Many of you still remember the 2018 predictions that we made in December 2017. How right (or wrong) are we, now we are almost crossing the half year mark?

Here you go – to make it easier, we highlighted those we predicted accurately in green, those we got wrong in red, and those which are yet to be clear in blue.

Overall – not bad I would say.

1. Payday loan bubble bursts.

In February, we already heard from many investors that Indonesia payday loan market was not as good as they thought. Many Chinese players have already left, or have their operations frozen for violating local regulations.

We actually believe the market potential is still there (and huge). A telling sign is that after so much land grab, the customer acquisition cost for payday loan providers in Indonesia has not risen much, if at all. This tells you a lot about supply and demand.

The difficult part for every one is how to control the risk, through data modelling and credit scoring. This will probably be the main differentiator in the market for the next 6-12 months.

2. Uber throws in the towel in South East Asia.

Bingo! Told you so!

3. Ecommerce (and payment) continues to be fight of Chinese titans, with their local partners.

Just as the ecommerce battle seemed to have eased a little – between Alibaba-Lazada and Tencent-SEA-Shopee, JD decided to heat things up a little, by announcing its Thailand launch, slated for August 2018.

The market is still expecting Facebook and Amazon to step up its game but it probably won’t happen anytime soon. While Japanese/Singaporean-backed Carousell seem to be having significant traction, is still nowhere near being a titan.

Besides ecommerce, Chinese companies continue to dominate the payment landscape. Lazada, by launching its own wallet – quite possibly turning itself into a fintech player with the largest amount of users (all Lazada users have this wallet) in Southeast Asia. Other popular apps such as Airpay and BluePay – they too are Chinese-owned.

At least for now, the top spot for ecommerce (and payment) continues to be Chinese-dominated.

