On 16 August, Sea Group announced their Q2 2022 results. It seems many analysts were really baffled by the fact that the management refused to give renewed guidance for the year – a number of questions in the earnings call were harping on this point. You can read the full transcript for details.

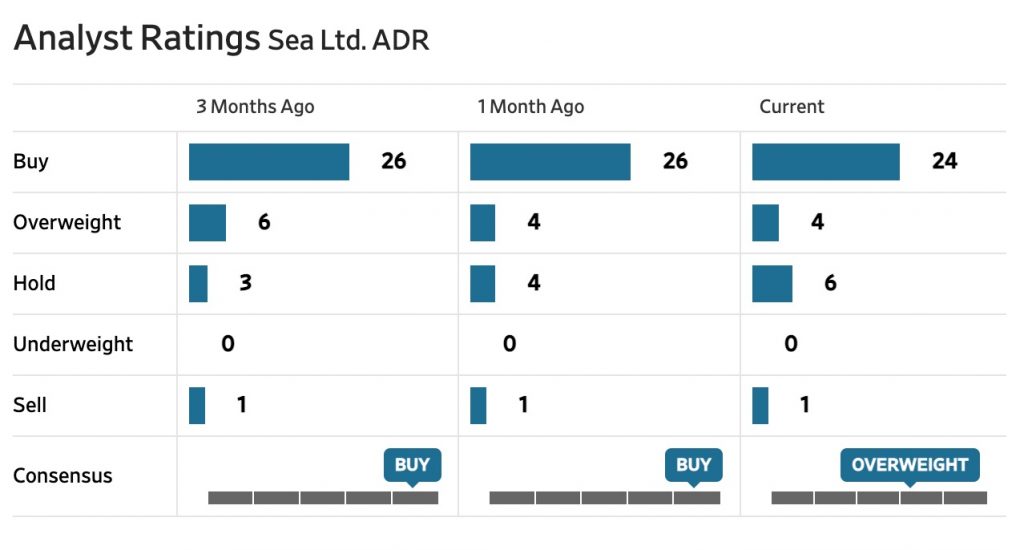

Most analysts still gave the “Buy” or “Overweight” rating, but many lowered the revenue projections, and thus the target price. The market, as usual, quickly voted with their feet, sending the share price down by more than 22% in the four trading days after the release.  We have recently published a commentary on whether Shopee is ‘in decline’. In that piece we have expressed clearly our viewpoints on Shopee’s leadership, people, organisation, and product. Here we would like to share some thoughts about the Q2 results, and Sea Group’s future:

We have recently published a commentary on whether Shopee is ‘in decline’. In that piece we have expressed clearly our viewpoints on Shopee’s leadership, people, organisation, and product. Here we would like to share some thoughts about the Q2 results, and Sea Group’s future:

Our thoughts

- The problems with the digital entertainment business are not new at all. People had expected the decline because of either the lifecycle of Free Fire or the reopening (where people spend less time playing heavy games). Although many were still shocked by the Q4 2021 results, which showed decline in bookings for the first time. Many mobile gaming veteran friends have told us that this is an industry wide problem – just that other companies did not need to use the gaming profit to subsidise a costly ecommerce business.

- Sea Group emphasised the fact that the quarterly active user number for its digital entertainment business stabilised quarter over quarter in Q2. However, paying user number has declined, and the active user number stabilisation could be largely due to Ramadan holidays in Q2. To reverse the downward trend of Free Fire is not exactly realistic. Garena will continue to do what it has already been doing: multiple tactics to try to extend user activity and game lifespan.

- In this short term, we should not hold high expectations on new games contributing to the Group’s revenue and profit. At the moment, Moonlight Blade, a Tencent-developed game published by Garena, is doing well in Thailand. In the meantime, Garena has been delaying the release of a major new game called Undawn, also by Tencent. Whether Undawn will become a hit (as Free Fire did), and if so how many quarters of user operations are needed before it becomes a hit, are all unknown. Also, worth remembering that unlike Free Fire, these games are not developed by Garena (therefore the profitability levels will be very different).

- Garena’s gross Billings grew 7X between 2018 and 2021 – and moving forwards, the growth and profitability of Shopee and SeaMoney will probably be more important for Sea Group as a whole.

