Last year’s turbulent year for cryptocurrencies did not go unnoticed. It all culminated in the dramatic downfall of FTX; today, we have naysayers say, “more and more people are seeing this for the scam that it is,” and unfortunately, the negative sentiment surrounding crypto has trickled into blockchains as well. But blockchains go far beyond the cryptocurrencies that are hosted on them.

Everyday businesses that we interact with on a daily basis, like banks, supply chain owners, and even airlines, already leverage this technology, and in our “Off the record: Web3’s brutal year” event we dove into these examples in a little more detail.

As discussed in our event, more and more enterprises are adopting blockchain technology, whether in their back-end or in a consumer-facing way. Loyalty programs, ticketing, and interbank transactions are just some of the use cases being affected. Why are organisations quietly adopting blockchain despite all the potential risks, complexity and risks?

First, let’s take a look at what makes up a blockchain: transactions and decentralised blockchains.

Transactions

Transactions, and all the information that accompanies them, are piled atop one another and put into a “block”. This block is then validated and “chained” to the previous block, and this cycle continues to form the blockchain.

Now, the most common example of this technology in use is with cryptocurrencies such as with Bitcoin and Ethereum’s respective blockchains, but there are ways to leverage this technology as a business as well.

P.s. check out our Web3.0: The inevitable next step report where we build up the foundation of Web3.

Decentralised blockchains & public chains

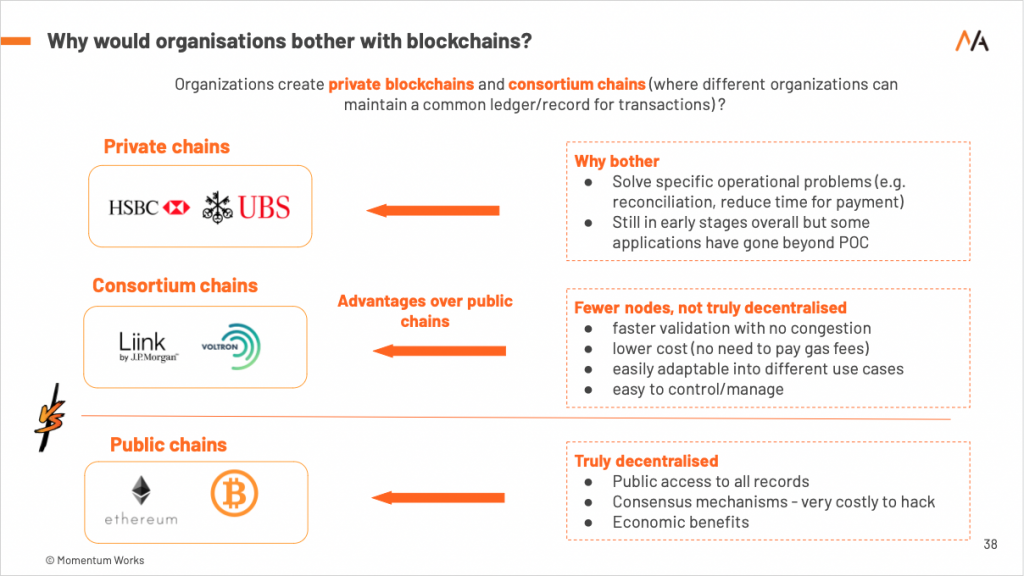

Bitcoin and Ethereum are both completely decentralised blockchains, which means that they have no “owner”.

In fact, just recently, I was clarifying with my team that Vitalik Buterin, the creator of Ethereum, doesn’t own Ethereum. He may have ethereum tokens but he cannot control Ethereum (the way that Elon Musk can control Tesla).

This also means that anyone and everyone has access to the transaction information that is hosted on them. Public chains like these are extremely difficult – I would go so far as to say nearly impossible – to tamper with, but are not fully scalable at this stage, and remain pretty inefficient in terms of speed.

Public chains are not suitable for businesses

For almost all businesses (traditional or tech), keeping their data and their customers’ data private is key.

For example, a bank in Singapore has to adhere to strict privacy laws with their consumer’s data. So how would they benefit from this technology?

Enter: private blockchain.

Private chains have an owner; someone who oversees the ledger, and decides who has access to it. Unlike public chains, they don’t need as much effort to validate transactions because they control all the data; so validating transactions becomes much, much faster.

Private chains can be good for businesses, but they don’t make sense if the business isn’t highly transaction based. They aren’t necessarily easy to implement, and plug and play solutions that exist can be costly. They can be tampered with by permissioned users within the organisation, but have the benefits of being extremely efficient in terms of speed and easily scalable.

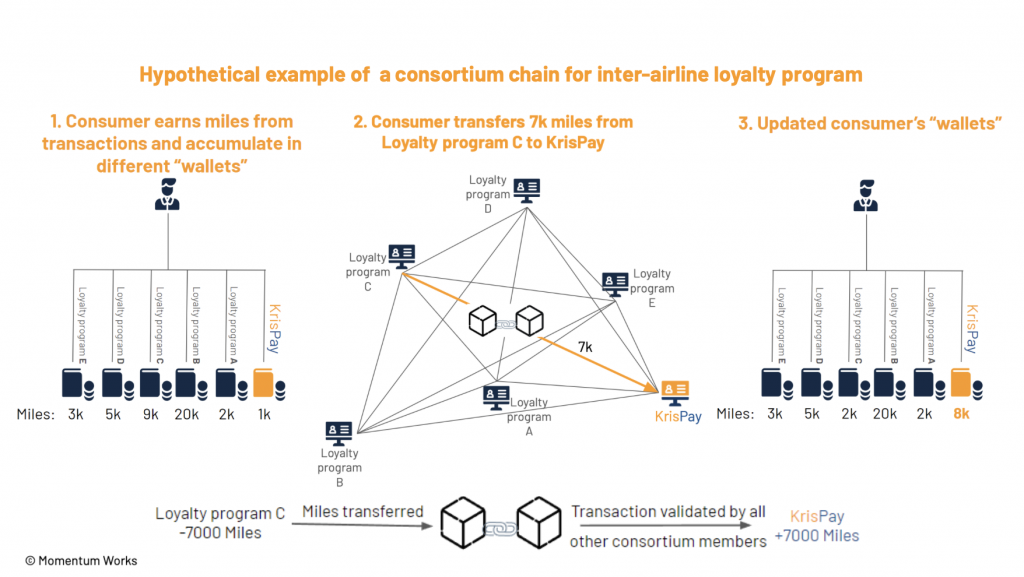

Let’s use the example of a business with a loyalty program – take Singapore Airlines’ Krispay.

A single customer could make a hundred, if not thousands of transactions in a given year, and with thousands of customers, manually processing reconciliations would leave room for human error, not to mention the amount of time it would take. Solving specific operational problems is one way a private chain could come in handy. Reducing time for payment and customer friction is always a good thing.

Because these blockchains have less users than public ones, as well as no anonymous users, it doesn’t make sense for the security on them to be based on overpowering more than 50% of the system – financially or in terms of power. Instead, the private chain owner can select trusted participants to validate the transactions and confirm the blocks to the chain.

There are a few more reasons private blockchains could be more secure than existing processes, including having untamperable proof of which participant facilitates each step of any given transaction. They also eliminate the need for a third party intermediary to validate these transactions, which not only decreases data vulnerability, but also decreases costs.

Now that we have the theory down, where would this technology come into use?

Theory always makes sense, but in practicality it is always more complicated.

How blockchain technology has been used by corporates is interesting, especially when companies want to break the chinese walls between one another.

What happens when there are four or five companies that want to share specific information, quickly and securely?

Let’s say KrisPay decides to merge its loyalty program with another airline for some reason. A customer wants to transfer points from one account to the other, but if there has to be one organisation to own a private chain, how could blockchains be of use in this scenario?

Enter: consortium blockchains…

A consortium chain is built when several organisations team up and decide to create a distributed ledger amongst them, where each organisation gets to give a metaphorical thumbs up before each block of transactions is added.

This way, they can all share select information with one another, and process inter-organisational transactions as well as share information faster. Now, if we apply this concept to our example of our multi-airline loyalty program, and we consider the two airlines to be two members of the consortium (two of the chain’s owners), the transaction between the two airlines is more seamless because it is processed on the same blockchain.

Consortium chains are a little tougher to tamper with, and share the benefits of being easily scalable and very efficient. They do, however, require every participant to maintain the integrity of the system.

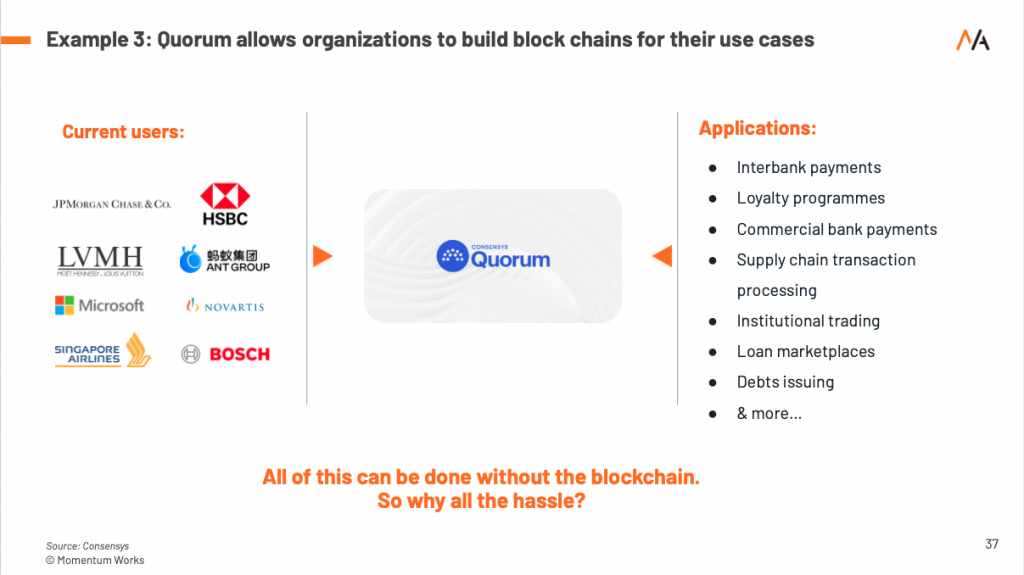

This is all very well and good in theory, but you might be wondering: has anyone ever done this? In our talk, we explored one platform where many of these applications are built, called “Quorum”.

What is Quorum (and why are we talking about it)?

Quorum was built in 2016 by J.P. Morgan, based on Ethereum’s existing technology, and they launched interbank payments on the platform in 2017. At the time, the engineering lead for JPM, David Voell said that the key was, “a single blockchain of everyone continuously checking the integrity.”

In late 2020, Quorum was sold to Consensys. Whether it was offloaded for being unprofitable for JP Morgan (as was speculated at the time), or whether both parties saw it as mutually beneficial to increase adoption of the open source technology is up for debate, but since then, many more applications have been built atop the platform; from fashion related to the oil industry.

While these technologies have now gone beyond Proof of Concept, the whole industry is still in its infancy. It’s important to remain critical about whether there are true benefits to adopting blockchain for a business. For more on this topic, feel free to check out the recording of our “Off the record: Web3’s brutal year” talk here.

If you want to find out more about Web3, you can check out our write-ups: Off the record, Web3’s brutal year , and Web3: Our future or just a beautiful ponzi scheme?,