")

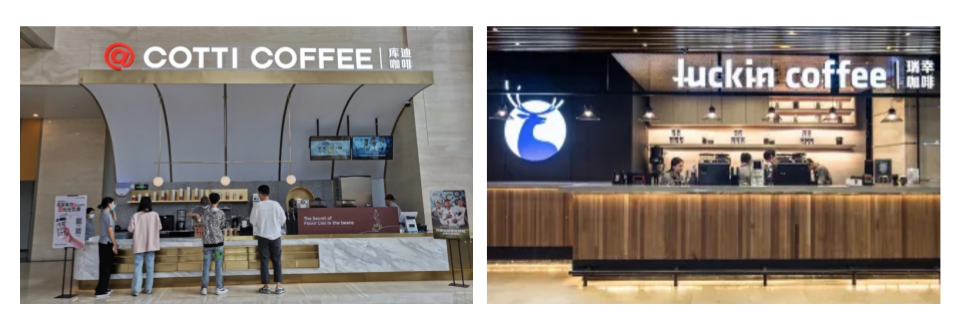

Luckin Coffee, the largest coffee chain in China which recently opened in Singapore, has hit a milestone in China – opening its 10,000th store.

Its ousted founder, Lu Zhengyao, however, is mounting a challenge by launching a new rival coffee brand, Cotti. Since opening its first store in October 2022, Cotti has already reached more than 3,000 stores by the end of May 2022.

Luckin and Cotti are competing in the same space – with similar product and pricing

This highlights how cutthroat China’s coffee chain business is – where Cotti and Luckin are not the only contenders.

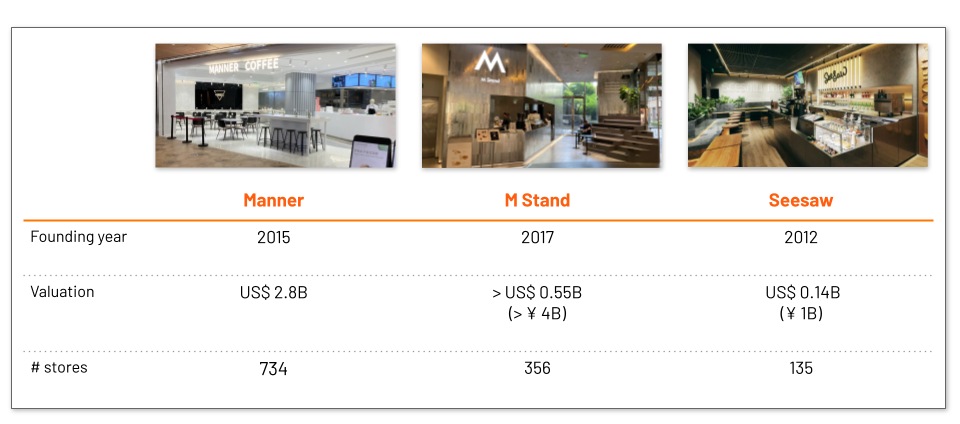

Few other players have reached meaningful scale and valuation: e.g.: Manner ($2.8B valuation), M Stand (> US$ 0.55B valuation) and Seesaw (US$ 0.14B valuation).

The rise of premium chains?

Beyond the rise of mass-market-focused Luckin, some premium coffee chains are also brewing under the purple ocean of the coffee market in China.

Some of the players that have raised funding recently

Compared to Luckin (<¥20 or US$2.8 per cup after discounts), a cup of coffee in a premium coffee chain is normally priced around ¥30-50 (US$ 4.2 – 7), i.e. Starbucks’ pricing levels in China.

While mass market brands typically run on a more asset-light model, with small storefronts / kiosks optimised for order pick-up/delivery and little (or no) dine-in space, premium brands (e.g.: M Stand, Seesaw, CUP ONE) typically run a more asset-heavy model with a large storefront and similar concept to Starbucks’ “third place between home and work”.

M Stand store

M Stand store

As you can imagine, the asset-heavy model is expensive to operate and slow to scale.

CUP ONE for example, which runs on a large storefront providing coffee and (proper) food, has been very slow in its expansion – opening only three stores since its founding in 2012.

CUP ONE store

In comparison, Shanghai-HQ’ed Manner, which runs on the more asset light model providing coffee which many Shanghainese claim to be really good quality, has been expanding much faster to more than 700 stores (larger than Kopi Kenangan in Indonesia).

All these numbers, though, still trail far behind Luckin’s 10,000 or Cotti’s 3,000.

Manner store

Manner store

Can premium coffee brands challenge the likes of Luckin?

We have done some calculations in our Bubble Tea in Southeast Asia report last year on the viability & scalability of premium bubble tea chains. We have also previously talked about whether Heytea’s premium bubble tea model is sustainable.

At that time, our thought was that a mass market chain can survive and (optionally) add a premium offshoot, while a pure premium chain will hit its growing ceiling much faster.

Does it apply to coffee chains as well? Let’s do some calculations here, on a single-store basis:

Premium coffee brands are selling at ¥30-50 per cup, and according to a few sources in China, many premium outlets are selling 200-300 cups per day on average.

Luckin, on the other hand, is priced at < ¥20 per cup, with daily sales of 500-600 cups on a weekday and up to 900 cups on weekends.

Which means on a per-store basis Luckin’s coffee revenue is easily double that of a premium brand.

Of course, premium brands supplement coffee with food/snacks to increase the average order value.

But overall a premium brand still runs a higher cost structure compared to the likes of Luckin.

That is coupled with the limitations in optimal locations and consumer base, which impact scalability.

How to differentiate

As Momentum Academy has shown in a recent Sip, Innovate, Repeat – Lessons on Innovation workshop – any premium value proposition would limit the customer base, and there are many more brands focusing on ‘quality’ rather than ‘selection’ and ‘savings’ – the latter two being hallmarks of mass brands like Luckin.

In May, Luckin Coffee announced the launch of franchising-with-own-store model (带店加盟模式) – i.e.: encouraging people who own shops in strategic locations like malls to become franchisees – a move that will speed up its expansion plan and secure good locations.

Starbucks, on the other hand, targets to open 3,000 more stores in China, and operate a total of 9,000 stores in 2025 – Luckin’s level earlier this year.

With key players in their full force, premium coffee chains (or any players) have to find their way amongst strong players like Starbucks (“Third Place between home and work”), Luckin (with mass market pricing) and McCafe /7-Eleven/gas stations (“fast and easy”).

Besides, they have to compete against each other.

More insights

Find out more in The Impulso Podcast E09 – Bubble Tea in Southeast Asia where we discussed the business model behind Southeast Asia’s favorite drink. You will find a lot of parallels between that and the coffee chain business.

Momentum Academy has also condensed some of the learnings into our workshop “Sip, Innovate, Repeat – Lessons on Innovation Infusing Luckin Coffee, Starbucks & Mixue‘s Strategies into Your Organisation for Success”.

If you are interested in bringing such learnings to your organisation, please contact [email protected].