On 18 April 2023, Momentum Academy was invited by Huawei Cloud to provide an immersive sharing on “Opportunities and growth potential in Southeast Asia” for Chinese decision-makers looking to expand their operations into this region.

Together with my colleague Liz, I delivered the sharing to the audience who were mainly founders, CEOs and other key decision makers of Huawei’s partnership ecosystem.

Some key takeaways from the event:

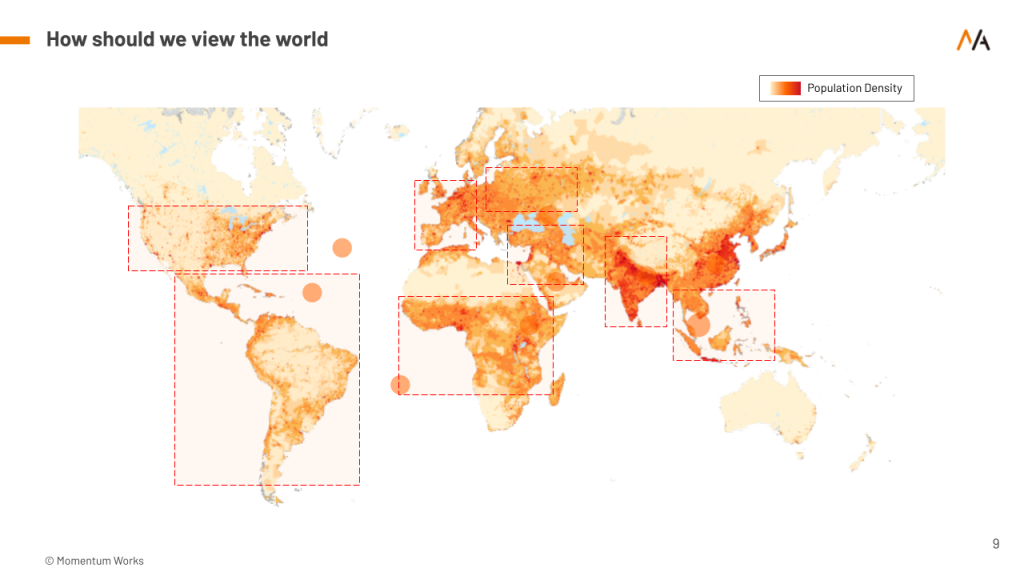

- Southeast Asia is a sizeable market, and competition is much less intense (less 卷) than in China.

Compared to Latin America, Southeast Asia’s geographical and cultural proximity to China make it the first target market for Chinese companies venturing overseas.

