New targets for 2019 are said to include the Philippines, Malaysia, Myanmar and Cambodia.

However, expanding into new markets won’t be easy. We believe that Go-Jek will take it slow. Think marathon, not 100 meter dash.

Here are the challenges:

- Well funded incumbent. Grab has been operating in eight markets in Southeast Asia for a long time and they have enough green ammunition. Will the two companies start a fierce price war like the Uber era? And, even if you play a price war, can Go-Jek catch up? If they have learnt anything from Uber’s (or even Meituan’s) experience in China, they would be wary of the fact that it is pretty hard to catch up with a rich incumbent through burning money.

- SEA markets are distinctly different from one another. Each market has unique characteristics and with Indonesia strong in Go-Jek’s DNA, adapting to other markets won’t be easy. This is unlike Grab, which grew almost organically across all markets before it became big. Go-Jek is currently trying to give their local management greater autonomy. Additionally, unlike Grab, which has the same app across all SEA markets, Go-Jek believes in heavily localising their products. For example, it is named Go-Viet in Vietnam and GET in Thailand. This is an interesting strategy. However, whether it can perform well under various shareholder interests and competitive pressures remains to be seen.

- Product market fit. Go-Jek has a very comprehensive product line in Indonesia, which comes with its own complexities. How will it adapt to new markets quickly and effectively at the product level is also a challenge the team with have to tackle. Prioritisation will be a key concern.

- Payment. This will be discussed again below. We believe that the payment market will still be heavily contested in Southeast Asia, without a clear winner to emerge in 2019. How will the Go-Jek story play out in this epic?

Of course these challenges are not insurmountable but it will be interesting to see how Go-Jek moves ahead. All these factors put together, be prepared for a slow traction in 2019.

-

Payment remains fragmented, with central banks exercising more control over settlement

Payments will continue to be a fragmented landscape with banks, conglomerates, telcos all sitting on a treasure trove of data and unwilling to give up their lucrative share of the pie.

In Indonesia, the landscape has been constantly evolving with Lippo Group’s OVO (which works with Grab), and Ant Financial + Emtek’s Dana gaining recent traction in a short time via aggressive marketing.

Mandiri, Telkomsel etc. have a strong hold via their e-wallets. Go-Jek’s GoPay too is popular because of a strong use case.

However, things became interesting with Grab and Tokopedia joining hands with OVO, Bukalapak with Dana, and JD.id with GoPay.

Part of the reason why so many startups partnered with existing payment players is because of uncertain and stringent license regulations. Indonesia’s central bank – Bank Indonesia (BI)- had put in place an effective moratorium of payment licence issuance.

However, do note that BI recently issued an e-wallet license to a payment company from China namely, Bluepay. This fuels speculations that the moratorium will soon be lifted.

That said, in China before Alipay became dominant, various telcos and other companies had tried to build their own payment as well. Though what has played out in China has served a warning to many players in the region of what to do and critically what not to do. Payment landscape in 2019 will continue to remain fragmented.

Some other markets in Southeast Asia are similar with central banks being quite active in retaining control. Singapore has already bashed third-party payment apps through a unified QR code, and has recovered a lot of lost ground (which may not have been lost) for the banks. Thailand’s PromptPay is not as quick as Singapore’s initiative but it is expected to draw a lot from Singapore’s experience.

-

Ecommerce giants, including Tokopedia, move more aggressively offline for growth

The future of online ecommerce is…offline.

The fact that most ecommerce markets in SEA have captured only less than 4% of total retail underscores that the potential for growth is staggering.

E-retailers across SEA have been seeing a saturation in online marketing channels, infrastructure bottlenecks, and fierce competition for a limited pool of digital consumers (only about half the population has access to internet in SEA’s largest economy). All these contribute to a (fast) growth ceiling. To forge ahead quickly, they will push for more aggressive offline.

In Indonesia for example, Tokopedia is expecting to use a large portion of the $1.1 billion that it recently acquired from Softbank and Alibaba to pursue new retail – whatever that means. Bukalapak too has signed up more than 300,000 neighbourhood kiosks as partners. They will continue these efforts to tap into > 90% of the retail market that’s still outside the ecommerce platform.

Elsewhere too, retailers are realising that strategic brick-and-mortar stores and other offline channels are a necessity to scale operations across the region.

