The competition will spill over outside China.

Last week, my colleague and I visited the Shanghai Auto Show, at the vast National Exhibition and Convention Center (Shanghai) – an important showcase of the current EV landscape in China.

Shanghai Auto Show is the most prominent showcase by car brands and manufacturers – and this year’s show attracted particular attention as people are trying to pick up signals of new trends as well as China’s consumption recovery. Not surprisingly, the key focus of the show this time is on EVs – with most of the 150 new models launched there purely electric.

As we also realised – the show also gives you a sense of how competitive the EV space in China is. It is a red ocean but it is also a sector where a lot of strategy, operational excellence and branding happen – offering rich business lessons.

Before landing in Shanghai, we were told by friends there that the biggest change in China’s largest city, now compared to before the pandemic, is the amount of electric cars on the street.

Indeed, we probably saw more “new energy” (electric, hybrid, hydrogen etc., but mainly electric) cars (light green plates) on the street than fossil fuel cars (blue plates). What we did not expect was the amount of EV brands: Arcfox, Voyah, Aion, Zeekr, Neta, Aito … in addition to the familiar names Tesla, BYD, Nio, Li Auto, and Xpeng.

What differentiates all these brands? What are the strategies? How will the competition play out? What are the lessons learnt? After visiting the Auto Show, we feel that there are some very interesting case studies and lessons on strategy, business operations, branding & PR, as well as sustainability here. Some of the thoughts:

- Almost every Chinese brand, independent or affiliate of larger automotive brands, raced to showcase new models, designs and concepts. In most cases, however, we really see little differentiation. Good designs get copied quickly, as in tech in China. The competition in that market segment is likely concentrated on price, and of course, efficiency.

- This is a difficult value proposition for many manufacturers as a significant percentage of the cost is batteries – where a few upstream players dominate. CATL, the largest EV battery manufacturer in the world, had an impressive showcase of its batteries and swapping stations. In this regard, Tesla is building a moat by producing its own batteries.

- Tesla is absent from this year’s Show. Perhaps it is related to the consumer protests at Tesla stand during the previous show in 2021; perhaps the company just did not think the show would be as worthy especially when it just announced plans to build a new battery factory in Shanghai. A technologist we spoke to thinks Tesla can probably reach the extreme production efficiency of one car out of production line every 10 seconds very soon.