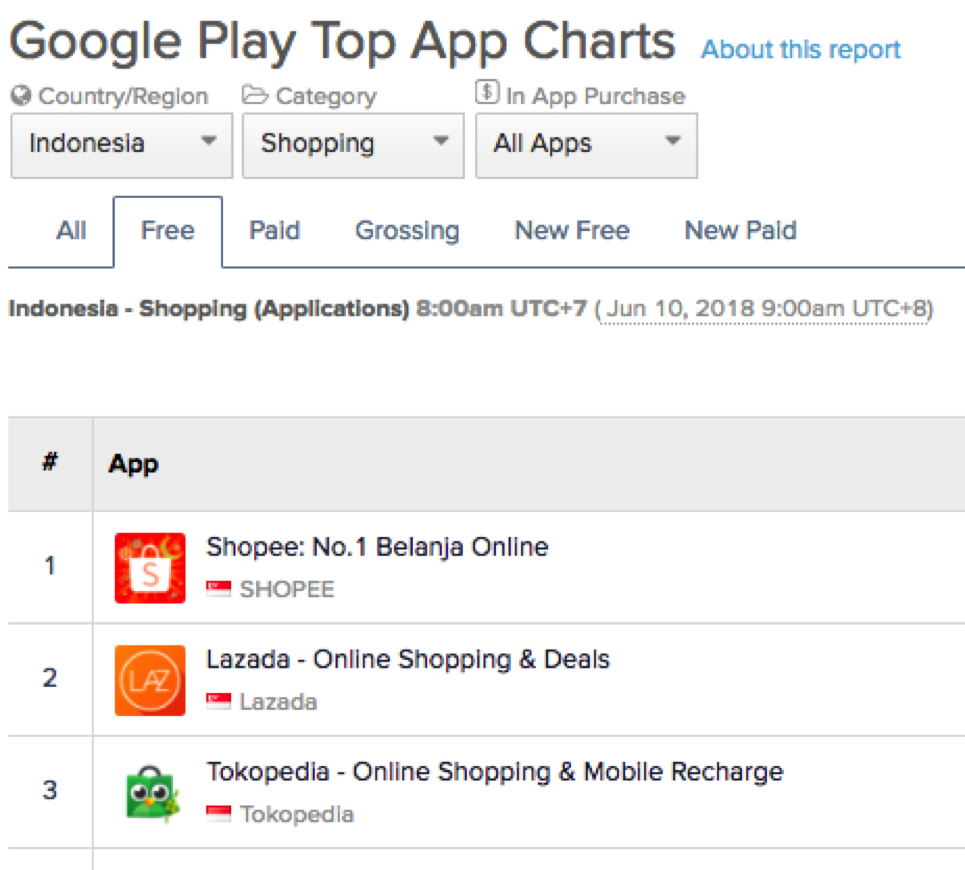

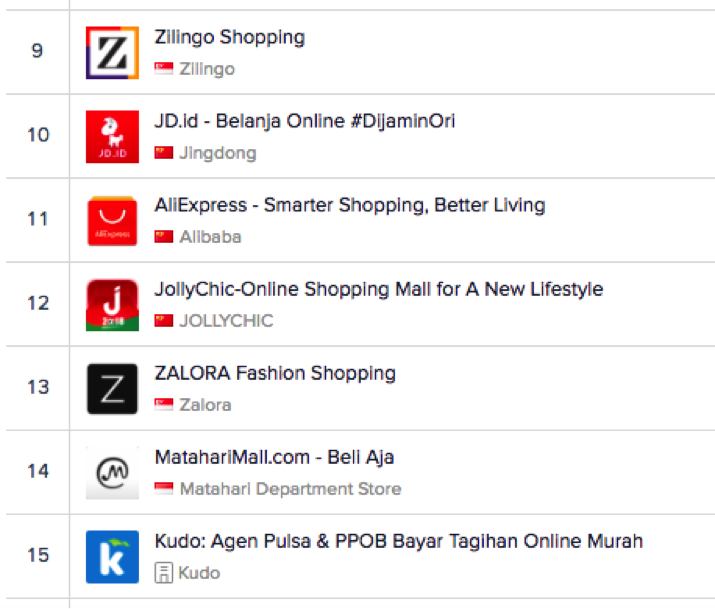

4. Chinese cross border e-commerce enter fierce competition

It is happening, though not as aggressively (yet) as we predicted. Among the top 15 Shopping apps in Indonesia’s Google Play Store, only Chinese crossborder players are AliExpress and JollyChic.

In Thailand, only SheIn made to top 10.

A deep dive with relevant stakeholders told us that many are still struggling with customs, COD (through third parties), and crucially, hiring the right local team. Ezbuy once had a strong local team – alas, poor cultural understanding, lack of trust, and inadequate management has caused an exodus with hardly anyone left.

5. GoPay will rapidly become the preferred payment method in Indonesia.

It seems regulatory forces are pulling GoPay back – a few launches have been delayed again and again. Nonetheless GoPay is still light years ahead of Grab.

Lippo’s relentless push of OVO is interesting to watch. Perhaps Indonesian payment landscape will never be as united as it is in China.

6. Vietnam and Philippines receive more attention.

This is happening indeed. Over the last three months especially, we have seen droves of investors heading to VN and PH. That said, in terms of actual investments, we believe it will still take some months at least.

7. Investors still struggle to find the next billion dollar opportunity.

Still the case – that’s why some of the subprime companies have been able to receive significant B & C rounds. There is so much money in this space and not enough good companies in that range to invest in.

That said, we believe in the prospects of Southeast Asia – it is more than 600 million people with stable economic growth and fast-spreading consumerism. It is only a matter of time that more unicorns are emerging – we actually believe this will happen very, very soon.

8. Corporate innovation goes to the tangibles – with bold moves

While 2018 has not seen any successful results from corporate innovation yet, we still believe that there is a chance for one.

An accelerated corporate innovation trend is expected as corporates start to realise that they are more likely to succeed through acquisitions or partnerships. They either set up a fund to acquire or a separate business to partner others with strong synergies. Singha, for example, has launched a $25m fund to invest in Series A rounds.

Grab started Grab ventures to allow them to enter opportunities quickly. JFDI, an accelerator in Singapore has switched its business model from accelerating startups to corporates. Capgemini set up an innovation lab recently.

9. Bitcoin reaches $100,000, and blockchains enter the mainstream.

We made this prediction based on the assumption that bitcoin will be quickly accepted as an asset class by global investors. This has not happened yet – the prices have been sluggish since February, as we continue watching this space.

However, a few notables. While companies that ICOs before February are not entering the death zone of having to deliver some product (as promised in the roadmap part of their white papers). Blockchain, on the other hand, is entering the mainstream, with some actually applications starting to be built.

It will take a few years to mature – a severe test of investors’ confidence. But then isn’t it the same for other sectors, such as VR, Big Data and ecommerce?

10. Deep tech remains elusive for the region.

Indeed – government-funded deep tech accelerators are still poaching people from local deep tech companies that are struggling to find people themselves. You also see that new batches of companies coming out of deep tech accelerators are not that ‘deep tech’.

On the other hand, big boys step up the talent grab, especially in Singapore. Life will be harder for standalone deep tech, especially AI, companies, in the region, we reckon.