Last week, Volt Bank, the first exclusively online bank to gain an Australian banking licence shut down and returned deposits and is selling its mortgage book. Media reported that it had failed to raise sufficient funds to support the business.

This topic was a hot topic in the Friends of Momentum Works (FMW) group– especially from Charlie and Chek Tee who used to drive innovation at banks. With the number of digital (or neobanks) expanding in Southeast Asia – there are many stakeholders who are viewing how Volt Bank failed, and whether the same would happen here in Southeast Asia.

Volt bank (like many of the other neobanks in Australia) did not have any income generating products, and relied heavily on external capital to sustain operations.

This is the common way for startups to scale under normal circumstances. However, 2022 is not normal – and in the current investment environment, Volt could not raise the additional AUD$200mil (US$138mil) needed to take the bank through the tech winter.

Volt Bank had tried to pivot in their business model to Banking as a Service a few years back and were aggressively executing on that, including establishing themselves as a digital assets friendly bank but unfortunately that journey was cut short as we saw on the news last week.

Volt is not the first neobank in Australia to fail. Xinja folded in 2020, and 86 400 (pronounced as “eighty-six, four-hundred”) was acquired by National Australian Bank in 2021. Amongst the original four licensed neo banks in Australia, only the SME-focusing Judo is still standing – it made to the public market in November 2021:

So what happened?

In the FWM group, we debated whether Volt, Xinja and other neobanks across the world were inspired by the success of Nubank in Brazil.

This is a sentiment globally, not just limited to Australia or Southeast Asia – in fact, certain digital banks in Southeast Asia are specifically modelled after Nubank.

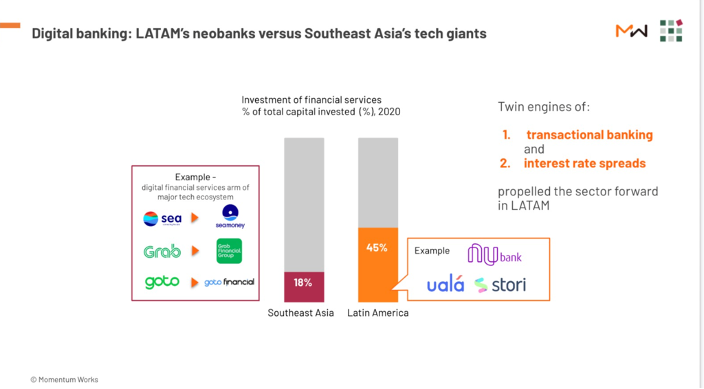

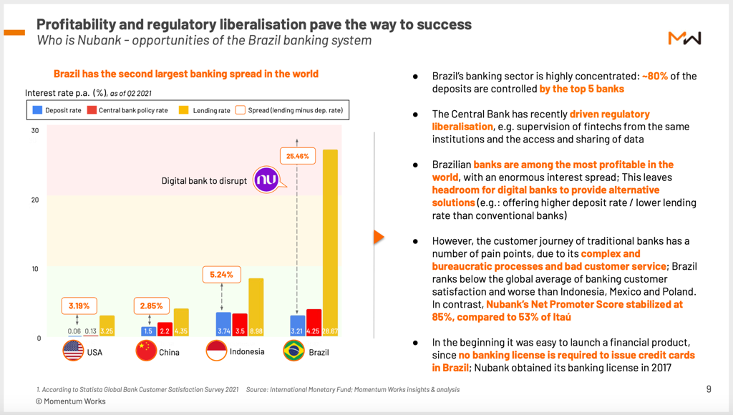

However, each country is different – Nubank has identified specific opportunities (e.g. high interest rate spread, and poor banking experience) in Brazil which might not exist in other markets:

Digital banks in Southeast Asia

For example, while in the West there is a general distrust in incumbent banks and grumbles over high fees, in Thailand it is hard to imagine that the leading banks are not offering a good consumer experience. In fact, the leading banks there went as far as building commission free food delivery platforms.

In Indonesia, leading banks have been able to guard consumer trust, while NOT waiving or reducing fees, even if they were in a very competitive market. In general, incumbents in Asia actively shun from activities that attract non-profitable clients. They are also aware that the interchange from card processing will not be enough to cover the interest paid to depositors, let alone business overheads and consumer costs.

People in Southeast Asia are still generally happy with Main Street banks and also trust them. Even if they are not happy, they still trust them to hold their life savings.

This is why Digital banks in Southeast Asia do not try to go against the system, but co-exist with the main traditional banks. Some focus on specific segments (BRI Agro in Indonesia) or demographics (Jenius in Indonesia); while others (like Seabank and Bank Jago) piggyback on large tech ecosystems. Large tech ecosystems also work with traditional banks for capital access.

Tactics also differ between countries. For example, in Singapore it would rather be unwise for any neo bank to go against incumbents (case in point: digital banks in Hong Kong); while branch cost is identified as a reason for traditional banks to move digital, more than in other countries; while the interest spreads in Indonesia and the Philippines allow digital banks ways to offer more attractive deposit rates while maintaining profitable.

Over the last year, we have published a number of digital bank related reports: Rise of Digital Banks in Indonesia; Digital Banks in Malaysia; Who is Nubank; and Decoding Digital Banks: best practices. You can find plenty of useful insights and analyses in these reports – you can obtain copies at our Insights page.

Another interesting phenomenon in Nubank is that its founders are not banking veterans. In fact, Nubank does not have a banking licence – and does not need one in Brazil to offer the ‘banking’ services they are offering now.

In a way, the path is indeed ‘nu’.

Maybe some lessons to be learned there as well.