-

More money in revamping the region’s logistics network

Logistics in Southeast Asia has only started to accelerate in recent years and with the rise of ecommerce, the pain points are becoming obvious leaving a large room for improvement.

With the opportunity ripe and lucrative, it is not difficult to predict that many players will continue to eye the Southeast Asian market in the near future.

Alibaba has been making inroads into the logistics sector in the region by investing in various markets. It’s first logistics hub was in Kuala Lumpur; It has invested in SingPost; It expects to complete the construction of an ecommerce and logistics hub in Thailand by 2019. It will continue to build a global logistics network by strengthening its presence in SEA over the coming year.

In the past year, JD.com has also increased its investment in logistics in Southeast Asia:

J&T Express’s achievements in Indonesia have been widely known and in 2018 J&T also expanded to many places outside Indonesia.

Ecommerce delivery is only a small part of the overall logistics market, with a lot of opportunities untapped and inefficiencies unresolved. We see more capital and startups moving into the field next year.

-

Chinese cross-border ecommerce competition intensifies

The cross border ecommerce market in Southeast Asia still has significant challenges. To put things into perspective, the combined orders to this region for cross border sellers add up to a tiny percentage of what they would do on Amazon alone.

In the past year, giants such as Shopee and Lazada have been doing well in educating the market. Complicated customs clearance has become more transparent and the regulations have become more comprehensible. Customs clearance agents have also improved in professionalism and maturity.

This is also the same forecast we made for 2018 at the end of 2017. However, infrastructure challenges such as as payments, language, and localisation made development in this sector slower than we had predicted.

However, with the continued saturation of European and American markets and external factors (including a series of restrictions imposed by Amazon’s most recent sellers in 2018), more cross border sellers will focus their attention on Southeast Asia instead.

Let’s not forget Southeast Asia is collectively richer than India and much bigger than Saudi Arabia, both seeing great Chinese cross border incursion in 2018.

-

Fintech still growing – survival of the fittest, not the fastest

We predicted the payday loan bubble in Southeast Asia would burst in 2018. Many outside companies are just here to make quick profits – nonetheless the potential of fintech in this region is evident: In Indonesia for example, research has shown that there is a $73 billion loan gap and by end of 2018, an estimated meagre amount of $1.3 billion would have been covered by lending enabled by fintech.

This means 98% still remains unfulfilled. It’s easy to see why so many foreign players are salivating at the prospects.

However, regulators have been cracking their whips which saw a number of businesses stripped of their registration. 404 illegal P2P lenders have been identified between January to October 2018. Regulators have also been paying heed to the outcry of thousands of customers who complained against aggressive debt practices.

However, this does not mean that the doors are closed for Indonesia’s P2P lending industry. On the contrary, strict supervision is conducive to a healthy development of the industry. Those who plan to stay in the game for a long time don’t want the market disrupted by reckless players.

2019 will be that year when the fittest, not the fastest will survive. It is not enough to move fast, play aggressive, and make quick money. On the contrary, players need to build their core risk control capabilities while adapt to the ever-changing regulatory environment.

We think many of the current top players will fall on the way forward in 2019.

-

Many AI and robo-advisory startups in Singapore fail, and the country finds a better niche

In order to find new economic growth areas, Singapore launched the National Artificial Intelligence Program in 2017, and major universities have set up research centers with AI-related scholarships. Bolstered by the government’s heavy investments in grants for AI, Singapore has seen myriads of AI and robo-advisory startups mushroom over the last few years.

Many startups have received initial rounds of investments, but they have not been able to convert it into into productive tangible outcomes, and the market outlook cannot support further growth.

In this regard, the Singapore government is actually very self-aware. After all, Singapore’s core competitiveness is not scale (the core of many AI fields is the size of data engineers and data), but to continue to lead in the fields of systems and environment.

It is expected that in 2019 Singapore will find a more suitable niche for local startups, but this will not be AI.

-

VCs with different country backgrounds are finally effectively talking to each other; and nobody talks about Series B crunch anymore

VCs (or other investors investing in the same space) from the US, Japan, and China all share a keen interest in the Southeast Asia’s tech market and growing consumption. However, despite meeting up and taking part in various common forums and platforms, their interactions haven’t been all that in-depth. Oftentimes they get together but information is not effectively communicated between the various groups.