- Shopee GMV will not grow as fast as it did in 2019-2021, where it doubled every year. However, a 30% YoY growth is already very good, and enough to keep widening the gap with competitors. However, in the current landscape (and declining gaming revenue), investors are more concerned with Shopee’s ability to make a profit. A number of analysts asked such questions during the earnings call. Sea Group expressed that the guidance for digital entertainment and digital financial services remains – therefore the major uncertainty is on ecommerce.

- There are three ways to achieve profitability: increase seller commission, grow ads, and lower costs/subsidies on logistics/payment. The first two are essentially the same (combined as the % of GMV sellers are willing to pay to get sales). Many sellers are already complaining that it is hard to make money on Shopee, while TikTok Shop is actively trying to grab ecommerce market share in Southeast Asia. Shopee will need to manage the difficult task of achieving profitability without driving brands/sellers to competitors. At least it has been actively building its own logistics, which will take a bit of time to show results at scale.

- In June this year Shopee carried out a round of layoffs, especially in fringe markets as well as food delivery/payment businesses in Southeast Asia. This should have a positive effect on costs in the second half of 2022. As the layoffs were only carried out at the end of Q2 – theoretically it probably increased the costs in that quarter.

- Shopee is essentially following the growth pathway of Taobao – occupy as much online consumer traffic as possible, and then monetize through ads (especially to brands) and build additional services such as digital lending. The question is whether the same pathway is valid for Southeast Asia – for that different people have (vastly) different perspectives. Our summary, after hearing all these perspectives, is that before someone proves it, nobody actually knows. Similarly, nobody knew whether Meituan could become profitable in food delivery, before it did. One thing is for sure: in Southeast Asia because of the market fragmentation, infrastructure and other factors, friction is much higher compared to China. In other words, to win in this market, a platform probably needs to have better operational efficiency compared to their counterparts in China.

- Shopee has been using the same tactic in Brazil and Latin America – although in market, infrastructure, competitive landscape etc. Latam is very different from Southeast Asia. To win, Shopee needs to put good effort in leadership, people and organisation, especially in the current capital market environment where it can no longer trade time/efficiency with money. The major competitor there, Mercado Libre (Meli), is still favored by the capital market – Meli’s share price only declined by about half, versus Sea Group’s 80%.

- On the latest Balance Sheet (by 30 June 2022), Sea Group has short term loans receivable (net allowance for credit loss) of about US$2 billion – a ⅓ increase from the Dec 2021 level of US$1.5 billion. We are not sure whether it signifies the loans outstanding of SeaMoney’s consumer credit business. The allowance for credit loss is about 8.8% of the total loan outstanding – where in reality the non performing loan ratio should be lower than that.

- Also, Sea Group spent US$540 million in the first half of 2022 to buy property and equipment – an amount that is more than twice the balance of property and equipment as of the end of 2021. We are not sure whether it is because of the investment in logistics and services, or is there anything else there. Regardless, logistics infrastructure and servers can be monetised – just like how Amazon did with FBA and AWS.

- Most of the pointers above are about market, technical and operational issues. The most important adjustments Sea Group needs to make are around leadership, organisation and people. The high speed growth phase of 2019-2021 is over, moving forwards the core leaders/managers will need to spend a few times the effort to achieve the same level of results. This will be a big test on people’s mentality as well as the capabilities of the leadership. As for the turnover at the mid and junior levels, we still do not think it is a major problem that the company should be concerned about.

- Lastly, the mentality of key managers will be very different in driving for growth versus trying to achieve profitability. A few of Momentum Works’s team members have had the experience of leading cash burning venture building games – and we understand this deeply. A core organisational advantage could become its key weakness or even Achilles Heel in a different phase of the organisation. We believe that in this aspect, Sea can learn a lot from Alibaba and Meituan – who had been through similar challenges multiple times.

Seeing the unseen

Much of the experiences and lessons learnt are covered in our new book “Seeing the unseen: behind Chinese tech giants’ global venturing”, which will be published by Wiley in September.

You can pre-order the book on Amazon.

We welcome thoughts, comments and debates about Shopee and the general theme of emerging market tech expansion, you can email us at [email protected].