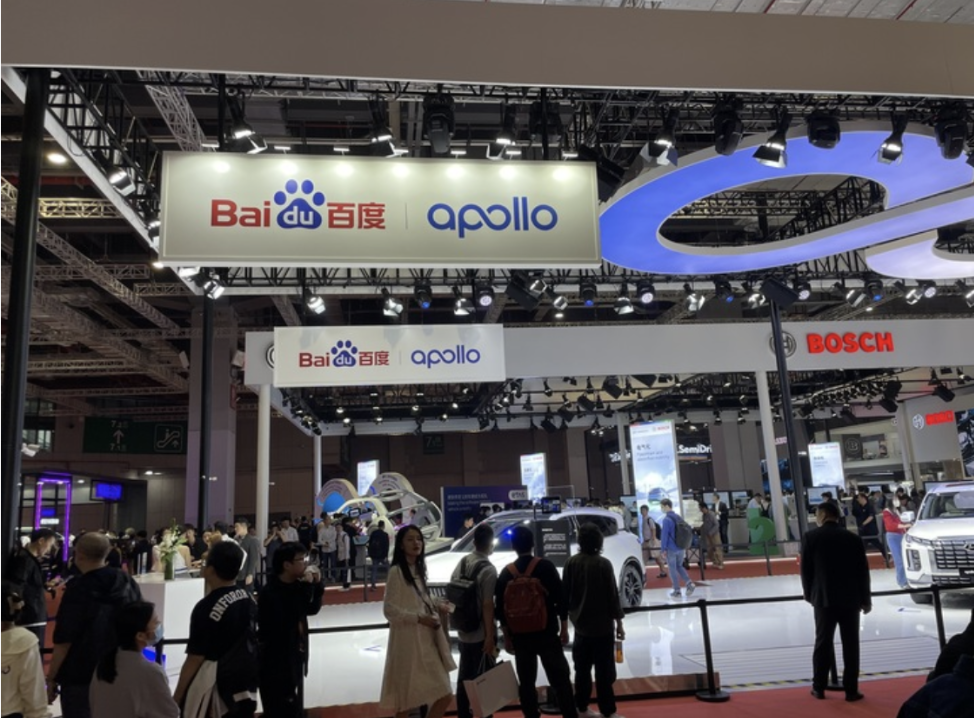

- Baidu, which went ‘all in’ AI with its Apollo autonomous driving system, only had a tiny stand with three Hyundai cars. We were told by industry experts that a few EV companies’ own autonomous driving systems were already on par with if not better than Apollo. Besides, Baidu as an AI company is probably very focused on its Ernie Bot large language model now.

- According to a Financial Times article on Shanghai auto show, international brands are slow to launch/customise new EV models in China because of the coordination/approval needed from headquarters. Indeed we saw very few new models being revealed by international brands. Chinese manufacturers are much more nimble, fast and aggressive. The competitive situation here probably has some resemblance to the “war of a thousand group buy companies” back in 2010 – check out Momentum Academy’s case study on Meituan to find out more about the competition and why Meituan won.

- BMW ran into a PR crisis during the show probably also because of its long decision chain. Promoters at MINI (a BMW owned brand) booth told Chinese visitors that they had run out of free ice cream but later offered ice cream to a few Europeans, which is a big taboo in China. What was worse was BMW’s PR response to the incident – it had been slow and out of sync with the media sentiment. Some PR experts told us that it was probably because they needed headquarters approval for the response. This incident may be an example of when leadership faces the significant task of balancing the mental demands associated with managing home markets while tackling the complexities of foreign ones. This is common and discussed using multiple case studies in the book I’ve authored Seeing the unseen: behind Chinese tech giants’ global venturing.

- Polestar, an EV affiliate of Volvo, showcased its new model Polestar4 amid 80,000 tulips. The person who came up with this grand concept is probably not Chinese. (hint: when do Chinese put a lot of flowers surrounding something?) Again – it could be the same issue that BMW faced, but with a funnier twist. Comprehending and adapting to the cultural nuances of target markets is essential (but very challenging) for the successful integration and acceptance by local staff and consumers.

- As competition continues and margins are thin in the domestic market – a few Chinese EV players have been eying global markets. BYD, GreatWall and Wuling are pioneers in this undertaking. More will come even though very few will succeed. Any company that is thinking of expanding to a new market must also determine the appropriate allocation of resources between exploring new markets and fostering growth in their core business at home.

- Also, while so many countries talk about EV adoption, which ones will be able to force the adoption using policy tools (including subsidies) as effectively as municipal governments in China have exercised? That assessment will impact business strategy as well as expectations of the whole EV value chain.

- Amongst ‘new force tiro’ (Nio, Li Auto & Xpeng) of automotive startups, Li Auto seems to be in the best position (in sales numbers) while Xpeng’s sliding sales numbers are worrying many. There are rumours of a potential Xiaomi acquisition of XPeng. Experts we spoke to point out that while XPeng has breakthroughs in many technologies, its positioning (of mass premium) leaves it in an awkward position of both low margin and low volume.

- Will BYD’s Denza D9, whose monthly sales has surpassed 10,000 units, be a worthwhile challenger of Toyoto Alphard in luxury MPV?

During the same week, we also had long discussions with a few key stakeholders in the sector: investors, executives, as well as technologists. Some of the discussions went into great details in industrial design and manufacturing processes.

While these stakeholders are divided on how exactly the competition between BYD, Tesla and the “new force trio” (Nio, Li Auto & Xpeng) will play out, one thing everyone does agree is: at the lower-priced mass segment of EV market, it is a dog fight and probably very few brands will survive profitably – just like any other industry in the highly competitive Chinese market.

