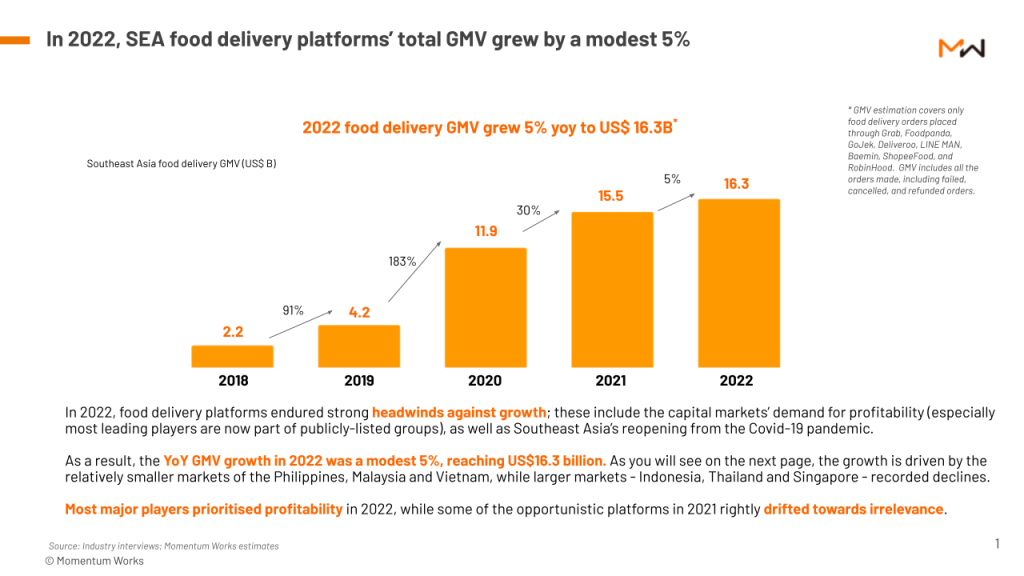

Modest growth, changing market dynamics.

When Momentum Works released our first Food Delivery Platforms in Southeast Asia report in January 2021, the whole of Southeast Asia was in the middle of covid. Offline dining was disrupted, if not banned altogether.

As a result, food delivery platforms GMV in 2020 almost tripled, and the growth sustained into 2021, as we indicated in our second Food Delivery Platforms in Southeast Asia report released in January 2022. A lot has happened in the ecosystem since then. Today we are unveiling Momentum Works’s 3rd annual Food Delivery Platforms in Southeast Asia report.

The report examines key trends, competitive dynamics as well as the platforms’ focus on path to profitability. You can download your copy here.

Here are some highlights of the report.

- Total food delivery platform GMV in Southeast Asia grew at a modest 5% year on year, reaching US$16.3 billion

This is against the strong headwinds the whole sector faced in 2022, including the capital markets’ demand for profitability, as well as Southeast Asia’s reopening from the pandemic.

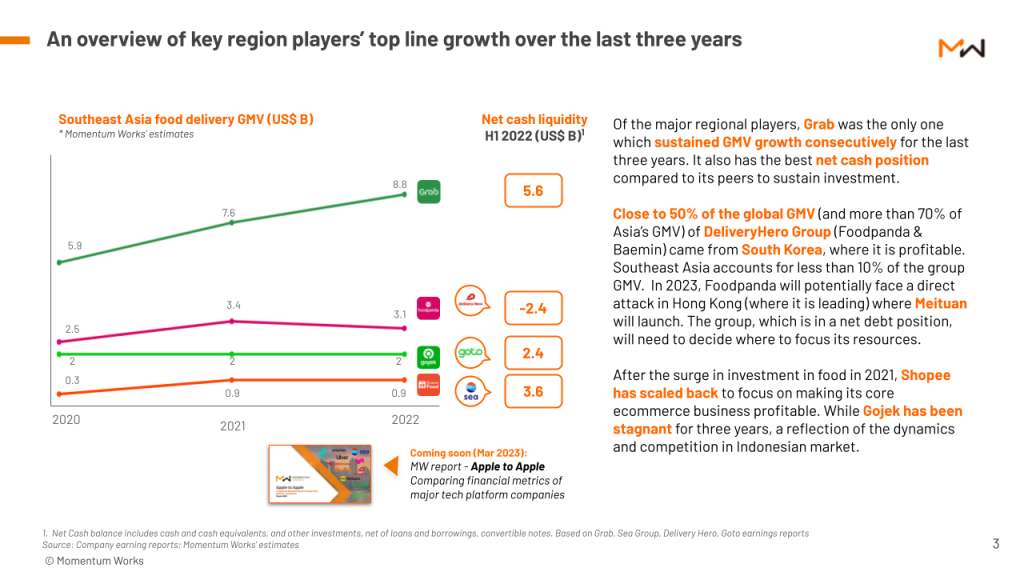

- Smaller markets grew while larger ones contracted; Grab extended market share leadership

Indonesia, Singapore and Thailand, the three largest food delivery markets in Southeast Asia, recorded GMV declines in 2022 – due to factors including reopening, withdrawal of government subsidies as well as platforms’ growth activities.

Smaller markets, including Malaysia, the Philippines and Vietnam, showed significant uptick, pushing the whole region still into the growth zone.

- In the tough capital environment, cash is king

In the last three years, Grab is the only regional player that has registered continuous GMV growth year on year. This is correlated with Grab’s strong cash position versus its regional and global peers.