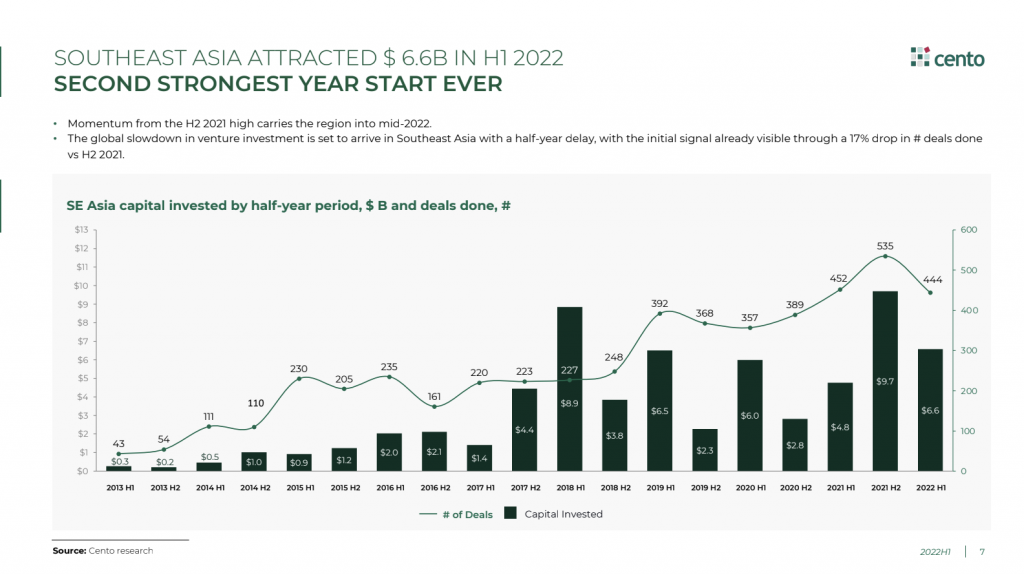

Case in point, Southeast Asia has gained more attention in recent years, attracting $6.6B tech investment in H1 2022, the second-strongest year start ever.

Sidenote: Our partner Cento Ventures is in the midst of finalising FY 2022 Tech Investment in Southeast Asia report. We will release the report in the coming days – stay tuned!

You can refer to the English and Chinese versions of the 2022 H1 report here.