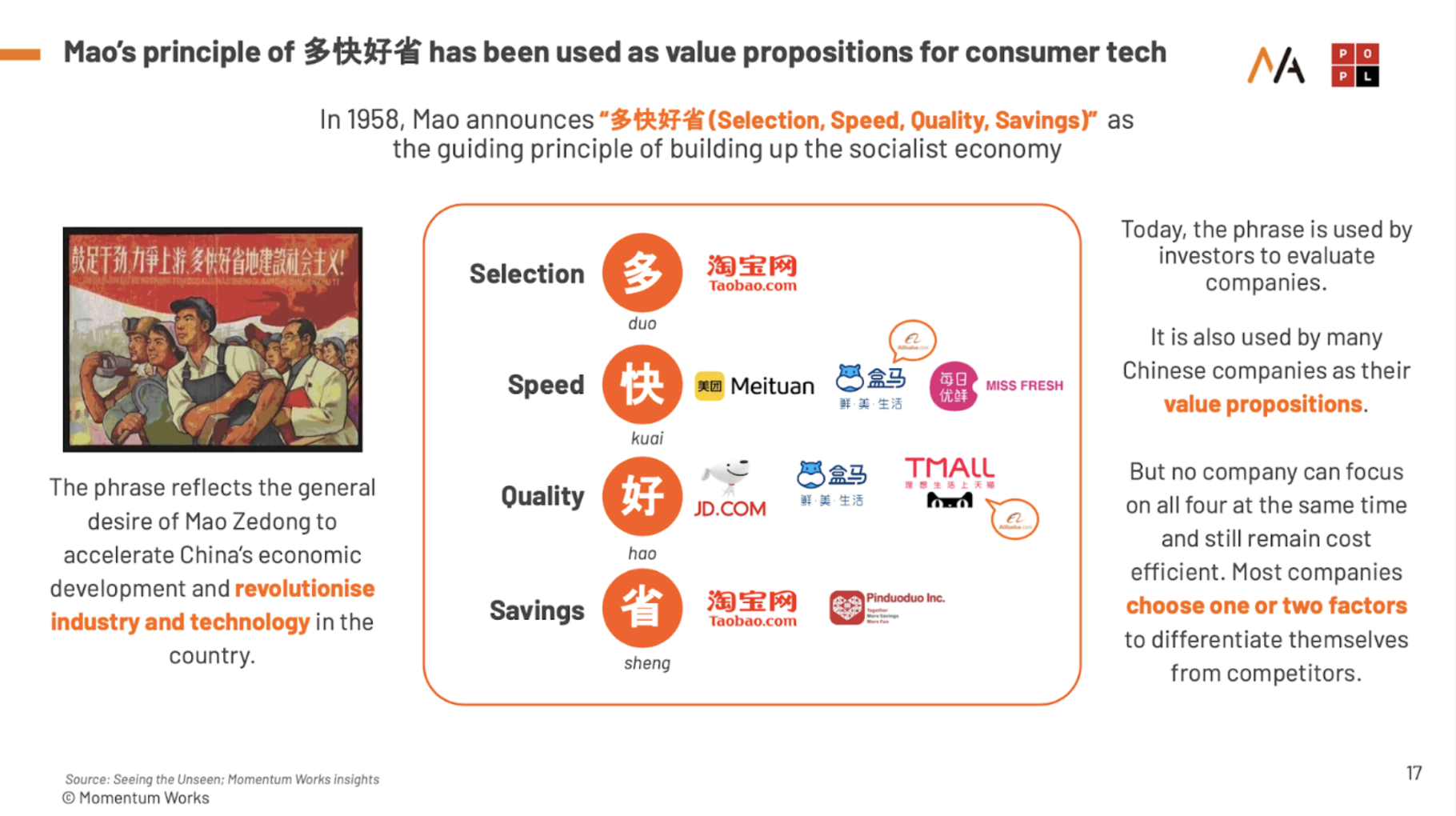

The strategy and value proposition, at the end of the day, will mimic that of the internet companies: a combination of Selection, Speed, Quality and Savings. Companies will need to use at least one of these to penetrate through the market, while building a sustained moat will require doing really consistently well in two or three of these:

As the competition offers us valuable lessons, and will probably spillover to impact many of us, Momentum Works and Momentum Academy team will continue to follow this space closely, rolling out insights, and immersion/simulation products along the way. Tune in!

By the way, my favourite car of the whole show: