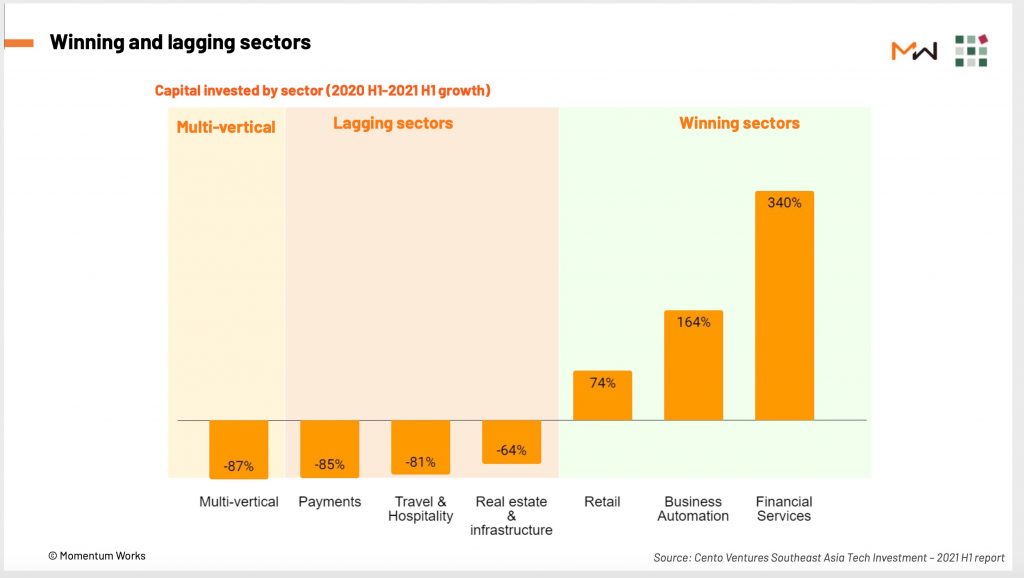

In the recently published 2021 H1 Southeast Asia tech investment report, the team at Cento Ventures have highlighted the winning and lagging sectors. The tech sectors here are defined according to the underlying sectors they are disrupting, or modernising.

As you can see, the most obvious is the surge of digital financial services – growing by 340% compared to H1 2020.

In our online briefing on the report last week, attended by more than 300 stakeholders, Dmitry Levit and I thought it would be useful to highlight a few key trends in the booming digital financial services sector. We have identified the following trends, which have evolved quite a bit from half a year ago.

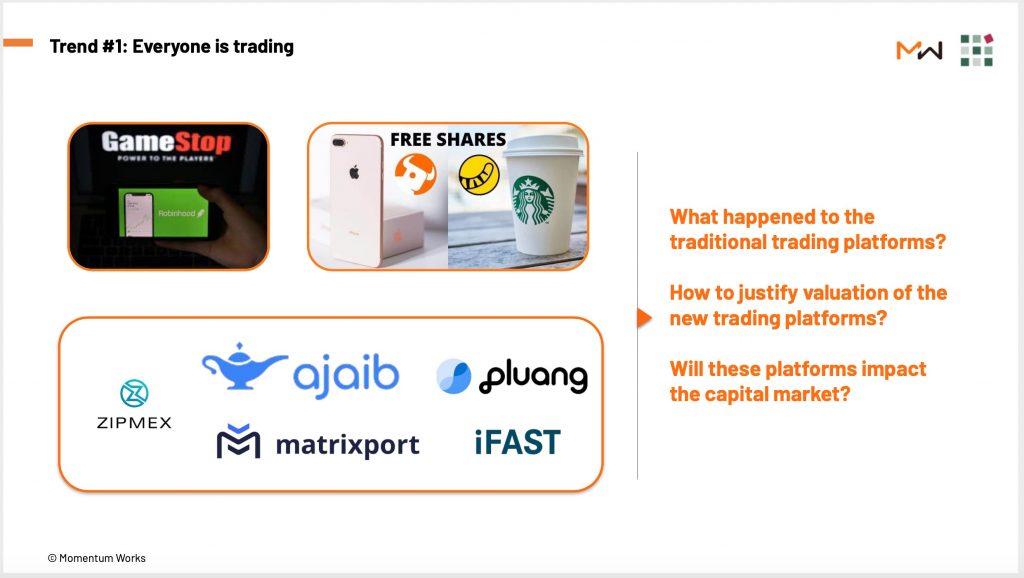

Trend 1: everyone is trading

From stocks to crypto, Southeast Asia’s consumers are following the global trend of trading frenzy during the pandemic.

Indonesia’s Ajaib, which was inspired by Robin Hood (and maybe China’s Futu), has risen quickly; Matrixport, a Singapore-based, Chinese-founded crypto wealth management platform, has reached unicorn valuation; and not to forget iFast, the Singapore listed digital wealth manager which saw share price surge over the last year, giving the company a US$2 billion market cap:

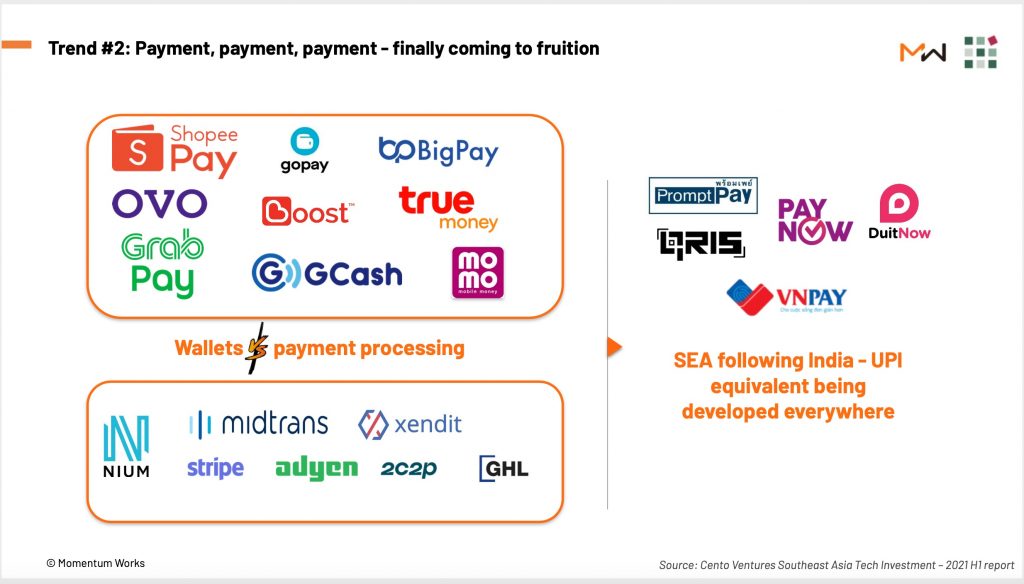

Trend 2: payment, payment, payment – finally coming to fruition

Finally, people realised that the digital wallets in China, which many in Southeast Asia tried to imitate, are not exactly digital wallets. They are in fact enclosed mobile payment ecosystems made possible by the large user base and use cases provided by their parents.

In the meantime, many payment processing companies (the regional or local versions of Stripe and Adyen) are doing very well. Xendit, which became a unicorn after a recent Tiger Global funding round, is the most obvious example but there are many others hidden in plain sight.

And of course, we should not forget the efforts by different countries to build their own digital payment switches to stop paying tolls to international card networks. These efforts will alter the digital payment landscape in the countries – as India’s UPI has shown.

Efforts to connect these switches (or Singapore’s PayNow – Malaysia’s DuitNow, or PayNow – Thailand’s PromptPay) could have big implications and enable very interesting business models:

Trend 3: credit scoring:

Trend 3: credit scoring:

The zeal over direct fintech lending (P2P etc.) has subsided in the region. The replacement, BuyNowPayLater (BNPL), charges a much lower effective interest rate, and is more demanding on the operators’ ability to control risk. Same can be said about digital banks, another boom in digital financial services.

FinAccel, which owns BNPL platform Kredivo, and Advance Intelligence Group, which owns Advance AI and BNPL service Atome, are two examples of fintechs which have focused a lot of credit scoring data models.

Of course, compared to Ant Group and Tencent, which have tens of thousands of attributes for their credit scoring data models, most digital players in Southeast Asia are still relatively modest and rudimentary.

The question is what is enough for the region, and how will that boundary evolve. This is especially the case when players like Shopee have entered lending space on their own.

They have the richest data (ecommerce consumption) to really fine tune their models. Besides, in the specific case of Shopee (or SeaMoney), it can tap into good, experienced talent from China, after the broad P2P crackdown over there.

Expect more competition in Southeast Asia.

And of course, we can’t forget the local IPO of Malaysia-based CTOS digital, which has attained a market cap of more than US$1 billion.

Additional trend: MSME digitisation in Indonesia

In addition to the three trends above, we also have an interesting intersection of financial services, retail and business automation: the digitalisation of small businesses in Indonesia.

We find the often quoted number of 64 million micro, small and medium enterprises (MSMEs) intriguing (in comparison, there are 67.5 million households in Indonesia according to the 2020 census). However, the opportunity is indeed big – no wonder there are so many different companies trying out different models to target this segment:

The danger for (especially earlier stage) startups here is, it can be very tempting to bump up the top line growth with two items: cigarettes or Indomie (instant noodles). The FMCG categories will sell fast, but give hardly any customer stickiness or margins.

Momentum Works is currently preparing a new report called “Menjamur: the race to digitise 64m small businesses in Indonesia”. You can subscribe to our newsletter on TheLowDown to get notified when it is ready!

Momentum Works is currently preparing a new report called “Menjamur: the race to digitise 64m small businesses in Indonesia”. You can subscribe to our newsletter on TheLowDown to get notified when it is ready!