We see things changing in 2019 with more in-depth exchanges between investors from different backgrounds. With the capital environment become colder in other regions, Southeast Asia will become a warm melting pot due to the inflow and integration of diverse capital.

-

FA for VC investments as an industry gains traction

In the past few years, there weren’t that many good startups in the region. Oftentimes as an investor you just need to do a round of the region’s capitals to meet all the potential investment targets.

But now the situation has changed. Some unicorn executives have decided to start their own businesses. And the obvious opportunities have been taken – VCs have to spend more time judging startups from unfamiliar fields.

Also, as mentioned above, the presence of VCs from different backgrounds makes scanning the market and decision making more challenging.

Therefore, the time is ripe for the development of an intermediary (financial advisory – or FA) industry. Although there are already many FAs active in the region, very few can really help solve the issue of information asymmetry and assist in making judgment calls.

In 2019 we believe that some good boutique FAs will start emerging in this area.

-

E-scooter fails to take off in the region

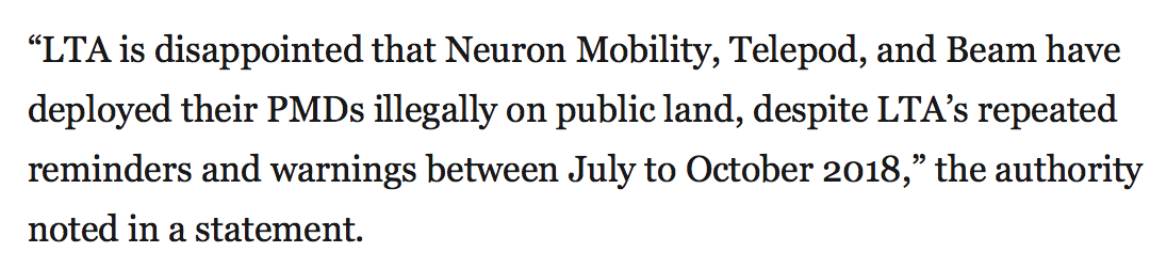

E-scooters have begun ramping up their presence in Southeast Asia. Uber-backed Lime has launched a pilot fleet of scooters in Singapore. Neuron Mobility, present in Singapore, snagged $3.7M to expand to other SEA cities such as Bangkok and Chiang Mai. Beam, a Singapore based startup, raised $6.4 million in seed funding to launch e-scooters in Singapore and Asia. However, the development of this industry won’t be smooth in 2019.

Singapore may be the most conducive market for e-scooters in Southeast Asia, but Singapore’s Land and Transport Authority (LTA) has been quite strict on enforcement, armed with its experience regulating the bike sharing industry.

These impoundings were as results of scooters being found outside permitted areas:

The strict licensing imposes limitations on maximum fleet size and wants operators to enforce responsible parking practices. Operators can be fined huge sums of money for violation. We saw how that turned out for Ofo.

As a result, Neuron mobility had to downsize its fleet and is now awaiting change in regulations which will take a few more months.

While this has slowed down the development of such startups in Singapore, we don’t expect things to be rosy in other markets either. With cheaper alternatives like motorbike taxis available in emerging markets like Indonesia and Vietnam, is there even a demand that e-scooter needs to fulfil?

More viable markets for the e-scooter companies? Australia and New Zealand.

——————-

These opinions are based on our long-term observation and practice in the local markets. If you have different opinions, please leave a comment or write to us at [email protected].

Preview: The next few days will be the 2019 forecast for the Middle East, India, Latin America and other regions, so stay tuned.

Momentum Works Emerging Markets Tech Investment Index

Momentum Works has released the Emerging Markets Tech Investment Index for various emerging markets. The image below is an example that shows the projected time between the different stages and the valuations you can expect at each stage:

We also launched Indonesia Fintech 2018 report and Indonesia ecommerce 2018 reports that comprehensively and systematically analyse opportunities, risks and investment opportunities in the respective sectors.

We also launched Indonesia Fintech 2018 report and Indonesia ecommerce 2018 reports that comprehensively and systematically analyse opportunities, risks and investment opportunities in the respective sectors.

If you are interested, please write to us at [email protected] with your name + email + company + position to get more details about the report.