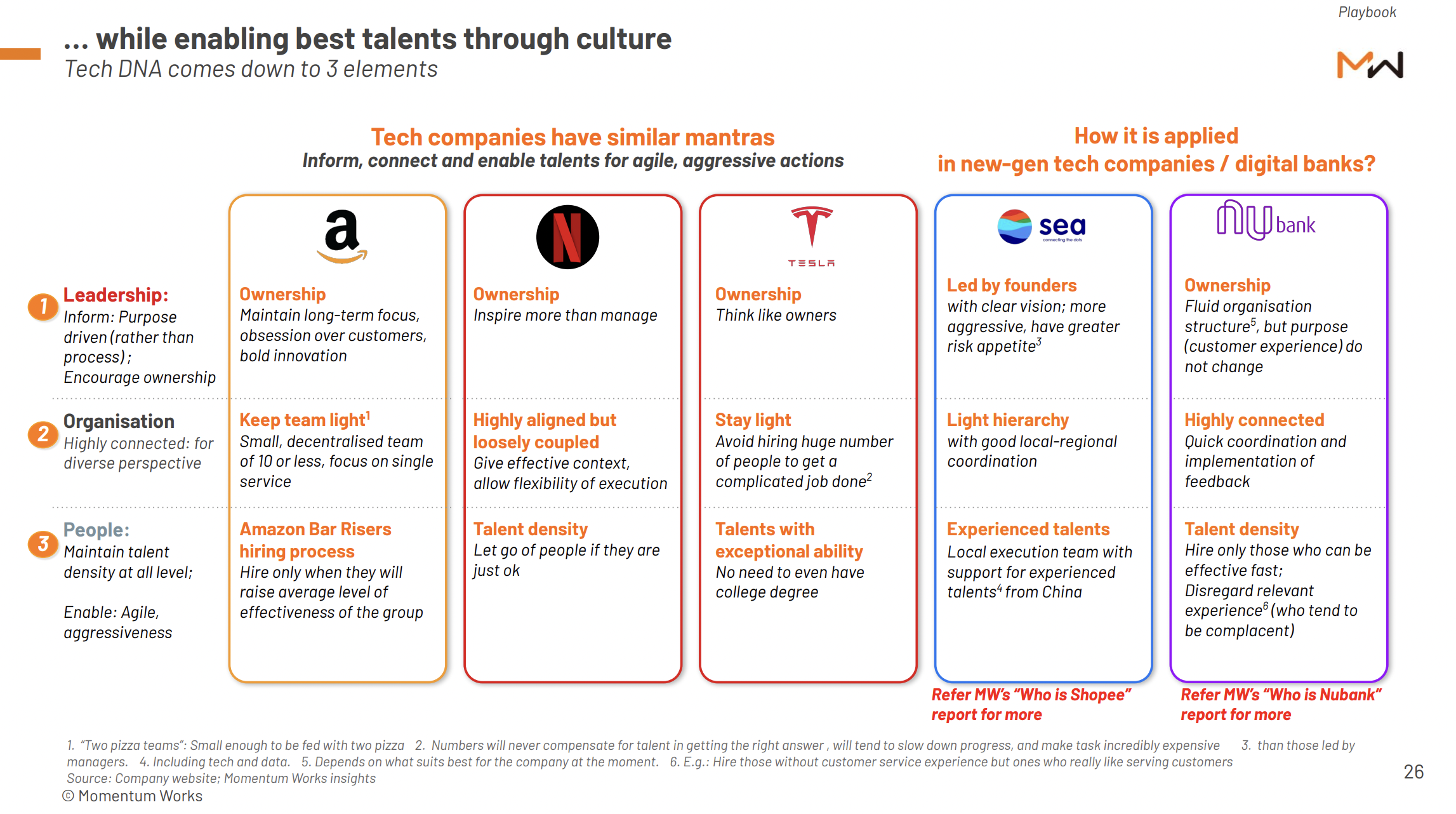

Many emerging tech companies / digital banks (e.g.: Nubank) have a culture that resembles large tech companies in their earlier days (e.g.: Amazon, Netflix).

Nubank took learnings from culture of Silicon Valley tech companies (and executed well)

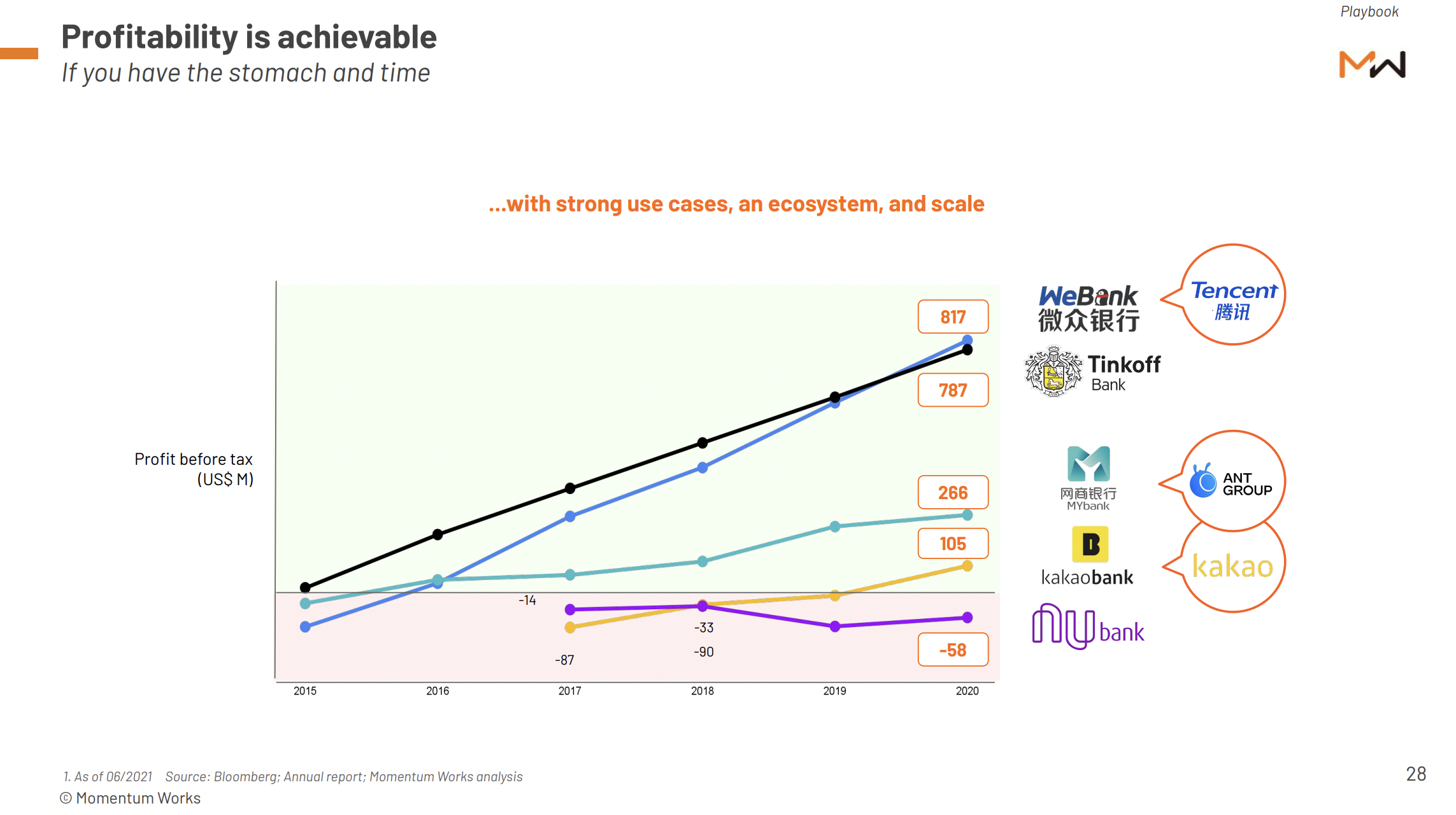

Ultimately, profit is achievable, with strong use cases, ecosystem and scale. Again, no rocket science here – just clarity of vision, good team, and great execution, which translate into customer experience, and shareholder value.

Conclusion

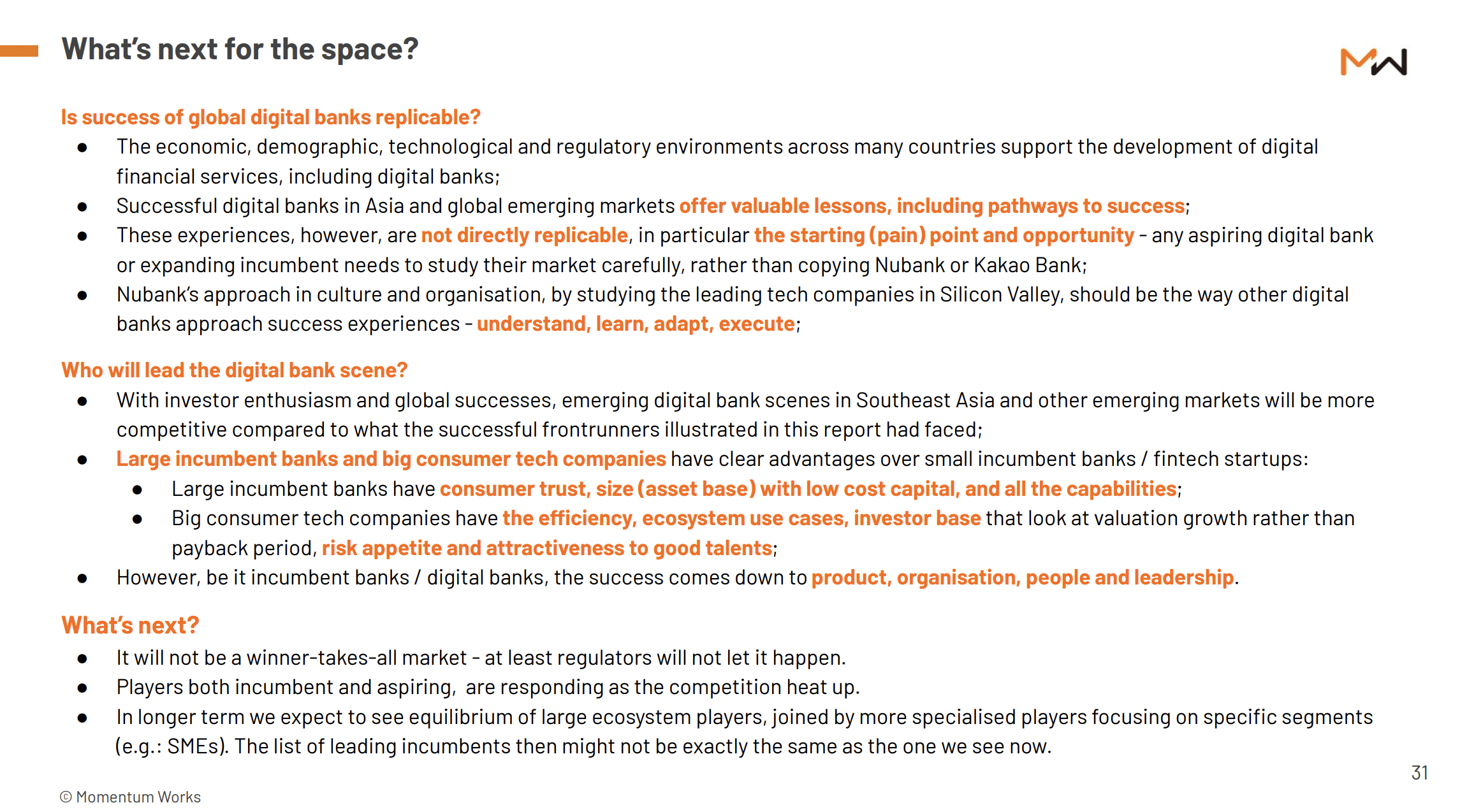

While we have seen efforts to exactly replicate Nubank or Tinkoff in part of Southeast Asia, we have to caution that the circumstances are very different and the exact experiences are not replicable.

Moving forward, large incumbent banks and big consumer tech companies will probably lead the digital bank scene in Southeast Asia, as they carry a lot of advantages a replica of Nubank will never have in this region.

Access the report

You can get the above and more from a copy of the Decoding digital banks – best practices report here.

Finally, we will be conducting a briefing to answer further questions you have. Subscribe to TheLowDown newsletter (link on the right) to get informed about the date and registration details once they become available.

As usual, we welcome burning questions, enquiries and sharing at [email protected].

See you at the briefing.