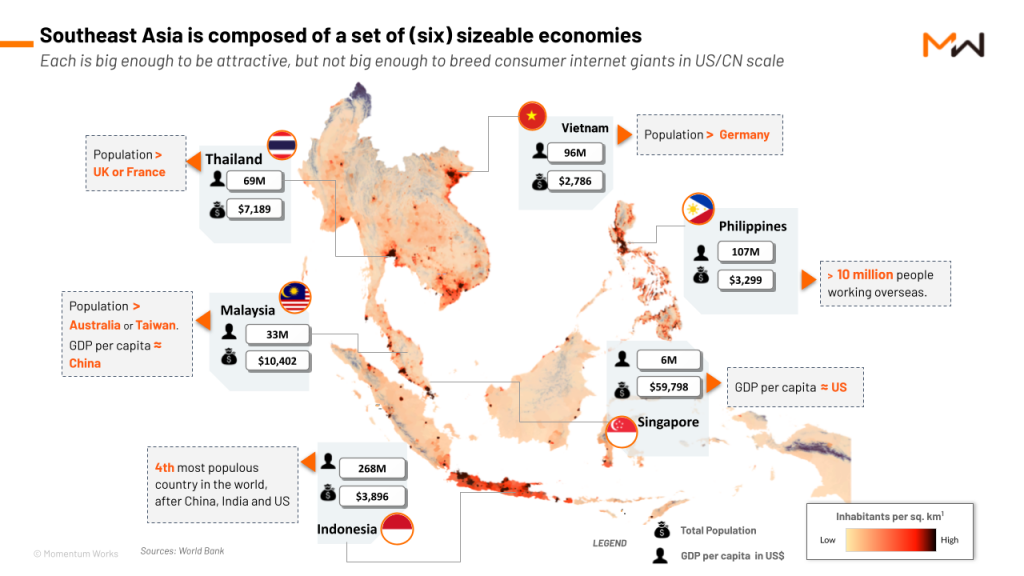

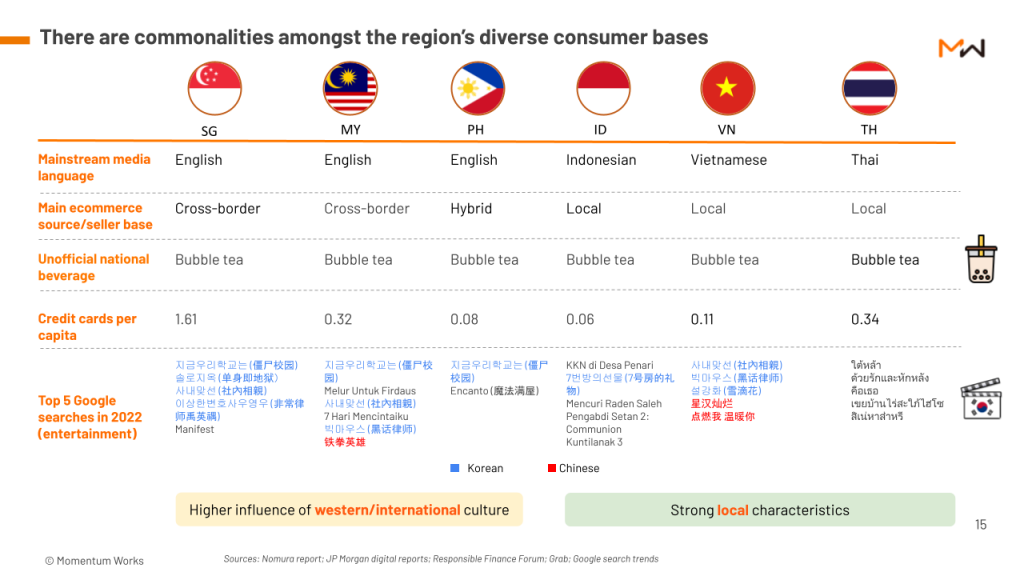

- Southeast Asia should not be seen as one single market

Six major countries in Southeast Asia have vast differences, in terms of population size, economic development, culture, and many others.

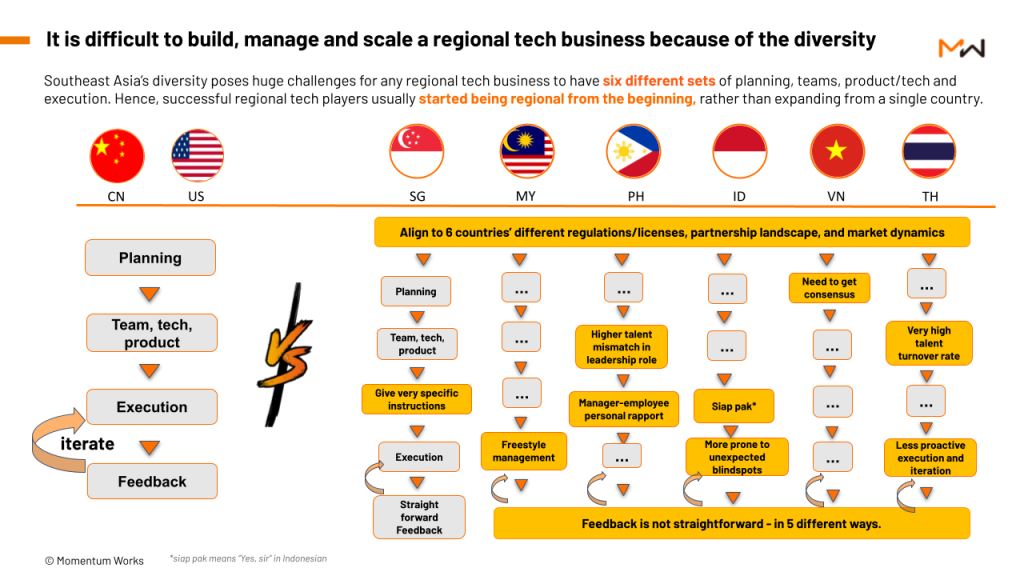

- Management in Southeast Asia needs to be differentiated and adapted to the local context – that means planning on people, organisation, product and leadership has to be repeated six times.

- The region’s diversity serves as natural barriers (or moat, for players who are able to navigate the region’s complexity).

For example, Singapore, Malaysia and the Philippines have a higher influence of western / international culture, whilst Indonesia, Vietnam and Thailand have strong local characteristics.

The love for Korean dramas and (more so) bubble tea however, are quite universal across the region.

- Product pricing and brand positioning need to be differentiated

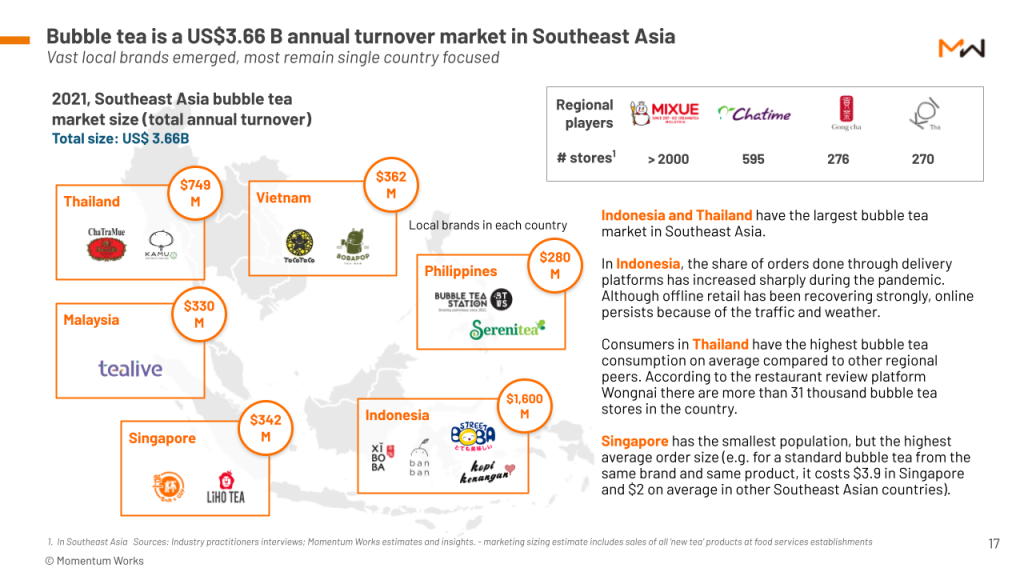

Bubble tea, the universal national drink in Southeast Asia, provides a good reflection on pricing strategies and brand positioning for companies expanding into Southeast Asia.

Bubble tea is a $3.7B market in Southeast Asia (access the report here)

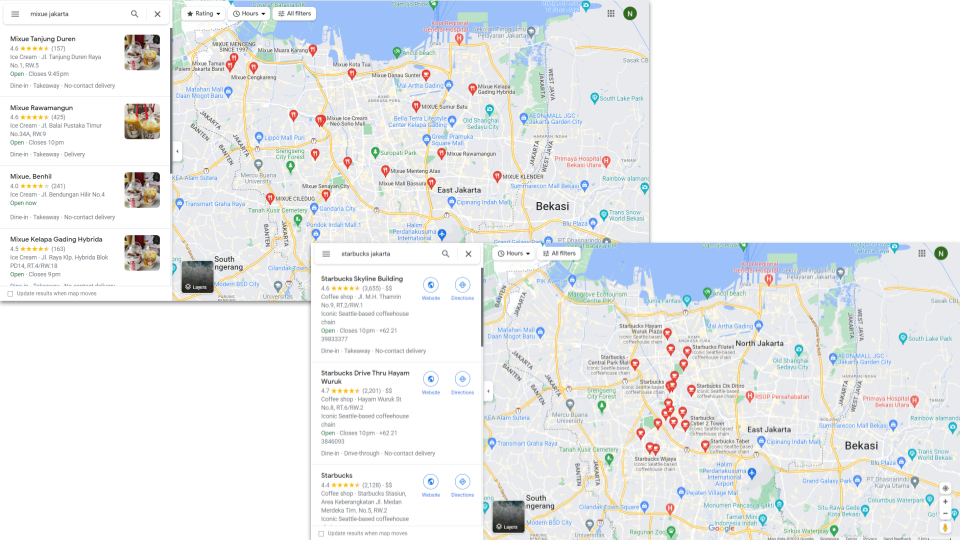

For example, Mixue, a mass market-focused ‘new tea’ brand started in China (< $2 / drink), expanded into Southeast Asia in 2018 by first entering lower average order value countries like Indonesia and Vietnam. Mixue now has > 2000 stores in Southeast Asia through a local franchise model.

Number of Mixue stores (left) vs Starbucks in Jakarta (right)

On the other hand, Heytea, which focuses on a more premium price-point (> $5 / drink) and expanded into Southeast Asia around the same time as Mixue in 2018, has kept its footprint only in Singapore, through a self-operated model.

Heytea in Marina Bay Sands, Singapore

Similarly in the coffee market, in China, Luckin Coffee priced itself lower than Starbucks, but in Singapore, it is priced around Starbucks’ price point because a low price will get them into unnecessary competition with low margins (e.g.: against hawker stalls).