While overall every major player was ‘rationalising’ marketing and promotions spend, the cash position impacted the players’ flexibility in balancing growth and profitability. DeliveryHero Group, which is reported to be divesting Foodpanda Thailand, is in a net debt position, which means it will need to decide where to focus its resources.

We will release another report toward the end of Q1 2023 to address other key performance metrics of the platforms – and compare them Apple to Apple.

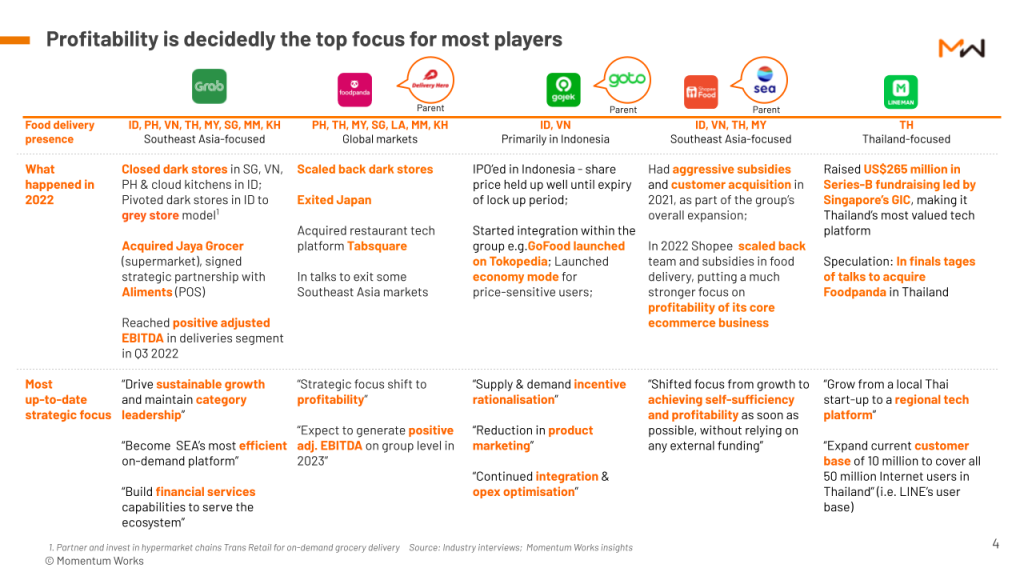

- Profitability is decidedly the top focus for most players

Both Grab and DeliveryHero scaled back on dark stores, whilst Sea Group (Shopee) scaled back on subsidies and the food delivery platform business as a whole. Both Grab and Lineman went on to/ are in the midst of acquiring strategic companies – Grab with Jaya Grocer and Aliments; whilst Lineman was speculated to acquire Foodpanda Thailand (probably at a good discount). GoTo finally started the integration between GoFood and its ecommerce platform Tokopedia.

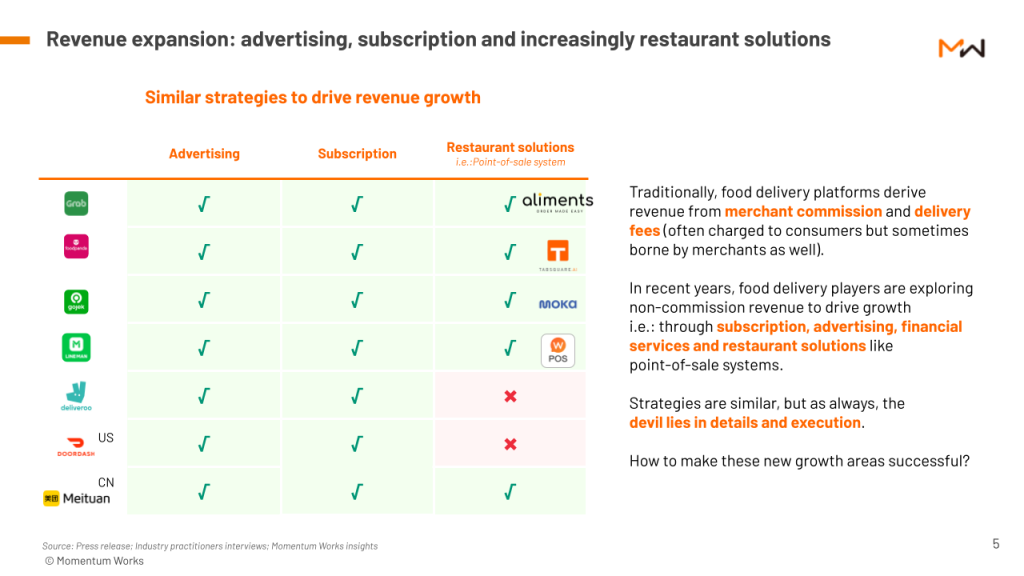

- Revenue expansion: advertising, subscription and increasingly restaurant solutions

Traditionally, food delivery platforms derive revenue from merchant commissions and delivery fees (often charged to consumers but sometimes borne by merchants as well).

In recent years, food delivery players are exploring non-commission revenue to drive growth i.e. through subscriptions, advertising, financial services and restaurant solutions like point-of-sale systems.

Strategies are similar, but as always, the devil lies in details and execution. Our basic formula for platform success has not changed: volume, density and operational efficiency.

More insights

You can obtain your copy of The Food Delivery Platforms in Southeast Asia report here.

You can also join our report briefing on 18 January (Wednesday) at 3-4pm Singapore time. Register for your spot here!