Luckin’s price in SG & CN, benchmarked against Starbucks’

Luckin’s price in SG & CN, benchmarked against Starbucks’

- ‘Orgnisation’ will be a central (and evolving) challenge for all international companies

Almost all the large tech companies in China put “organisation” as a top agenda item (see Our thoughts on Alibaba’s major “1+6+N” restructuring).

However, when these companies adapt their successful organisational practices to overseas ventures, another set of challenges arises:

- What type of structures, rules, and processes are needed to navigate an organisation of 100,000 people with multiple departments and business units through a constantly changing international landscape?

- Should decisions come from the headquarters in China or the regional / local team?

- To what extent should autonomy be given to the local team? How about resources allocation?

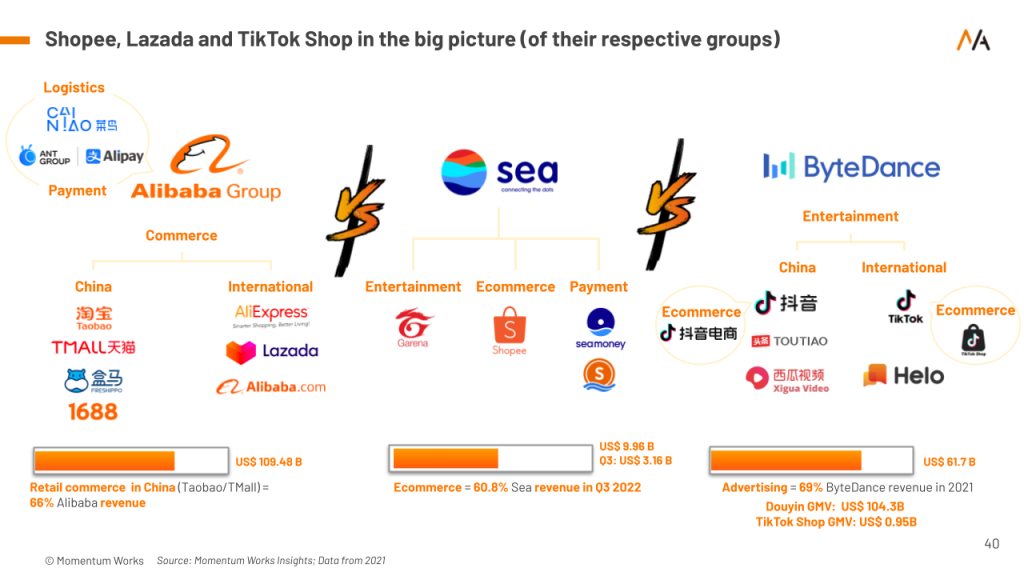

Some lessons can be taken from the way Lazada, Shopee and TikTok Shop are organised in Southeast Asia.

At their core: Lazada is a business unit, Shopee is the core of a group, and TikTok Shop is a department:

- Lazada is part of Alibaba and serves Alibaba’s overseas GMV and overseas user base;

- Shopee has to build ecommerce infrastructure in additional to GMV, in order to survive (e.g.: ShopeeXpress and ShopeePay);

- TikTok Shop is a department – its role is to monetise TikTok’s overseas’ traffic. In essence, Tiktok ecommerce will need to compete with internal departments such as advertising to meet TikTok’s KPIs for monetisation.

The resources, strategic focus and development pathway of a department, a business unit, and a conglomerate will be very different.

Conclusion

Ultimately, the ability to win the market (as a local / regional company) comes down to a few fundamental factors: Leadership, People, Organisation and Product, in that order.

You can get a deeper dive into this topic in Guoli Chen and Jianggan Li’s book Seeing the Unseen: Behind Chinese Tech Giants’ Global Venturing and Momentum Academy’s report Tech leaders with Chinese characteristics.

If you think our insights and community can benefit your organisation through talks, workshops and simulations, you are welcome to contact Momentum Academy at [email protected]